Investment Summary

The revenue in H1 was RMB 1.49 bn, up by 16.1% YoY; the net profit attributable to owners was RMB 109.6 mn, down by 35.4% YoY. The revenue growth in ERP business and Cloud services were 1.2% (below our previous estimate) and 54.9% (in line with our previous estimate). We give a TP of $8.55, downgrading to ¡§Buy¡¨ recommendation, with 10.3% potential upside. (Closing price at 20 Aug 2019)

Result update

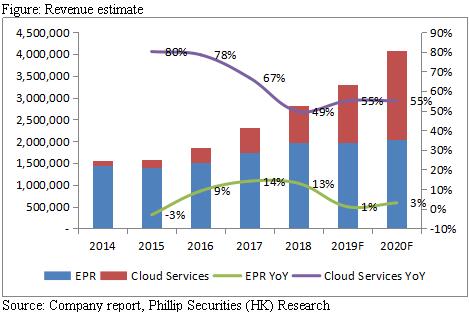

The revenue in H1 was RMB 1.49 bn, up by 16.1% YoY; the net profit attributable to owners was RMB 110 mn, down by 35.4% YoY. The revenue growth in ERP business and Cloud services were 1.2% (below our previous estimate) and 54.9% (in line with our previous estimate). The GPM dropped from 80.2% to 79.5%. The selling & marketing expenses and research & development cost as pct of revenue increased to 51.4% and 17% respectively, due to the increase in marketing and promotion expenses as well as research and development costs in cloud products. The proportion of cloud service to revenue grew from 27.8% in 18H1 to 37% in 19H1.

Business ERP

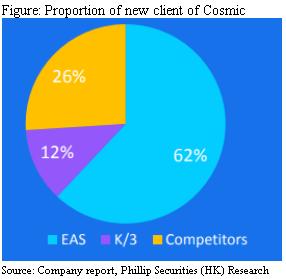

The revenue growth from ERP business in 19H1 was 1.2%, lower than our previous estimate 3%. As we mentioned in previous report, we believe the drop in the growth of traditional ERP were 1) the clients delay or reduce its IT expenditure due to the concern on the economic downturn in the first half and 2) the demand of traditional ERP is shifting to Cloud services. 62% and 12% of the cosmic clients are from EAS and K/3, implying that some of the demand on ERP business has been shifted to Cloud services. Also, the management said they will start to encourage their EAS clients moving to Cosmic in the next few year. As a result, we are more conservative on the prospective of the ERP business as the Group place more emphasis on Cloud services.

Cloud service

Cosmic

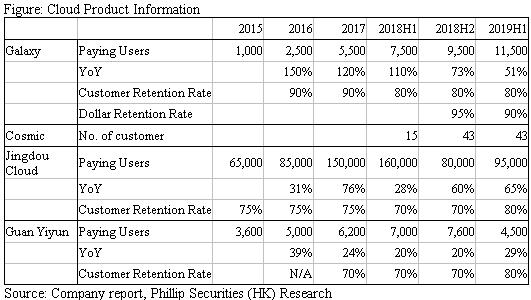

Cosmic has acquired 28 new clients in 19H1, where the total contract size reached RMB 33mn, representing an average contract size of RMB 1.2 mn. Their new clients included Xiamen C&D, Hesteel Group, Xiwang Group and etc. Only RMB 15 mn was recorded in the first half from Cosmic, while the other has been included in contract liabilities. The Group has started its ISV partner plan on the platform of Cosmic in order to create a PaaS ecosystem. The number of verified ISV reached about 50 and expect to be more 100 in the end of 2019. There will still be a huge investment in cosmic, so it is expected a few year will be needed for breakeven.

Galaxy

Galaxy was doing well in the first half, where its customer exceeded 11,500, and 90% of it are new customers, representing a YoY increase of 50%. It has acquired some renowned clients, such as Tencent, Alibaba, Samsung, Huawei and etc. Also, 77% of the new customers are new ERP users and 13% of which are from competitors. The dollar retention rate remained high, at 90%. Galaxy raised its price in this July. The management claimed that the net loss incurred from Galaxy is reducing, only incurred a net loss of RMB 10 mn, and should be able to breakeven in the second half of 2019.

Earnings forecast

In view of the dropped growth in ERP business for the first half, we expect the revenue growth of ERP business will be 1%/3% in 2019F/20F. Besides, we also expect the revenue growth of cloud business will be 55% for both 2019F/20F, as we are optimistic to the SaaS market.

Valuation

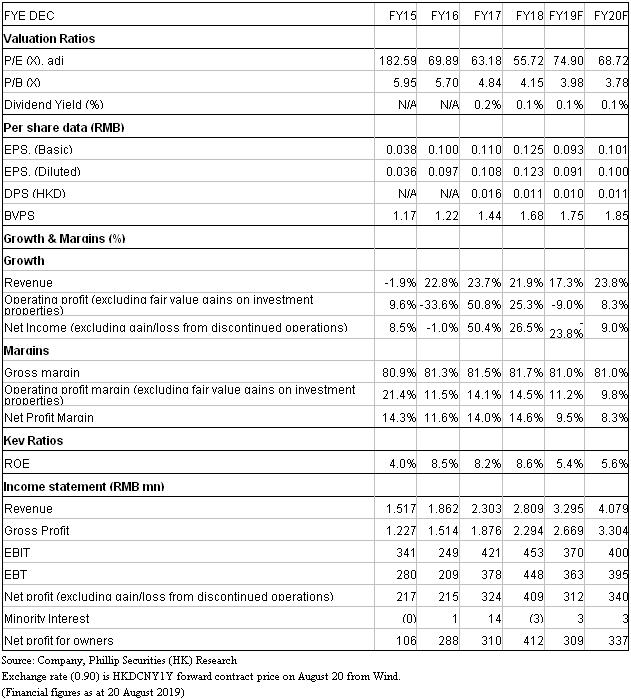

We adopted sum of the parts valuation by dividing the business into three parts: 1) Traditional ERP business (P/E), 2) Cloud business (P/S), and 3) Investment real estate business (book valuation). We forecast the earnings per share of the traditional ERP business in 2019F to be RMB 0.106, 2.8% lower than the previous estimate in reflection of the slower growth in the first half, with target PE ratio 15x; the revenue of cloud services per share in 2019F would be RMB 0.397, 3.1% higher than the previous estimate in reflection of the strong growth. We maintain the target PS ratio to be 13x; for the investment real estate business, the book valuation is used, and the valuation per share is RMB 0.55. Finally, a net cash is RMB 0.26 per share in 2018. A target price of HK$8.55 was derived, 3.9% lower than previous target price. As the stock price has rebounded recently, we downgrade to ¡§Accumulate¡¨ recommendation, with 10.3% potential upside. (HKD/CNY: 0.90)

Risk

1. Slower-than-expected growth in cloud products

2. The economy of China slows down

3. Cloud ERP may take away the existing customers of traditional ERP, particularly SME

Financials

Click Here for PDF format...