Investment Summary

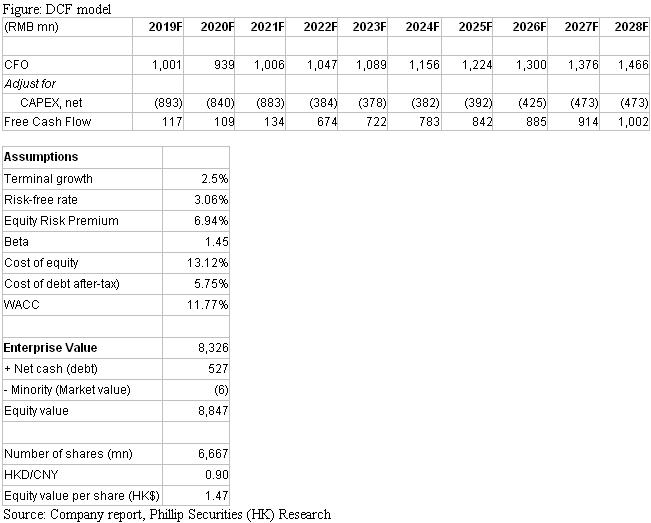

Hope education is one of the largest private higher education group in China, engaging in the bachelor program, junior college program and vocational education. They currently operate four independent colleges, five junior colleges and one technical college in Sichuan, Guizhou and Shanxi. As of the 2018/19 school year, the number of student enrollment was around 95,000. Based on DCF valuation, we derived a target price of HK$1.47, implied a P/E of 21.5x and 17.6x in 2019/20F. We initiate a ¡§Buy¡¨ rating with a 24.6% potential upside. (Closing price at 6 Aug 2019)

The private higher education market will be under pressure in short term, but will soar in long term

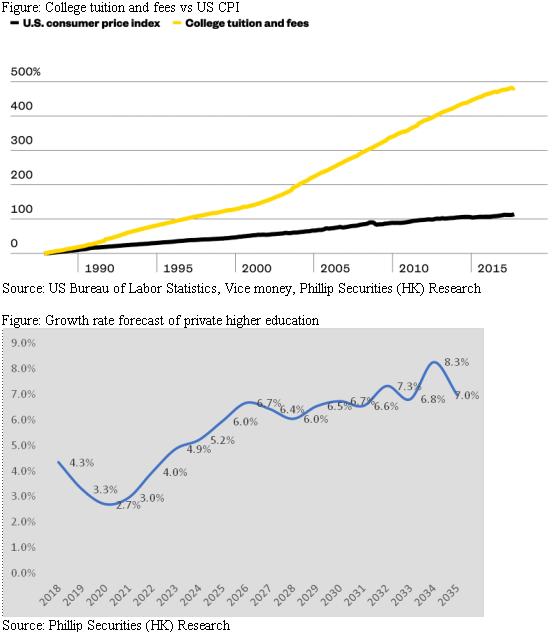

The population of the relevant age group in higher education will drop since 2020, and stabilize in 2025. As the GDP per capita in China increases, we should see gross enrollment rate in China catches up with the developed countries in the future. The penetration rate of private education will increase thanks to the rising acceptance in private universities and the dependence on private education form local governments. The tuition fee should grow with the CPI in China. Regarding those four factors where three are rising, whereas one is dropping in the short term and will rebound in long term, we expect the growth rate of private higher education will decrease from 2018 to 2020E, and will reach a mid to high single-digit growth.

Abundant capacity for enrollment expansion in higher vocational education

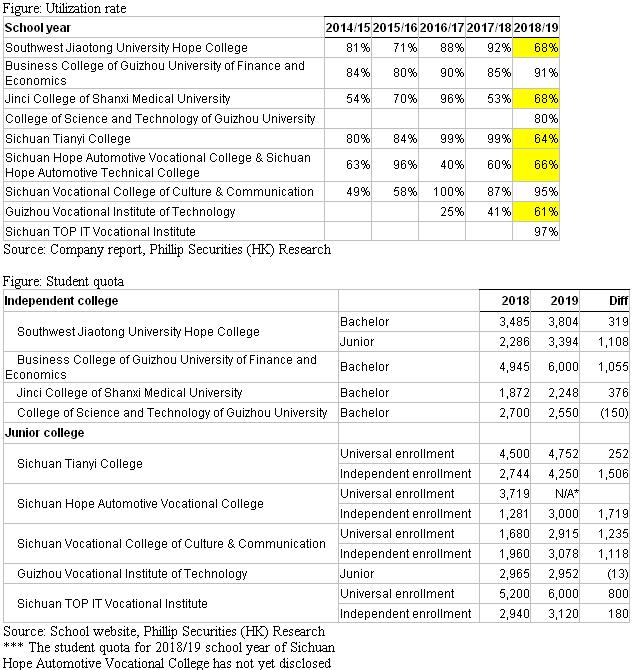

As of 2018/19 school year, the capacity of the schools reached 125,096, implying a utilization rate of 76%. Even if there is no increase in capacity, the schools could still accommodate 30,000 more students. As the junior college should be the beneficiary in this expansion, having a closer look at the utilization rate, the utilization rate of Jiaotong College, Tianyi College, Automotive Vocational College, Vocational Institute of Technology and Automotive Technical College which offers junior college educations (the beneficiary in this expansion) were all below 70% in the 2018/19 school year. As a result, the Group should be able to enjoy such enrollment expansion.

Decent quality of teaching protects from the drop in population of relevant age group

According to Chinese independent college and private university ranking (Wu Shulian) in 2018, Guizhou College and College of Technology are ranked the first and the second in Guizhou. the department of administration management of Jiaotong College ranked 10% - 20% out of 256 schools who offering administration management. The medical department of Shanxi College ranked 20% - 30% out of 62 schools providing medical study.

The department of administration management and economics of Guizhou College both ranked 10% - 20% out of 256 and 215 schools. The department of economics of College of Technology ranked 20% - 30% out of 215 schools. We believe those schools are with a decent quality of teaching, giving their protection once the student enrollment decreases.

Excellence in school integration

Shanxi College, Tianyi College and College of Culture & Communication have shown how good the Group was in school integration. Shanxi College grew at a 5-year CAGR of 25.1%; Tianyi College grew at an 8-year CAGR of 5.7%; College of Culture & Communication grew at a 5-year CAGR of 30.6%.

Company analysis

Company profile

Hope education is one of the largest private higher education group in China, engaging in the bachelor program, junior college program and vocational education. They currently operate four independent colleges, five junior colleges and one technical college in Sichuan, Guizhou and Shanxi. As of the 2018/19 school year, the number of student enrollment was around 95,000.

Schools

1. Southwest Jiaotong University Hope College (Jiaotong College)

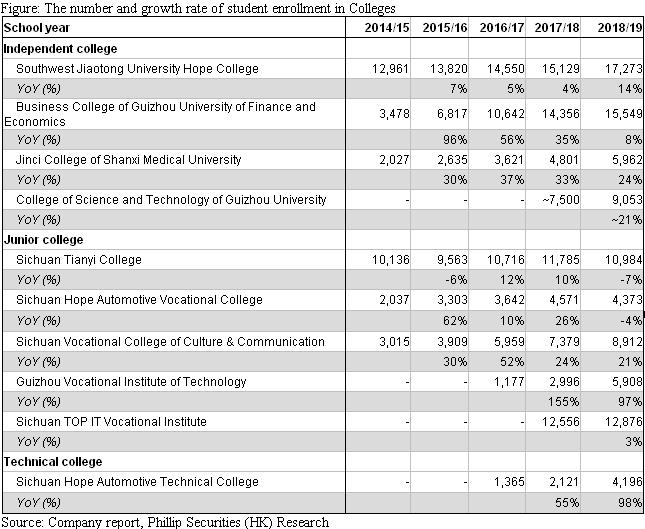

Cooperating with Southwest Jiaotong University, Jiaotong College is an independent college located in Sichuan providing formal undergraduate and junior college educations. It offered 44 majors primarily including urban rail transportation operation management, civil engineering, business and foreign languages, engineering management, electronic engineering and automation and e-commerce. Among the 44 majors, 25 are majors granting bachelor's degrees and 19 are majors granting junior college diplomas. Having two campuses in Chengdu and Nanchong, the school had 17,273 students enrolled in the 2018/2019 school year.

Jiaotong College pays an annual fee amounting to 15% of its tuition income and 5% of its scientific research income to Southwest Jiaotong University. The term of the cooperation agreement is 30 years, ended in 2039.

2. Business College of Guizhou University of Finance and Economics (Guizhou College)

Cooperating with Guizhou University of Finance and Economics, Guizhou College is an independent college located in Guizhou providing formal undergraduate education. It offered 13 majors granting bachelor's degrees including economics, accounting, management, science, engineering, literature and legal studies. Having a campus in Huishui, the school had 15,549 students enrolled in the 2018/2019 school year.

Guizhou College pays an annual fee amounting to 30% of tuitions. The term of the cooperation agreement is 30 years to 2044.3. College of Science and Technology of Guizhou University (College of Technology)

Cooperating with Guizhou University, College of Technology is an independent college located in Guizhou providing formal undergraduate education. It offered 25 majors granting Bachelor's degrees including literary, law and public management, engineering, business, and art. Having a campus in Huishui, the school had 9,053 students enrolled in the 2018/2019 school year.

College of Technology pays an annual fee amounting to 25% of the tuition. The term of the cooperation agreement is ended in 2034.

4. Jinci College of Shanxi Medical University (Shanxi College)

Cooperating with Shanxi Medical University, Shanxi College is an independent college located in Shanxi providing formal undergraduate education. It provided 10 majors granting Bachelor's degrees including clinical medicine, preventive medicine, dentistry, pharmaceutics, forensic medicine, nursing, public affairs management, information management and information system. It had one campus in Qixian and leased one campus in Taiyuan. For the 2018/2019 school year, the school had 5,962 students enrolled.

Shanxi College pays an annual fee amounting to 20% of the tuition. The term of the cooperation agreement is 30 years to 2044.

5. Sichuan Tianyi College (Tianyi College)

Tianyi College is a higher education institution located in Sichuan providing a junior college education. It had one campus in Mianzhu. It offered 21 majors granting junior college diplomas including tourism management, language and literature, art and design, civil engineering, computer science and technology, businesses, accounting, aviation and nursing. For the 2018/2019 school year, the school had 10,984 students enrolled. It also operates a ¡§junior college-undergraduate¡¨ program.

6. Sichuan Hope Automotive Vocational College (Automotive Vocational College)

Automotive Vocational College is a higher education institution located in Sichuan providing a junior college education. It offered 19 majors granting junior college diplomas including automobile engineering, automobile advanced technology, mechanical and electrical engineering, management engineering, automobile marketing and service and e-commerce and accounting. It had one campus in Ziyang. For the 2018/2019 school year, the school had 4,373 students enrolled. It also operates a ¡§junior college-undergraduate¡¨ program.

7. Sichuan Vocational College of Culture & Communication (Vocational College of Culture & Communication)

Vocational College of Culture & Communication is a higher education institution located in Sichuan providing junior college education and serving as a leading cultivation base of talents in television and aviation communication. It provided offered 27 majors granting junior college diplomas including an art performance, film and television, art and design, culture management, electronic information and aviation services. It had one campus in Chongzhou and leased part of Sichuan Tianyi College's campus in Mianzhu to accommodate its increasing student enrollment. For the 2018/2019 school year, the school had 8,912 students enrolled. It operates a ¡§junior college-undergraduate¡¨ program.

8. Guizhou Vocational Institute of Technology (Vocational Institute of Technology)

Vocational Institute of Technology is a higher education institution located in Guizhou providing a junior college education. It provided 18 majors granting junior college diplomas including accounting, automobile testing, e-commerce, automobile marketing and applied chemistry engineering. It had one campus in Fuquan. For the 2018/2019 school year, the school had 5,908 students enrolled.

9. Sichuan TOP IT Vocational Institute (TOP IT Vocational Institute)

TOP IT Vocational Institute is a formal higher education institution located in Sichuan providing junior college education and serving as a leading cultivation base of talents in information technology. It offered 35 majors granting junior college diplomas including software technology, big data technology and application, mobile application development, computer network technology, accounting, automotive testing and maintenance technology and e-commerce. The school had a campus in Chengdu. For the 2018/2019 school year, the school had 12,876 students enrolled.

10. Sichuan Hope Automotive Technical College (Automotive Technical College)

Sharing the same campus with Automotive Vocational College, Automotive Technical College offered 18 majors, including applied technology of numerical control, automobile maintenance, accounting, applied computer science, comprehensive management of the rural economy, e-commerce and automobile marketing of vehicles and accessories. For the 2018/2019 school year, the school had 4,196 students enrolled.

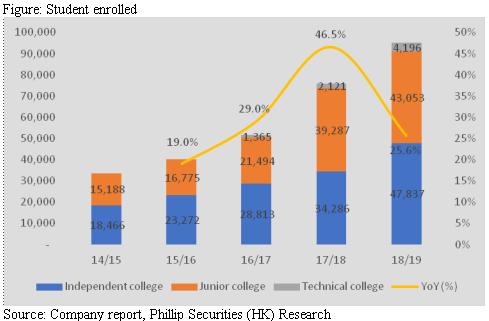

Student enrolled

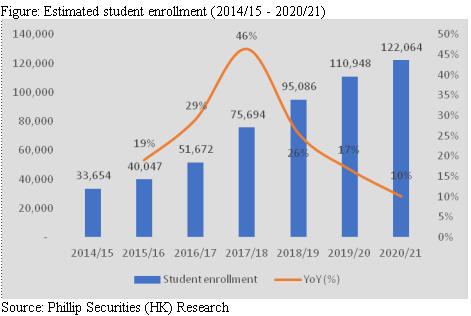

The student enrollment increased from 33,654 in 14/15 school year to 95,086 in 18/19 year. The growth rate in 15/16-18/19 school year were 19.0%, 29.0%, 46.5% and 25.6%, with a CAGR of 29.6%. As of 18/19 school year, the student from independent college accounted for 50.3%, while that from junior college and technical college were 45.3% and 4.4%.

Independent college: Jiaotong College is a mature school with a 5-year CAGR of 7.4%. Guizhou College and Shanxi College are both staying in a fast-growing stage, with a 5-year CAGR of 45.4% and 31.0% respectively. Besides, College of Technology was also in an expanding period, where the website of College of Technology stated that the student enrollment in 2017/18 school year was around 7,500, implying a YoY increase of 20.7%.

Junior college: Automotive Vocational College, College of Culture & Communication and Vocational Institute of Technology were all enjoying robust growth, with a CAGR of 21.0%, 31.1% and 124.0% respectively. To the update to a bachelor degree program, Tianyi College stopped its growth in student enrollment, only recorded a 5-year CAGR of 2% to fulfil the requirement from government. TOP IT Vocational Institute also recorded slow growth in student enrollment, up by 3% in 2018/19 school year.

Technical College: Automotive Technical College was also enjoying robust growth, with a 3-year CAGR of 75.3%.

School Capacity

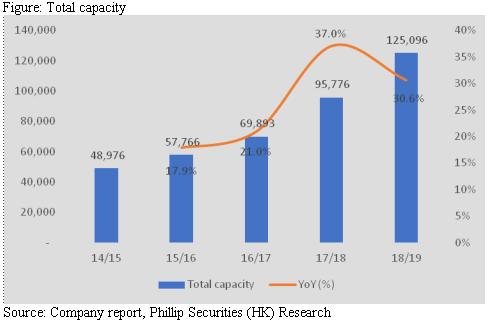

The capacity has been growing from 48,976 in 2014/15 school year to 125,096 in 2018/19 school year with a 5-year CAGR of 26.4%.

Tuition fee

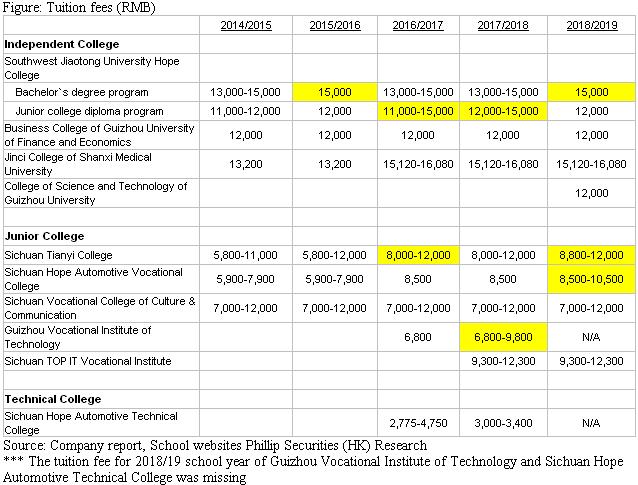

In 2018/19 school year, the tuition fees of independent colleges are ranging from RMB 12,000 to 15,000, while that of tuition fees for junior colleges are from RMB 7,000 to 12,300 without considering Vocational Institute of Technology. The tuition fees of technical college are the lowest, ranging from RMB 3,000 to 3,400 in 2017/18 school year.

Financial performance

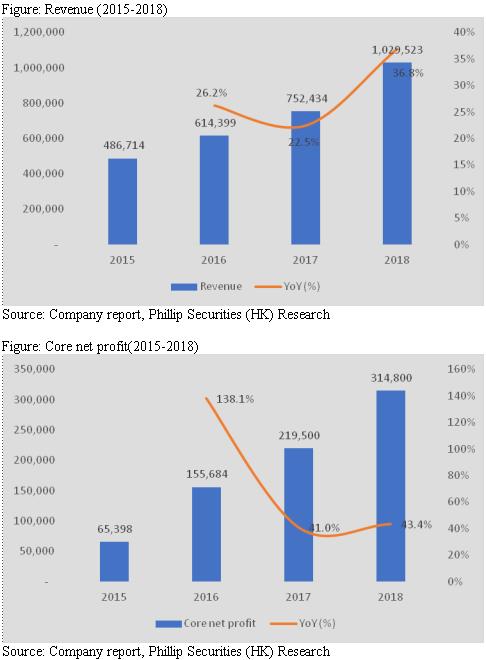

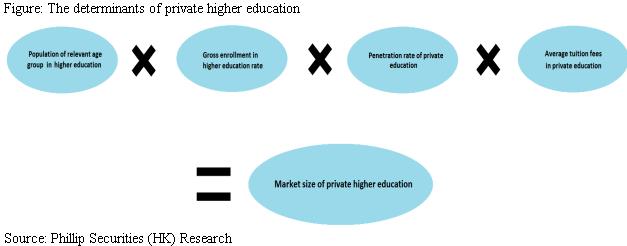

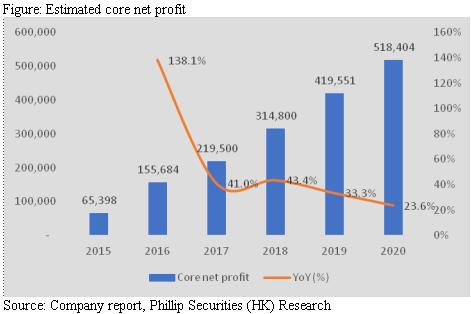

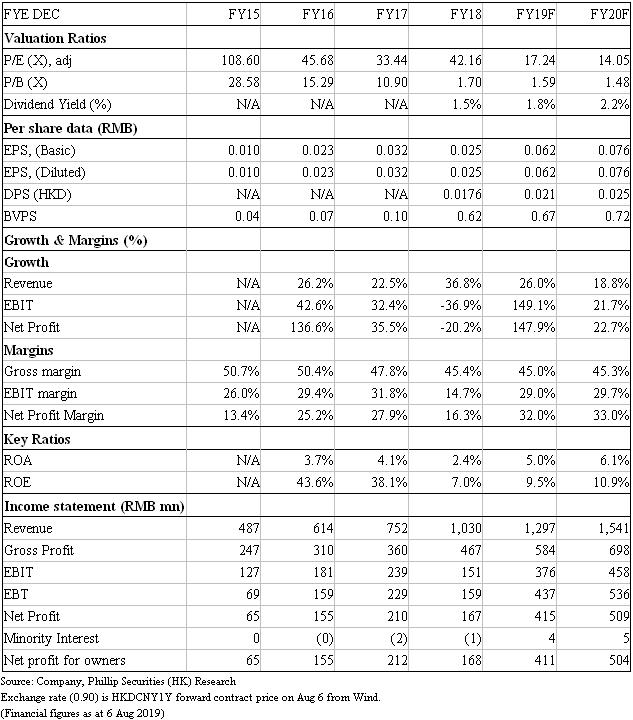

The revenue and core net profit (excluding listing expenses, equity-settled share option expenses and gain on exchange differences net) remains a strong growth in the last three years and reached RMB 1,029.5 million and RMB 314.8 million in 2018 respectively.

Industry overview

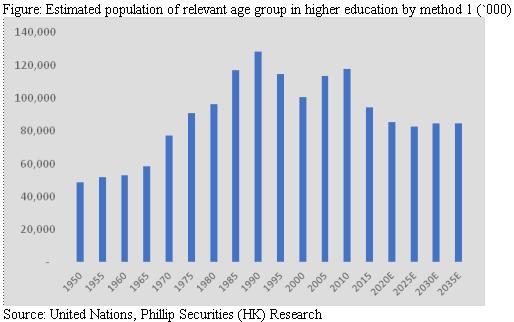

The market size of private higher education consists of four factors: 1) Population of the relevant age group in higher education, 2) Gross enrollment rate in higher education, 3) Penetration rate of private education and 4) Average tuition fees in private education.

Population of relevant age group in higher education

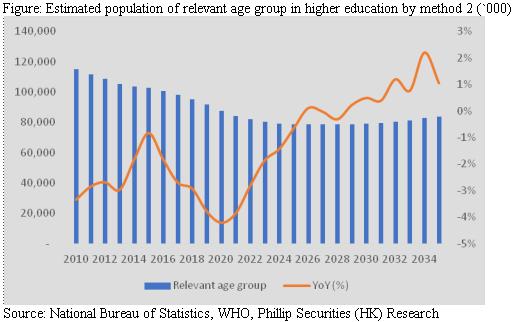

We estimate the future population of the relevant age group by two methods: 1) the age group in 2020E estimated by the United Nations as well as 2) the birth rate across the years in China.

1) The age group in 2020E estimated by United Nations

We first estimated the age group of 15-19 and 20-24 by calculating how the younger age group will be promoted to those two age group after adjusting the mortality rate. Then, since the population of the relevant age group in higher education is ranging in age from 18 to 22 years old, to simplify the estimate, we weighted 40% for the age group of 15-19 (age 18 & 19) and 60% for that of 20-24 (age 20, 21 &22).

Based on the population estimate in 2020E from United Nations, we see the relevant age group in 2020E/2025E will drop by 9.5%/3.1%, but then rise by 2.1%/0.2% in 2030E/2035E. The population of the relevant age group should be stabilized in 2025E.

2) The birth rate across the years in China

The birth rate is calculated by the number of newborns divided by the average population in the corresponding year. With the total population in China, we estimated the number of newborns. Based on the mortality rate of WHO from ages 0 to 24 in 2016 (~1.4%), we forecast the number of population aged from 18 to 22 by our estimated number of newborns.

We see the population of relevant age group will continue to drop at a decreasing rate since 2020, then will stabilize in 2025, finally rally in 2030.

Those two methods produced similar results that the population of the relevant age group in higher education will drop from 2020E to 2025E. While the method 1 suggested the population of relevant age group will rebound from 2025E to 2030E and stabilize from 2030E to 2035E, the method 2 gives an opposite view that the population of relevant age group will stabilize from 2025E to 2030E and rebound from 2030E to 2035E.

Gross enrollment rate in higher education

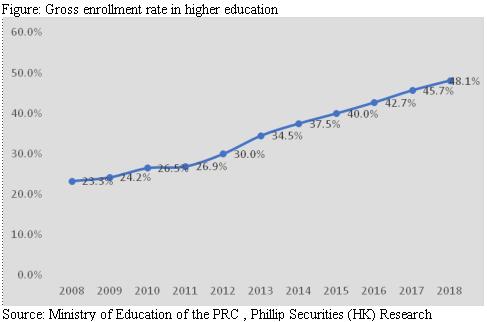

The gross enrollment rate in higher education has been rising from 23.3% in 2008 to 48.1% in 2018. In the 13th Five-Year Plan for the Development of National Education, the government aims to reach 50% in the gross enrollment rate of higher education in 2020. And, on 30th April, the State Council of the PRC announced an enrollment expansion in higher vocational education by 1 million. The Ministry of Education claimed the gross enrollment rate could reach 50% in 2019, one year earlier than the target. To make higher education more accessible, we believe the gross enrollment rate should keep surging in the future.

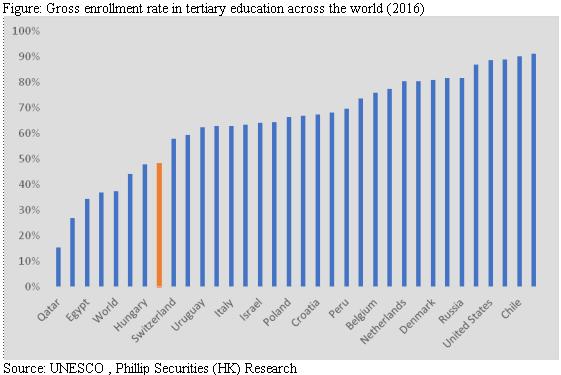

The gross enrollment rate in tertiary education in China was still lower than the most of the developed countries, such as Spain, United State, Netherlands, Germany, Canada and the United Kingdom, showing there is still room for the growth of gross enrollment rate in tertiary education in China. As the GDP per capita in China increases, we should see China catches up with the developed countries in the future.

Penetration rate of private education

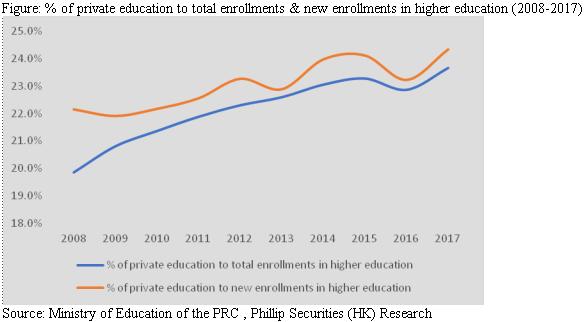

The popularity of private higher education in China has been rising, measured by both the percentage of private education to total enrollments & new enrollments in higher education. The % to total enrollments increased from 19.9% in 2008 to 23.7% in 2017 and that to new enrollments also rose from 22.2% in 2008 to 24.3% in 2017. We believe the surging penetration rate is due to the rising attractiveness of private education institutions.

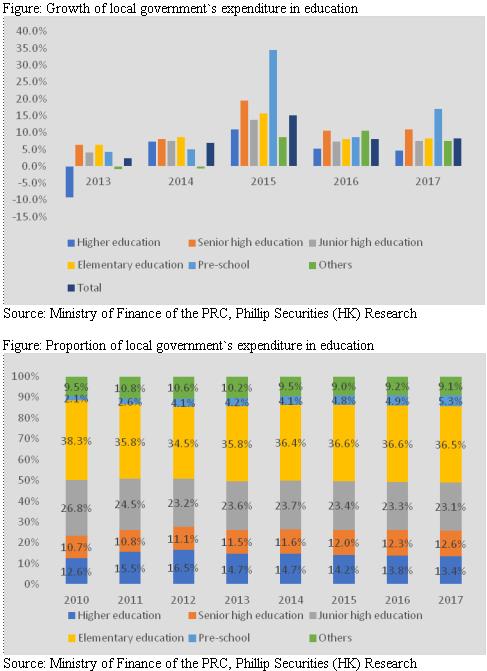

In addition to the rising attractiveness, the dependence of the local government on private higher education was also a reason for the rising penetration rate. The central government aims to make higher education more accessible, handing a target on gross enrollment rate to local government. However, the growth of local government's expenditure on higher education was generally lower than the aggregate expenditure, except in 2014; the proportion of the expenditure in higher education to the aggregate was dropping since 2013. To fulfil the target from the central government but with less expenditure, the local government can only depend on the private education institutions, driving the penetrating rate up.

Therefore, we expect the penetrating rate should be rising if the local government's expenditure on higher education is left behind.

Average tuition fees in private education

According to Frost & Sullivan, the average tuition fees in private higher education in 2017 was RMB 11,533. The tuition fees are generally adjusted with the Inflation rate. We expect the tuition fees will increase at 2.5% annually (the average of CPI in China in the last ten years). In fact, the data shows the growth in tuition fee is stronger than that in inflation in the US. As a result, we believe growth at an inflation rate is a relatively conservative assumption.

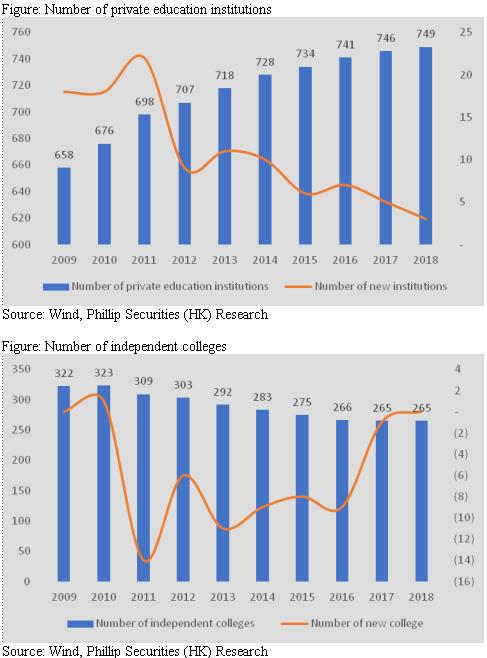

Supply of private higher educationThe number of private education institute has increased slowly, around 10 new institutions founded annually in the last decade. The slow growth in private education institutions could be attributed to its heavy asset business model, where schools offering bachelor program need at least 500 Mu (equivalent to 333,333 sq.m.) land use rights to construct teaching and ancillary buildings and facilities. Besides, the government urged the independent colleges to separate from its original public universities. The private education schools may decide to acquire those independent colleges rather than building it from scratch, can change it to private universities. Therefore, the number of new schools has decreased recently. As of 2018, since there are still 265 independent colleges for acquisition, we expect the number of new schools will remain at a low level.

Policy risk in the industry

Although the Amendment of Law for Promoting Private Education of the PRC has not been revealed, we believe the policy risk in higher education is lower, compared to compulsory education. On November 2016, the 12th National People's Congress proposed the Regulations for Classification Registration of Private School - for-profit and non-profit, where it indicates that compulsory education can only be non-profit. For those non-profit schools, the profit can only leave in schools for further development and do not allow to distribute to the owners. Although listed companies offering compulsory education currently could distribute dividends by making use of related party transactions to transfer its profit, we believe that such practices are likely to be rectified in the future because non-profit schools do not pay taxes on tuition fees, which lead to the unfairness. In contrast, higher education can choose for-profit, meaning the company could distribute dividends after paying taxes and land transfer fees. Besides, as education is one of the industries that the state encourages for development, the market generally believes that profits tax is likely to be only 15%. The land transfer fees can be amortized into 50 years, so the impact on the income statement should be not significant.

Enrollment expansion in higher vocational education

In the Report on the Work of the Government in 2019, it suggests an enrollment expansion in higher vocational education by 1 million to resolve the lack of technical manpower and structural unemployment in China. The expansion mainly faces to graduates from senior high school and secondary technical vocational school, veterans, migrant workers, laid-off workers. We believe the enrollment expansion will significantly the gross enrollment rate in higher education. The denominator of gross enrollment rate is the population aged from 18 to 22; whereas the numerator is the number of students studying in higher education whom age could be over 22. Therefore, since this expansion is facing those veterans, migrant workers, laid-off workers, whom age may have already been over 22, the gross enrollment rate could enjoy a significant boost.

Company highlights

Abundant capacity for enrollment expansion in higher vocational education

For new student enrollment, the Ministry of Education in province assign a student quota to every school, where the quota is usually taking consideration of the capacity and the education quality of the school. Higher vocational education will expand its enrollment by 1 million this year, as the Ministry of Education in the province should assign more student quota to schools, especially those with abundant capacity.

As of 2018/19 school year, the capacity of the schools reached 125,096, implying a utilization rate of 76%. Even if there is no increase in capacity, the schools could still accommodate 30,000 more students. As the junior college should be the beneficiary in this expansion, having a closer look at the utilization rate, the utilization rate of Jiaotong College, Tianyi College, Automotive Vocational College, Vocational Institute of Technology and Automotive Technical College which offers junior college educations (the beneficiary in this expansion) were all below 70% in the 2018/19 school year. As a result, the Group should be able to enjoy such enrollment expansion.

The student quota in 2019 has increased hugely, such as Southwest Jiaotong University Hope College, Sichuan Tianyi College, Sichuan Hope Automotive Vocational College, and Sichuan Vocational College of Culture & Communication, reflecting those schools should be enjoying from enrollment expansion in higher vocational education this year.

Decent quality of teaching

Good quality of teaching is one of the most crucial competitive advantages for a school. Once the population of the relevant age group, the schools with a poor quality of teaching will suffer the first. Therefore, it is important to investigate the quality of teaching when analyzing an education company. As the schools of the Group were all located in those less developed provinces, its quality of teaching is generally poor than those schools in developed provinces, making the ranking in China of the schools of the Group less impressive. Indeed, we believe it is more appropriate to compare the schools within the province since most of the student enrolled are from the local province.

According to Chinese independent college and private university ranking (Wu Shulian) in 2018, Guizhou College and College of Technology are ranked the first and the second in Guizhou. Jiaotong College ranked the eleventh out of fourteen in Sichuan and Shanxi College ranked the last in Shanxi.

Although Jiaotong College and Shanxi College may not impressive in terms of the overall ranking in the province they are located, it is also important to investigate the majors they are providing individually, because schools maybe only provide a good quality of teaching in some of their majors. As a result, the overall ranking of those schools may look bad.

According to Chinese independent college and private university ranking (Wu Shulian) in 2018, the department of administration management of Jiaotong College ranked 10% - 20% out of 256 schools who offering administration management. The medical department of Shanxi College ranked 20% - 30% out of 62 schools providing medical study. The department of administration management and economics of Guizhou College both ranked 10% - 20% out of 256 and 215 schools. The department of economics of College of Technology ranked 20% - 30% out of 215 schools.

We believe Guizhou College and College of Technology are regarded with good quality of teaching in Guizhou due to their leading position in the ranking in Guizhou. Although Jiaotong College and Shanxi College did not rank as high as the schools in Guizhou, they have their strength in some of the majors, such as administration management and economics. Therefore, we believe those schools are with a decent quality of teaching, giving their protection once the student enrollment decreases.

Excellence in school integration

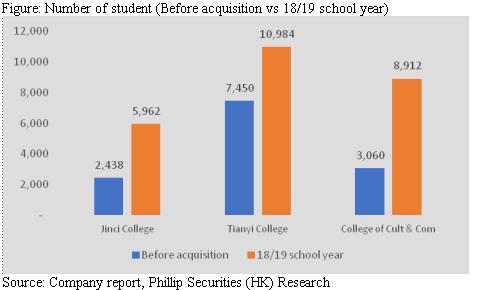

The Group developed depending on acquisitions in the last few years, where 7 out of 10 of schools are from acquisitions. As a result, the capacity to integrate the acquired schools is of utmost importance. Shanxi College, Tianyi College and College of Culture & Communication have shown how good the Group was in school integration.Shanxi College: Founded in 2002, the school was acquired in 2014. The Group received 2,438 students then enrolled at. In 2018/19 school year, the student enrolled has increased to 5,962, meaning a 5-year CAGR of 25.1%.

Tianyi College: Founded in 1991, the school was acquired in 2011. The Group received all 7,450 students then enrolled at. In 2018/19 school year, the student enrolled has increased to 10,984, reflecting an 8-year CAGR of 5.7%. The student enrollment stabilized in recent year, to update from junior college education to undergraduate education. Otherwise, the growth in a student could be stronger.

College of Culture & Communication: Founded in 2005, the school was acquired in 2014. The Group received all 3,060 students then enrolled at. In 2018/19 school year, the student enrolled has increased to 8,912, reflecting a 5-year CAGR of 30.6%.

With enriched resource, the Group can increase the capacity of those acquired schools by building a new dormitory and school building. Besides, the synergy can be created after being acquired by the Group. Tianyi College and College of Culture & Communication both operated a ¡§junior college-undergraduate¡¨ program with Jiaotong College, which could enhance the attractiveness and the acceptance of their courses.

Low gross enrollment rate in higher education in provinces located

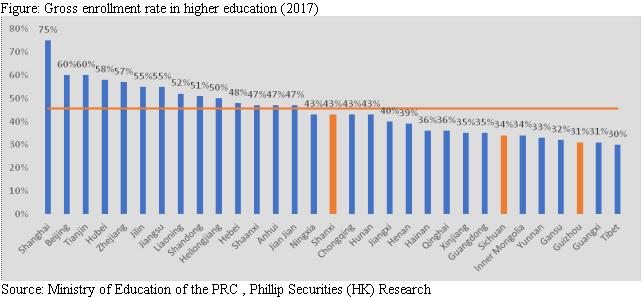

The schools of the Group are all located in Sichuan, Guizhou and Shanxi. Moreover, most of their new student enrolled are from the local province, so it is helpful to look into the gross enrollment rate in each province. In 2017, the gross enrollment rate in higher education in Sichuan, Guizhou and Shanxi were 34%, 31% and 43%, versus 45.7% (the overall in China). It shows that the gross enrollment rate in Sichuan and Guizhou were still far behind the overall.

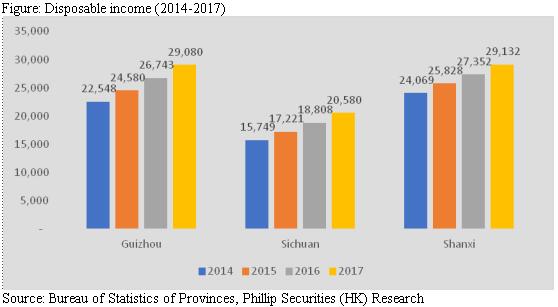

As those less developed provinces become richer, we should see the gross enrollment rate improves, because the residents are affordable for higher education. The disposable income of Guizhou, Sichuan and Shanxi have risen in a 4-year CAGR of 8.9%, 9.3% and 6.6%. In the 13th Five-Year Plan for the Development of Education in Sichuan Province, it targets the gross enrollment rate in higher education to reach 50% in 2020, reflecting how eager are those less-developed provinces to improve their education level.

Earnings forecast

Student enrollment

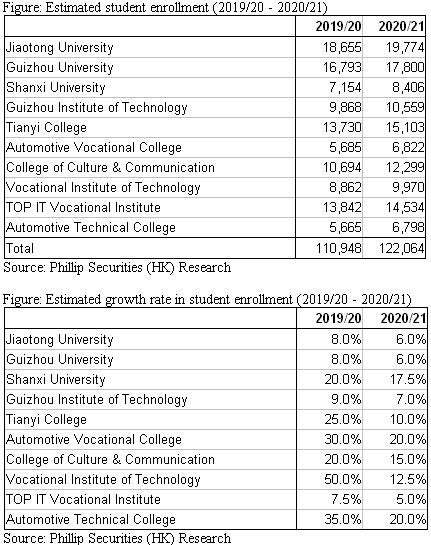

We expect there will be a significant surge in the school year 2019/20 thanks to the enrollment expansion in higher vocational education, and the growth in the school year 2020/21 should resume normal. We expect to see the student enrollment to reach 110,948 and 122,064 in the school year 2019/20 and 2020/21, implying a 7-year CAGR of 24%.

Tuition fee

We assume the average tuition fee per student grows at 2.5%, in line with the average of CPI in China in the last ten years and lower than the guidance from management (3%-5%) for the sake of being conservative.

Revenue

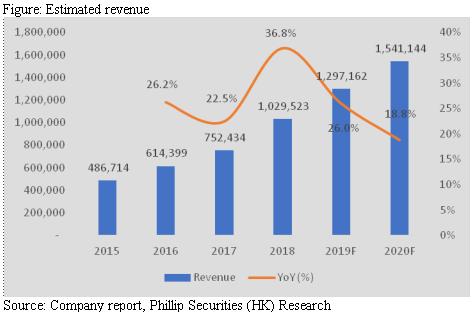

We expect the revenue in 2019F/20F will grow by 26.0%/18.8%. The significant increase in 2019F was partly attributed to the consolidation of the College of Science and Technology of Guizhou University.

GPM

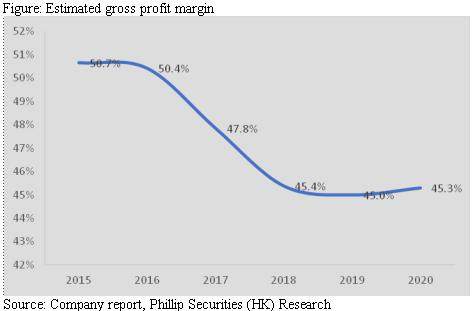

We expect the GPM in 2019F will drop to 45% due to the consolidation of the College of Science and Technology of Guizhou University. Then, it will rise to 45.3% in 2020F as the operating performance improves.

SG&A costs

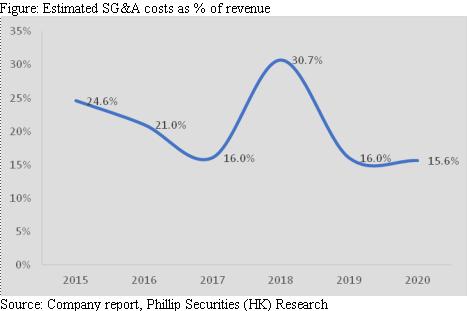

The SG&A costs as % of revenue in 2018 rose due to the listing expenses and the equity-settled share option expenses. We expect the SG&A will resume to a normal level. Moreover, as the operation performance is improving, the proportion should slightly decrease. We forecast the SG&A costs as % of revenue in 2019/20F will be 16%/15.6%.

Core net profit

Based on the assumptions above, we expect the core net profit will reach RMB 420/518 mn, with a growth of 33.3%/23.6% in 2019F/20F.

Valuation

We adopted the DCF model for valuation, where we assume the discount rate to be 11.74%, and terminal growth to be 2.5%, with FCFF forecast to 2028F. We derived a target price of HK$1.47, implied a P/E of 21.5x and 17.6x in 2019F/20F. We initiate a ¡§Buy¡¨ rating with a potential upside of 24.6%. (HKD/CNY=0.90)

Risk

1. A plunge in birth rate in China

2. The enrollment expansion cannot bring growth in the number of students

3. A sharp change in policies to education sector

4. The Group fails to improve the operation of the acquired schools

Financials

Click Here for PDF format...