Company Update

For the six months ended 30 June 2019, the company's revenue was HKD 2,004.0 million (corresponding period in 2018: HKD 1,310.8 million), representing an increase of 52.9%. Revenue from power sales and waste treatment was HKD 853.8 million (corresponding period in 2018: HKD 763.2 million), representing an increase of 11.9%. The operating profit was HKD 566.0 million (corresponding period in 2018: HKD 440.1 million). Profit attributable to equity holders of the company was HKD 400.8 million (corresponding period in 2018: HKD 318.0 million), representing an increase of 26.0%. Basic earnings per share was HK16.3 cents (corresponding period in 2018: HK13.0 cents). The interim dividend of HK3.2 cents per ordinary share for the six months ended 30 June 2019 (six months ended 30 June 2018: HK1.9 cents per ordinary share). The company's performance of core business is basically consistent with our forecast, related performance increase in total revenue was mainly contributed by the construction revenue from the additional projects. Additionally, Xinfeng WTE plant and phase 2 of Beiliu WTE plant commenced trial operation, and phase 1 of Lufeng WTE plant commenced trial operation in 2018Q3. Together with the stable contribution from the existing plants, the company recorded satisfactory results.

Investment Highlights

Benefit from the development opportunities brought by environmental industry policies

With 2020 being the last year of the 13th Five Year Plan, new project opportunities will continue to be tendered by local governments in order to achieve the 54% municipal solid waste treatment by incineration target. Following the ¡§Notice on the Implementation Plan of Municipal Solid Waste Sorting System¡¨ released by the General Office of the State Council in March 2017, which targeted a municipal solid waste recycle rate of 35% in 46 selected cities by 2020, a new ¡§Circular of the Ministry of Housing and Urban-Rural Development and other Departments on Implementing the Classification System for Municipal Solid Waste in Cities at or above the Prefecture¡¨ was released in June 2019, which targeted to establish municipal solid waste sorting system in 46 selected key cities by 2020, and in all prefecture and above level cities by 2025. In response to the Central Government's plan to promote the implementation of waste sorting system, the ¡§Shanghai Household Waste Management Regulation¡¨ became effective in July 2019, and Shanghai became one of the first pilot cities to require its residents to strictly follow waste sorting practice. The company believes that the waste incineration power generation industry will continue to develop steadily and rapidly in the next few years, and it will capture the opportunity and benefit from such new growth potentials.

Waste incineration business processing capacity has been steadily improved

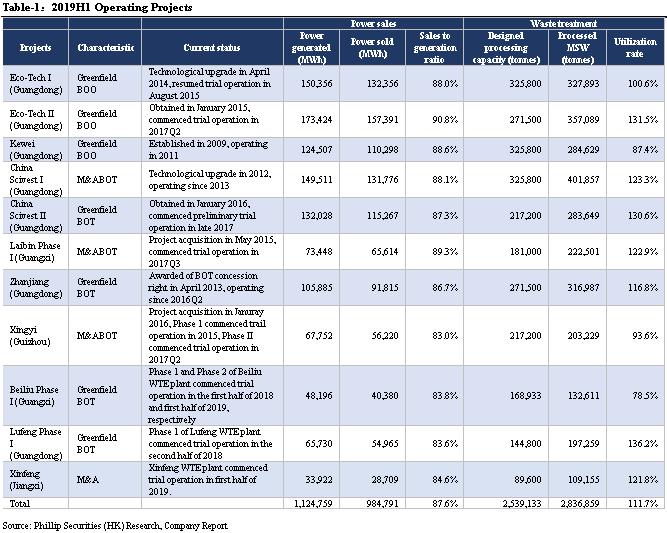

As of 30 June 2019, the operating, secured, announced and under management agreement daily MSW processing capacity of 23 projects was 34,490 tonnes, the operating daily MSW processing capacity of 12 projects (including the project under management) reached 15,890 tonnes. As of 22 August 2019, the operating, secured, announced and under management agreement daily MSW processing capacity of 25 projects is 36,590 tonnes. During the period under review, the company's implementation of innocuous treatment of waste volume amounted to 2,836,859 tonnes, representing an increase of 19.8% YoY. The company generated 1,124,759,000kWh from green energy, saving 348,650 tonnes of standard coal and reducing emission of carbon dioxide by 1,907,847 tonnes. During the Period, the company further expanded its presence to other provinces. 1) The company were awarded Mancheng WTE PPP project in Hebei Province and the Ruili WTE PPP project in Yunnan Province, with the daily MSW processing capacity both being 1,000 tonnes. 2) The company entered into an agreement for the acquisition of 49% equity interest of the Machong Town WTE project in Guangdong Province with a total daily MSW processing capacity of 2,250 tonnes. 3) The company were awarded the Shaoguan WTE public-private-partnership project in Guangdong Province in July 2019 and the Qiandongnan Prefecture South Area WTE project in Guizhou Province in August 2019, with the daily MSW processing capacity both being 1,050 tonnes.

Closer cooperation with SIHL

In March 2019, the company entered into an agreement with Shanghai Fudan Water Engineering Technology Co., Ltd (a non-wholly-owned subsidiary of SIIC Environment Holdings Ltd, which is an associate of SIHL), Shanghai Nanyi Environmental Technology Company Limited and Shandong Sanding Company Limited, both of which are Independent Third Parties, for the establishment of a project company, which will be principally engaged in the investment, construction and operation of a WTE project with total daily MSW processing capacity of 1,200 tonnes located in the Circular Economy Industrial Park in Shen County, Shandong Province. The establishment of a project company with SIHL represents an important new business development model for the company, and the company will capture more new project opportunities via the same cooperation model in the future.

New developed environmental hygiene services

To perfect its business model, the company further extended its business portfolio to the treatment of fly ash, bottom ash and environmental hygiene business. The company indirectly holds 35% equity interest in Dongguan Xindongyue, which currently owns the first landfill project for fly ash in Dongguan City. During the first 6 months of 2019, it processed 49,048 tonnes solidified fly ash under the strict treatment requirement by the local environment authority. The company indirectly holds 40% equity interest in Zhongzhou Environmental, which is principally engaged in the treatment of bottom ash created from the incineration of waste in China. Zhongzhou Environmental is under trial operation. Sichuan Jiajieyuan, a renowned environmental hygiene and related services player in China, continued to provide stable contributions during the period under review. The company holds 41% equity interest in Johnson, which indirectly holds 100% equity interest in Johnson Cleaning Services Company Limited, a leading environmental hygiene service provider providing a wide range of environmental services in Hong Kong. Johnson Cleaning Services Company Limited continued to provide stable contributions during the period under review. In the first half year of 2019, the company recorded a total income of HKD 52,104 million of environmental hygiene services, accounting for 2.6%.

Financial Forecast and Valuation

Financial Performance

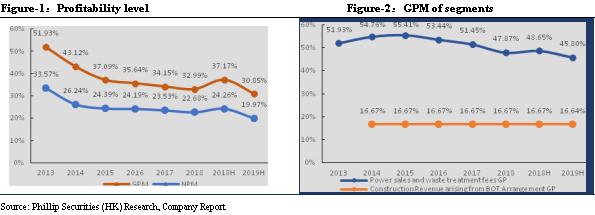

In the first half of 2019, the company realized gross profit of HKD 618.3 million, representing an increase of 26.9% YoY as compared to HKD 487.2 million in 2018. The increase in gross profit was mainly attributable to the construction plants. Gross profit margin of the company decreased from 37.2% in 2018 to 30.9% in 2019. The decrease was mainly due to the profit from construction projects which has lower margin.

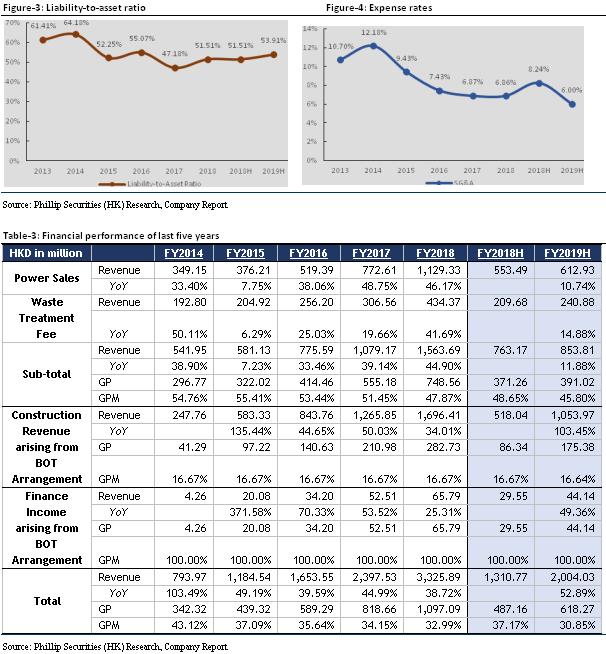

After the company went public in 2015, the liability-to-asset ratio fell to 52.25%. In recent years, it has been a dynamic trend, and the average overall liability-to-asset ratio has remained at 53.91%, increasing 2.4% compared with 2018. In terms of expense rate, the company's overall expense rate has decreased from 12.18% in 2014 to 6.86% in 2018, and to 6% of the first half of 2019, which we believe that it was beneficial from the company's effective internal cost control, overall expense has declined gradually year by years.

Financial Forecast and Valuation

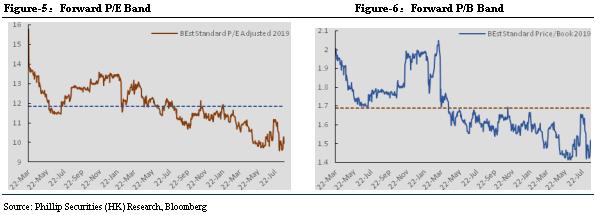

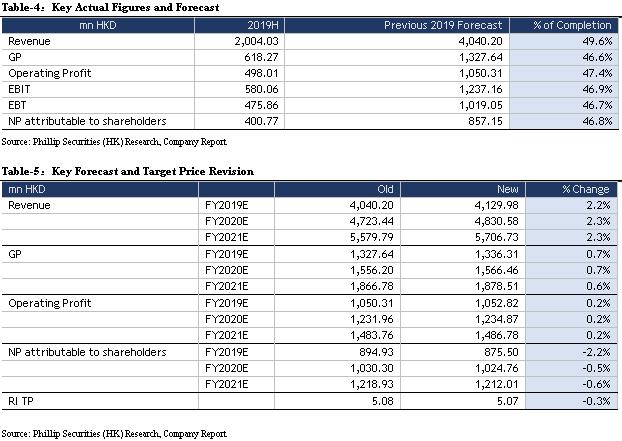

We adjust the company's revenue in FY19/FY20/FY21 to be HKD 4.13/4.83/5.71 billion, representing increases of 24.18%/16.96%/18.14% YoY; gross profit will be HKD 1.34/1.57/1.88 billion, representing increases of 21.80%/17.22%/19.92% YoY; net profit attributable to shareholders will be HKD 0.88/1.02/1.21 billion, representing increases of 16.06%/17.05%/18.27% YoY; corresponding EPSs are HKD 0.357/0.417/0.494. Based on our residual income valuation model, we adjust a TP of HKD 5.07, corresponding to FY19/FY20/FY21 14.21x/12.14x/10.26x PE with a +37.69% potential upside compared with CP of HKD 3.68 as of August 23, 2019, we maintain ¡§BUY¡¨ investment rating.

Risk

1. Fail expectations of project progress

2. Policy risk of electricity price allowance

3. Fail expectations of acquisition of new projects

Financials

Click Here for PDF format...