|

WUXI BIO(2269)

Analysis¡G

According to the positive profit alert of WUXI Biologics (2269), it is expected that the profit attributable to shareholders of the Company for the six months ended June 30, 2019 will increase more than 78% compared with the corresponding period of last year. The increase is primarily due to: (i) leading technology platform, competitive timeline and strong execution track record contributing to more market share and new integrated projects being added to the Group`s pipeline; (ii) the Group`s innovative proprietary technology platforms, including but not limited to the bispecific antibody technology platform WuXiBody™, have been more adopted in the industry; (iii) strong growth in revenue, as a result of the success of the Group`s¡§Follow-the-Molecule¡¨strategy; (iv) improvement of operational efficiency; and (v) other non-operating income recorded. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $75.5, Target Price: $82.00, Cut Loss Price: $71.00

|

CONCORD NE(182)

Analysis¡G

In the first half of 2019, the Company materialized a total income of RMB 963,349,000 (1H 2018: RMB809,609,000), accounting for 19.0% increase for the same period of last year. Profit attributable to equity holders of the Company amounted to RMB399,232,000 (1H 2018: RMB275,713,000), representing 44.8% increase for the same period of last year. The basic earnings per share were RMB4.75 cents (1H 2018: RMB3.21 cents). In the first half of 2019, the Company`s principal power generation business robustly grew with high safety and efficiency, power generation output and profit were both higher than expected. All new businesses such as Energy IoT, intelligent operation & maintenance (¡§O&M¡¨), energy storage and financing lease were speedily propelled as planned. Beneficial from accurate research and judgement for new energy policy, the Company gained well in respect of resources storage and project approval, which underlain the development this year and next. In addition, via capital operation between international clean energy funds, the Company developed a new business model that provided the industrial funds with management services that unified development and operation for new energy projects.

Strategy¡G

Buy-in Price: $0.360, Target Price: $0.460, Cut Loss Price: $0.345

TerraSky Corporation (3915.JT)

Established in 2006. Comprised of the solutions business in the Salesforce and AWS (Amazon Web Service) cloud systems, and the products business that provides cloud services domestically and overseas as an SaaS vendor. For 1Q (Mar-May) results of FY2020/2 announced on 12/7, net sales increased by 41.1% to 2.124 billion yen compared to the same period the previous year, and operating income returned to profit at 160 million yen from ¡¶27 million yen the same period the previous year. In their solutions business, results from the implementation of their cloud service exceeded a total of 4,000 cases, and in their products business, big project orders and a growth in the number of contracted companies / amount of money have contributed. For FY2020/2 plan, net sales is expected to increase by 31.7% to 8.634 billion yen, and operating income to increase by 96.1% to 246 million yen. Their Salesforce-collaborative groupware, ¡§micoto¡¨, has begun usage in an insurance revision head office for the purpose of internal communication and a move to paperless. The groupware that promotes work efficiency and the software equipment investment plan show signs of an increase in amount, and we can look forward to profit stabilisation from the increase in the number of continuous billing contracts such as micoto. Recommend to buy at ¥1750, target price ¥2400, cut loss if drop below ¥1500.

|

|

|

Report Review of July 2019

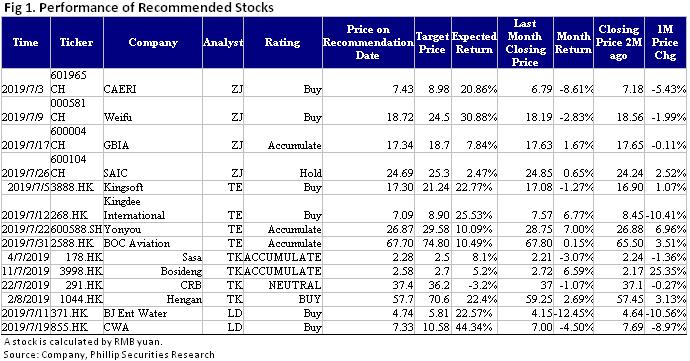

Sectors: Air, Automobiles (ZhangJing) TMT, Education & Finance (Terry Li) Retail, Property (Tracy Ku) Healthcare, Energy & Environment (Duan Lian) Automobile & Air (ZhangJing)This month I released 4 updated reports of CAERI (601965.CH)¡AWeifu (000581.CH)¡AGBIA (600004.CH) and SAIC (600104.CH), which got success by their unique Competitive edge. Among them, we recommend GBIA first The profits of Baiyun Airport in the last four quarters hit a six-year low as rebate for airport construction fee was cancelled and depreciation surged after new capacity came on stream. However, we believe that negative factors will be absorbed, and, with the launch of duty-free mode in the future and the construction of Guangdong-Hong Kong-Macao Greater Bay Area, we are optimistic about the commercial value revaluation of Baiyun Airport.Terminal T2 of Baiyun Airport was put into use on April 26, 2018. Currently, Baiyun Airport has two terminals and three runways, capable of meeting the annual operating requirements of 620,000 flight-times of aircraft movements, 80 million passengers and 2.5 million tons of cargos and mails, which solve effectively the previous production capacity bottleneck but also bring great pressure to the cost end in the short term. However, we expect the growth at the cost end to slow down from Q2 as the yoy base increases. In summer/autumn flight seasons of 2019, Baiyun recorded a yoy growth of 6.6% in total flights quote, far greater than that of 0.2% of BCIA and 0.7% of Pudong Airport. It is expected that, with the ascending time capacity and proportion of wide-body aircrafts, the aeronautical revenue of Baiyun Airport will benefit from the improvement of capacity utilization, and the bad in the cancellation of rebate for airport construction fee will be absorbed gradually in the future.The total duty-free area has been expanded from 1,300m2 to over 5,900m2 as the duty-free entry was launched in Terminal T1, and the duty-free entry/exit was launched in new Terminal T2. It is expected that the revenue from duty-free business will increase significantly in the future, and the duty-free commercial value of Baiyun Airport will reveal gradually. TMT¡AEducation & Finance (Terry Li)I released four reports on Kingsoft (3888.HK), Kingdee International (268.HK), Yonyou (600588.SH) and BOC Aviation (2588.HK). We highly recommend Yonyou. The group announced its first quarter results for 2019. During the period, the revenue was RMB 125 million , up 16.6% YoY; the operating loss was RMB 155 million, an increase of about RMB 40 million over last year. In addition, gross profit margin decreased by 1.6% to 62.5%, but the cost control improved. Selling and administrative expenses to revenue decreased by 3.5% and 4.7% respectively. Revenue from Cloud services reached RMB 125 million, a YoY increase of 95%. Currently, there are about 4.77 million cloud service enterprise users and about 380,000 paid enterprise customers, increased by 46.3% YoY. In other business areas, revenue from software business was RMB 864 million, up 20.6% YoY; payment service revenue was RMB 74 million, up 230.1% YoY; however, revenue from Internet investment and financing information service business decreased 29.7% YoY to RMB 197 million. Media reported that the Huawei ERP team visited Yonyou Industrial Park in Beijing. Therefore, it is speculated that Huawei may abandon SAP, their current ERP system, and adopt a domestic one. We think it is likely to happen. Under the China-United trade war, Huawei became one of the targets United States wants to restrain. US prohibited companies in US from providing any services to Huawei. In order to reduce the dependence on foreign software, we believe that Huawei has sufficient incentives to shift their current foreign ERP system into domestic. Although there is no confirmation at present, this visit reflects the intention of Huawei. Retail, Property (Tracy Ku)This month I released the first coverage report of Sasa(178.hk), Bosideng(3998.hk) , China Resources Beer(291.hk), and Hengan(1044) . I recommend Bosideng. Its annual revenue for FY 2018 increased by 16.9% y.o.y., slightly higher than our expectation. The revenue of the largest business branded down apparel increased by 35.5% y.o.y., mainly due to the increase of the proportion of medium and high-end products in the product mix, which led to the increase in ASP. There is not much growth in sales volume. The management team's goal this year is to make both sales volume and ASP to be the drivers of revenue growth. Medium to high-end products with a price exceeding $1800 accounted for 25% of the branded down apparel business last year, and this proportion is expected to increase further this year. Bosideng has issued clarification announcements, and the share price has since rebounded. During the annual result announcement conference, the management team also states that the chairman owns a number of asset businesses outside the listed company and will consider selling these off-balance sheet assets, including factories, to the listed company. It will also continue to pay attention to M&A opportunities, and the targeted items will contain outdoor functional, fashionable and technological elements. Pharmaceuticals, Energy & Environment (Leon Duan)I released two reports on CWA (855.HK) and BJ Ent Water (371.HK). We highly recommend CWA. The company is China's leading water supply business operator and the only Hong Kong listed water company with a focus on tap water business. As of September 2018, the company's urban water supply operation and construction has connected with about 4.4 million users, the potential service population is about 22 million, and the total length of water pipes is 137,000 kilometers. As of March 2019, the company's current water treatment capacity is about 8.94 million tons/day, a capacity of about 2.24 million tons/day is under construction, and a future expansion capacity is about 3.62 million tons/day. As of March 31, 2019, the company recorded a revenue of HKD 8.3 billion, showing a steady increase of 9.5% YoY compared with last year's HKD 7.6 billion. The revenue from water supply business was HKD 6.4 billion and it increased by 2.77% YoY due to the decrease in water supply construction and the slowdown in water supply operation growth. The revenue from environmental protection business was HKD 1.5 billion. Due to the significant increase in sewage treatment construction, the revenue from environmental protection business increased by 87.1% YoY. In addition, due to the decline in the fair value of the property invested by the company, property development and investment revenue was HKD 291 million, representing a YoY decrease of 39.2%. Overall, the company's water supply and environmental protection revenue has grown at a CAGR of 22.1% in the past four years, and as China's urbanization rate and water supply demand continue to increase, the company's core business has maintained rapid growth.

Click Here for PDF format...

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|