Investment Summary

China's leading integrated pharmaceutical company, multi-platform synergy to promote stable endogenous growth

The company has a leading position in many segments in the China pharmaceutical industry. According to the revenue in 2018, the company is the fifth largest pharmaceutical manufacturer, the third largest pharmaceutical distributor, and the largest OTC drug manufacturer in China, through CR Sanjiu, Dong-E-E-Jiao, CR Zizhu and CR Double-Crane maintained its leading position in the market. The company also has a leading position in the market in nourishing TCM, cardiovascular medicine, cold and flu medicine, large-volume intravenous infusion and emergency contraception.

With strong integration capabilities, extended development continues to expand growth space

As the fifth largest pharmaceutical manufacturer and the third largest pharmaceutical distributor in China, the company has strong resource integration capabilities and financial strength. In recent years, the company has completed several successful M&A integration cases in different fields such as pharmaceutical manufacturing and distribution. In the future, the company will make full use of the opportunity during the integrated period of pharmaceutical industry, and utilize the pharmaceutical industry fund to achieve forward-looking layout in the fields of biopharmaceuticals, innovative drugs, pharmaceutical retail and other fields and foster new business growth points.

Manufacturing and commercial drivers boost performance

The company has one of the most comprehensive pharmaceutical product portfolios among all pharmaceutical manufacturers in China, covering a range of therapeutic areas with good growth potential, such as cardiovascular system, cold and cough, anti-infection, reproductive health, alimentary tract and metabolism, dermatology and pediatrics. As of the end of 2018, the company manufactured more than 430 pharmaceutical products, of which more than 260 are included in NRDL. The company continued focus on core products, and optimize product structure. In 2018, 49 products exceed HKD 100 million in revenue, an increase of 10 compared to 2017; among which 7 products achieved annual revenue over HKD 1 billion, same with 2017. The company further strengthened distribution network coverage. In 2018, the company expedited distribution network in western provinces (adding coverage of Gansu), which not only made sustained efforts to expand the distribution network in terms of width and depth, but also penetrated markets at community-level to consolidate and promote competitive edge in regional markets. By the end of 2018, the distribution network has covered 28 provinces, serving over 90,000 downstream customers, including 6,581 Class II&III hospitals, and 51,505 primary medical institutions, customer coverage further improved.

Initial coverage with TP of HKD 10.58 and investment rating of ¡§BUY¡¨

Based on our residual income valuation model, we initiate coverage on CR Pharma with a TP of HKD 11.31, corresponding to FY19/FY20/FY21 15.76x/13.17x/12.14x PE with a 34.79% potential upside compared with CP of HKD 8.39 as of August 1, 2019, and recommend ¡§BUY¡¨ investment rating.

Industry Analysis

The pharmaceutical industry maintains rapid growth

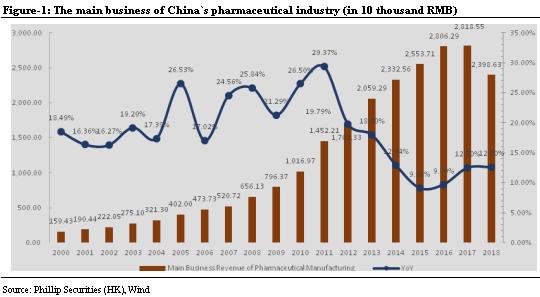

The pharmaceutical industry in China has grown rapidly in recent years. According to the statistics of Frost & Sullivan, the market size of the three major sectors (chemicals, Chinese medicine and biopharmaceuticals) of China's pharmaceutical industry has grown rapidly at wholesale prices, from RMB 743.1 billion in 2011 to RMB 1,220.7 billion in 2015, with a compound annual growth rate of 13.2%, which is expected to increase further to RMB 1,791.9 billion in 2020, with a compound annual growth rate of 8.0%. According to Wind, the annual growth rate of the main business income of China's pharmaceutical manufacturing industry from 2006 to 2018 is 16.25%, and the overall growth rate maintains high. We believe that the main driver of the rapid growth of the pharmaceutical industry is the rapid increase in personal disposable income of the urban and rural areas of China, the increased affordability of medical products and services, the rapid ageing of the population, the prolonged life expectancy, the demand for services and the healthcare reform in China.

The main mode of pharmaceutical circulation industry

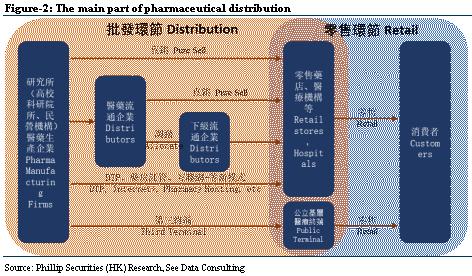

The general channels of commodity circulation can be divided into two parts, one is the wholesale (distribution), and the other is the retail. The distribution channels of the pharmaceutical market are also sold by manufacturers to retailers (including hospital pharmacies) through wholesalers. Specifically, the distribution part is mainly for pharmaceutical manufacturers or pharmaceutical distribution enterprises to sell drugs to retail pharmacies, terminal medical institutions, etc., which are divided into hospital pure-sales, commercial transfer, third terminals, etc. The retail part is mainly for pharmacies, chain pharmacies, and public medical terminals to sell drugs to individuals. In addition, there are various emerging distribution models, such as direct-to-patient (DTP) pharmacies, pharmacy hosting, and out-of-hospital prescription transfer platforms.

DTP is a new type of pharmaceutical business model, in which pharmacies obtain the distribution rights of pharmaceutical enterprises, and patients receive prescriptions from hospitals and obtain professional guidance and services after receiving prescriptions. According to Forward The Economist, DTP pharmacies mainly sell high-margin professional drugs, new special drugs, self-funded drugs, etc., and are equipped with licensed pharmacists to provide professional guidance and services, which is an advanced mode of retail pharmacies. The DTP pharmacy is completely connected to drug supply end (pharmaceutical enterprises), the prescription end (hospitals) and the demand side (patients), and combined with the drug distribution logistics function, has become the core role in the pharmaceutical circulation process. According to the China Pharmaceutical Business Association, it is expected that by 2020, the DTP pharmacy market size will reach RMB 610 billion.

The scale of the pharmaceutical circulation market has grown steadily

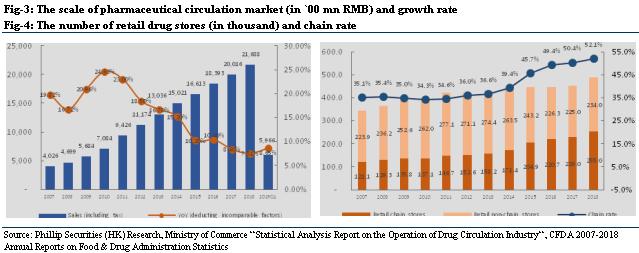

According to the Ministry of Commerce's Drug Circulation Statistics System, the total sales of the seven major categories of pharmaceutical products in the first quarter of 2019 was 596.6 billion RMB (including tax), showing an increase of 8.65% YoY deducting incomparable factors, and the growth rate was 0.72% higher than the same period of last year. The sales of retail market was 119.3 billion RMB, a YoY increase of 9.70%, growth rate increased by 0.6%. Among them, the income of pharmaceutical circulation direct reporting enterprises (total 1,071 enterprises) was 426.8 billion RMB (excluding tax), after deducting incomparable factors, the growth rate was 9.63% YoY, growth rate increased by 0.93%; the profit was 7.3 billion RMB, representing an increase of 8.84% YoY deducting incomparable factors, growth rate increased by 5.62%; the average gross profit margin was about 8.45%, an increase of 1.07%; the average expense rate was 6.88%, increasing by 0.71% YoY; the average profit rate was about 1.71%, remaining the same with last year. In 2018, the total sales of seven major categories of pharmaceutical products was 2,168.8 billion RMB (including tax), representing an increase of 7.51% YoY deducting incomparable factors, growth rate decreased by 1.03%. The pharmaceutical retail market's sales were 433.8 billion RMB, a YoY increase of 8.88%, growth rate dropped by 0.07%. Overall, the scale of the pharmaceutical circulation market maintained steady growth. From 2007 to 2018, the compound annual growth rate of the market scale reached 16.54%. Although the growth rate has declined slightly in recent years, the overall growth trend remains stable.

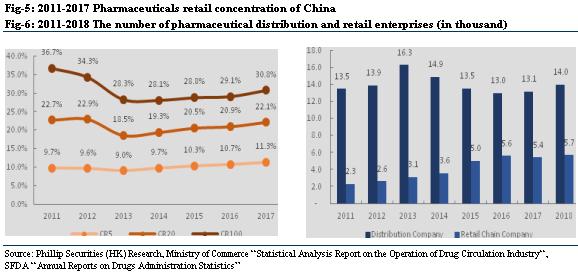

The concentration of pharmaceutical circulation industry has a large room for improvement

According to the overall goal of the National Drug Circulation Industry Development Plan (2016-2020), by 2020 there will be a number of intensive, informatized and large-scale drug circulation enterprises with a network coverage of the whole country: the annual sales of the top 100 wholesale enterprises will account for more than 90% of the total pharmaceutical wholesale market, the annual sales of the top 100 pharmaceutical retailers will account for more than 40% of the total retail market, and the retail chain rate will exceed 50%. This plan also encourages the implementation of wholesale and retail integration, chain management and multi-business mixed operations. At present, the target of the drug retail chain rate has been completed ahead of schedule. According to the ¡§Food and Drug Regulatory Statistics Annual Report¡¨ issued by the CFDA, as of the end of November 2018, there were 5,671 drug retail chain enterprises nationwide, an increase of 262 compared with last year; 2.55 million retail chain stores, an increase of 26 thousand stores compared with last year; 234 thousand retail pharmacies, an increase of 9 thousand pharmacies compared with last year; the retail chain rate of pharmacies is 52.1%, an increase of 1.7% compared with last year. It is expected that in the situation of pharmaceutical circulation management becoming stricter, the scale effect gradually becoming prominent and the industry's normative improvement, the pharmacy retail chain rate will continue to rise.

�

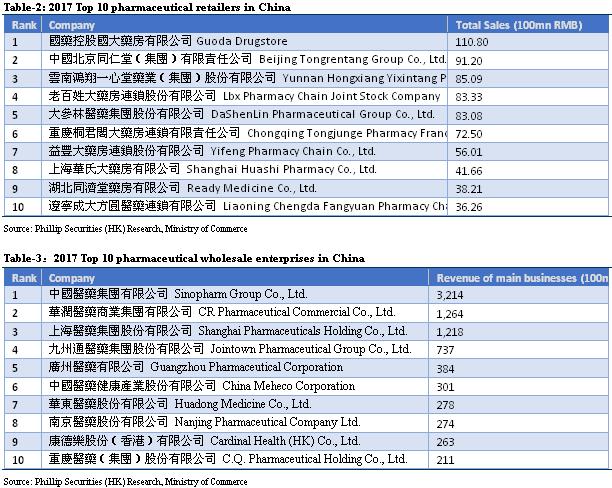

According to the ¡§Statistical Analysis Report on the Operation of Drug Circulation Industry in 2017¡¨ issued by the Department of Market Supervision of the Ministry of Commerce, the retail pharmaceuticals industry is still relatively fragmented. In the top 100 pharmaceutical retailers ranking by sales in 2017, there were a total of 58,355 retail stores, accounting for 12.9% of the market. The total sales were 123.2 billion RMB, accounting for 30.75% of the whole retail market, increasing by 15.04% YoY and exceeding 30% for the first time. In 2017, the top 100 income of pharmaceutical wholesale enterprises accounted for 70.7% of the total size of the national pharmaceutical market in the same period, down 0.2% YoY; among them, 4 national leading enterprises accounted for 37.6%, up 0.2% YoY; 30 regional leading enterprises (ranked 5-34) accounted for 24.5%, down 0.1% YoY. We believe that with the implementation of the new medical reform policy, the competitive pressure in the pharmaceutical circulation industry will further increase. The ¡§two-invoice system¡¨ reform will slow down the sales growth of distribution enterprises, and the prescriptions of medical institutions will also allow patients to flow to retail pharmacies. This has led to large-scale drug circulation enterprises and retail chain enterprises to continuously enhance the distribution capacity of enterprises through the extension of mergers and acquisitions, and also promote the increase of retail chain rate.

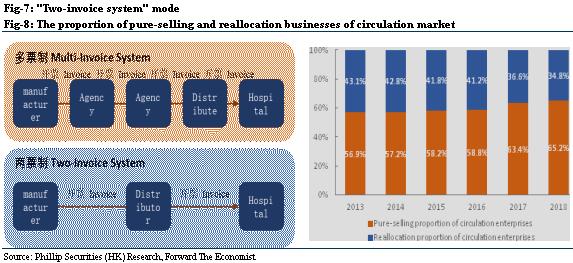

Two-invoice system promotes industry integration

The "two-invoice system" in the field of pharmaceutical circulation means that the pharmaceutical production enterprises directly invoice to the circulation enterprise, and the circulation enterprise re-invoices (delivery) to the hospital, and invoices are issued twice. Under the influence of the "two-invoice system", the pure-selling and reallocation business have polarized. The pure-selling business grows rapidly due to the "two-invoice" medical reform policy, and the reallocation business, in which the intermediaries transfer inventories to the sub-distributors, has a smaller proportion of business, leading to a further decline in industry sales growth. In addition, as the ¡§two-invoice system¡¨ brings greater capital turnover pressure to enterprises, M&A integration in the pharmaceutical commerce sector will become a new development trend. We believe that with the implementation of the national health reform policy and the enhancement of capital, the concentration and chain rate of the pharmaceutical circulation industry will further increase in the future.

�Company Analysis

Company Profile

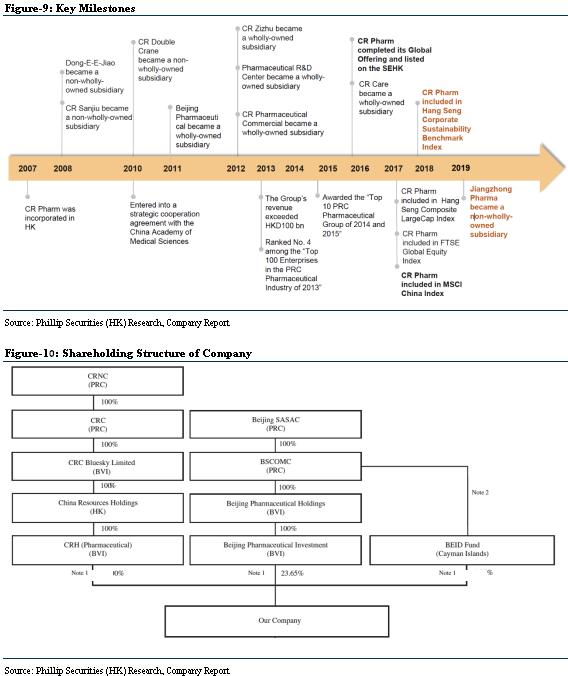

The company which is listed on the Main Board of The Stock Exchange of Hong Kong Limited in 28 October 2016 (Stock Code: 3320), is a leading integrated pharmaceutical company in China, its business spans across manufacturing, distribution and retail of pharmaceutical and healthcare products. The company was established in 2007, and has developed into the fifth largest pharmaceutical manufacturer and the third largest pharmaceutical distributor in China. The company has already been included in a number of capital market indexes such as MSCI China Index, FTSE Global Large Cap Index, constituent stock of Hang Seng Composite Large Cap Index and Hang Seng Corporate Sustainability Benchmark Index.

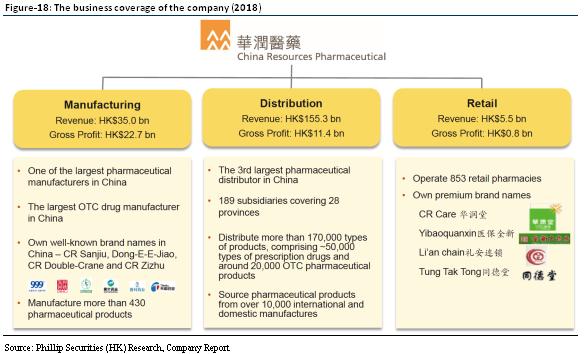

The manufacturing business of the company encompasses the research and development, manufacturing and sale of pharmaceutical products. It manufacture more than 430 products comprising chemical drugs, Chinese medicines and biopharmaceutical drugs as well as nutritional and healthcare products, covering a wide range of therapeutic areas including cardiovascular, alimentary tract and metabolism, large-volume IV infusion, pediatrics, respiratory system etc.. Besides, the company owns a series of strong, well-known brands including ¡§CR Sanjiu¡¨, ¡§Dong-E-E-Jiao¡¨, ¡§CR Double-Crane¡¨, ¡§Jiangzhong¡¨ and ¡§CR Zizhu¡¨. Meanwhile, the company operates a national distribution network comprising 170 logistics centers strategically across 28 provinces, municipalities and autonomous regions in China, and directly distributes products to hospitals and other medical institutions across the country. In addition, the company operates one of the largest retail pharmacy networks in China, comprising over 850 retail pharmacies under national or regional premium brands -- ¡§CR Care¡¨, ¡§Yibaoquanxin¡¨, ¡§Li`an chain¡¨, and ¡§Tung Tak Tong¡¨.

In 2018, the revenue of the company was HKD 189.69 billion, with a YoY increase of 9.9%; net profit was HKD 34.93 billion, with an increase of 23.5% YoY; net profit contributed to owners was HKD 4.04 billion, an increase of 15.9% YoY.

Key Business Analysis

The company is a leading integrated pharmaceutical company in China, engaged in the research and development, manufacturing, distribution and retail of a broad range of pharmaceutical and other healthcare products. The company primarily operates in the following three segments: pharmaceutical manufacturing, pharmaceutical distribution and pharmaceutical retail.

1. Pharmaceutical manufacturing business

The company is one of the largest pharmaceutical manufacturers and the largest OTC drug manufacturer in China. As of 31 December 2018, the pharmaceutical manufacturing business of the company produced and sold more than 430 pharmaceutical products, 49 pharmaceutical products with annual revenue over HKD 100 million, among which seven pharmaceutical products achieved annual revenue over HKD 1 billion. The manufacturing business is mainly included 4 segments: chemical drugs, Chinese medicines, biopharmaceutical products, and nutritional & healthcare products.

Chemical drugs are primarily manufactured and marketed by CR Double-Crane and CR

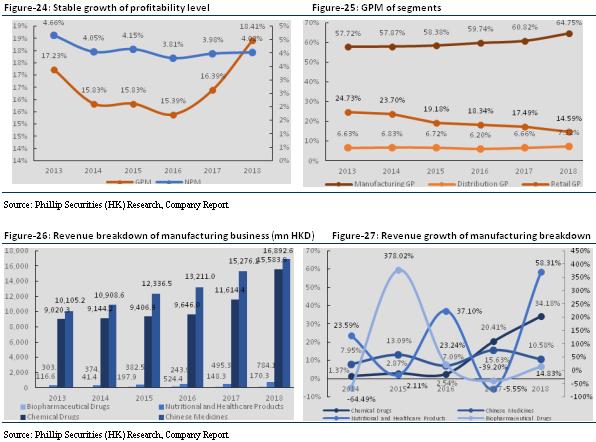

Zizhu, and cover three major areas: (i) the development, manufacture and sale of medicines for chronic diseases, such as cardiovascular diseases and diabetes; (ii) intravenous therapy, mainly large-volume IV infusion products; (iii) specialty therapeutic areas such as pediatrics, nephrology and reproductive health. CR Sanjiu, our manufacturing subsidiary with its primary focus on Chinese medicines, also manufactures and markets a limited number of chemical drugs, mainly anti-infectives and dermatological products. In 2018, the revenue from sale of chemical drugs was HKD 15.58 billion, a rapid YoY increase of 34.2%, which mainly attributable to the increase in the revenue from anti-infective drugs, infusion products as well as chronic diseases drugs and specialty drugs.

Chinese medicines are primarily manufactured and marketed by CR Sanjiu and Dong-E-E-Jiao, and cover three main areas: (i) self-diagnosis and treatment products, which are mainly OTC medicines and cover therapeutic areas such as cold remedies, alimentary tract and metabolism and orthopedics; (ii) prescription Chinese medicines, which cover therapeutic areas such as cardiovascular system and oncology; and (iii) E-Jiao product series, a traditional Chinese medicine. CR Double-Crane, the company's manufacturing subsidiary with its primary focus on chemical drugs, also manufactures and sells a limited number of Chinese medicines, covering therapeutic areas such as cardiovascular system, orthopedics and pediatrics. In 2018, the revenue from sale of Chinese medicines was HKD 16.89 billion, representing a YoY increase of 10.6%, which mainly caused by the increase in the revenue from OTC products and formula granules of Traditional Chinese Medicines (TCM).

The major biopharmaceutical products manufactured by Dong-E-E-Jiao are: (i)Recombinant Human Erythropoietin for injection (Jialinhao) for the treatment of anemia in chronic kidney disease (renal insufficiency); (ii) Recombinant Human TissuePlasminogen Activator Derivatives (r-PA) for injection (Ruitongli), a thrombolytic drug for the treatment of myocardial infarction; and (iii) Recombinant Human Interleukin-11 for injection (Baijieyi), a medicine for chemotherapy-induced thrombocytopenia in patients with cancer. In 2018, the revenue from sale of biopharmaceutical drugs was HKD 170.3 million, representing a YoY increase of 14.8% caused by adjustment of sales model.

The major nutritional product is Taohuaji, which is derived from our E-Jiao Chinese medicine product series. In 2018, the revenue from sale of nutritional and healthcare products was HKD 784.1 million, representing a YoY increase of 58.3%, attributable to the enriched variety of healthcare products.

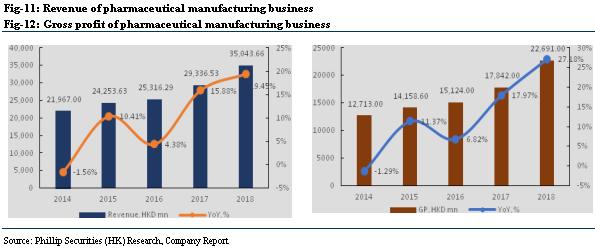

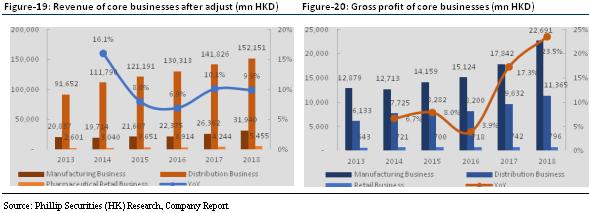

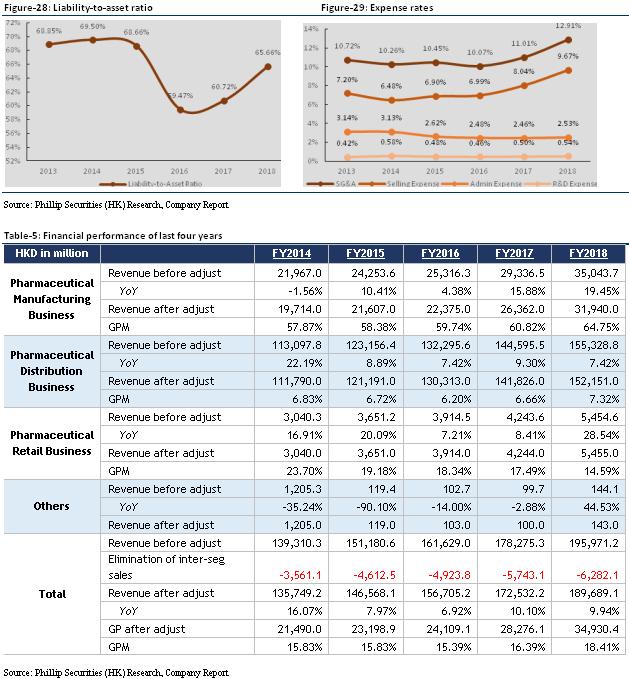

In 2018, the segment revenue in pharmaceutical manufacturing business of the company recorded HKD 35.04 billion, representing an increase of 19.5% YoY; the segment gross profit was HKD 22.69 billion, with a YoY increase of 27.2%; the segment gross profit margin was 64.8%, representing an increase of 4.0% YoY, which was mainly caused by restructuring and upgrading of the pharmaceutical manufacturing business, continuous optimization of product portfolios and improvement of manufacturing process.

2. Pharmaceutical distribution business

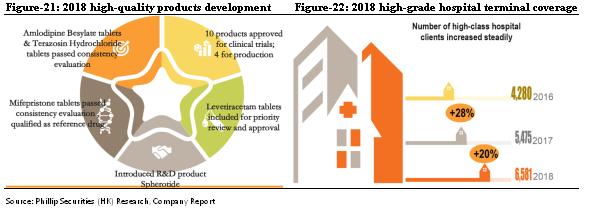

The company is the 3rd largest pharmaceutical distributor in China, distributes more than 170,000 types of products, comprising 50,000 types of prescription drugs and around 20,000 OTC pharmaceutical products. As of 31 December 2018, the pharmaceutical distribution network of the company covered 28 provinces, municipalities and autonomous regions nationwide, with customers including 6,581 Class II and Class III hospitals, 51,505 primary medical institutions and 26,964 retail pharmacies. The company's distribution business operates 170 logistics centers, and provided hospital logistic intelligence (HLI) services to approximately 300 hospitals cumulatively, and commenced dozens of network hospital logistics intelligence (NHLI)projects.

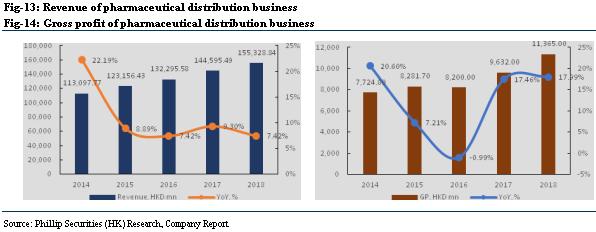

In 2018, the segment revenue in pharmaceutical distribution business of the company recorded HKD 155.33 billion, representing an increase of 7.4% YoY; the segment gross profit was HKD 11.37 billion, with a YoY increase of 18.0%; the segment gross profit margin was 7.3%, representing an increase of 0.6% YoY.

3. Pharmaceutical retail business

As of 31 December 2018, the company had 853 retail pharmacies in total, including 140 DTP pharmacies covering 66 cities in China. The company owns premium brand names such as ¡§CR Care¡¨, ¡§Yibaoquanxin¡¨, ¡§Li`an chain¡¨, and ¡§Tung Tak Tong¡¨.

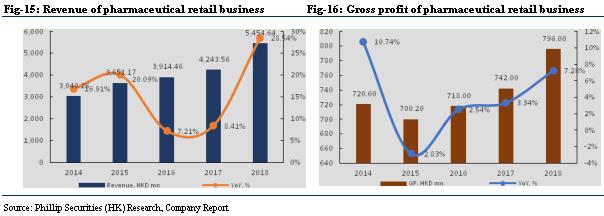

In 2018, the segment revenue in pharmaceutical retail business of the company recorded HKD 5.46 billion, representing an increase of 28.5% YoY; the segment gross profit was HKD 796 million, with a YoY increase of 7.3%; the segment gross profit margin was 14.6%, a decrease of 2.9% YoY. The decreasing of gross profit margin was mainly due to the rapid growth of DTP business which has a relatively lower profit margin.

Investing Highlights

China's leading integrated pharmaceutical company, multi-platform synergy to promote stable endogenous growth

The company has a leading position in many segments in the China pharmaceutical industry. According to the revenue in 2018, the company is the fifth largest pharmaceutical manufacturer, the third largest pharmaceutical distributor, and the largest OTC drug manufacturer in China, through CR Sanjiu, Dong-E-E-Jiao, CR Zizhu and CR Double-Crane maintained its leading position in the market. The company also has a leading position in the market in nourishing TCM, cardiovascular medicine, cold and flu medicine, large-volume intravenous infusion and emergency contraception.

The company's diversified business segments and product portfolio in the pharmaceutical industry, as well as extensive coverage of the medical industry chain, not only help to reduce risks and uncertainties associated with individual product, but also effectively leverage synergies between different platforms. effect. With its extensive customer network, the company's pharmaceutical distribution business regularly assists the pharmaceutical business in promoting the products to hospitals and other medical institutions. The company's pharmaceutical retail and distribution business also pass the tendering strategy for the centralized tendering process as well as OTC pharmaceutical products and nutritional supplements. The development strategy of retail pharmacies and other stores provides advice to assist the pharmaceutical business. The synergy between the company's internal business is more flexible, which can effectively improve the stability and efficiency of the supplier.

The company's performance has maintained steady growth in recent years. In 2018, the company recorded revenue of HKD 189.69 billion, an increase of 9.9% YoY (representing an increase of 6.9% YoY in terms of RMB). In 2018, the revenue of the three major business segments, namely pharmaceutical manufacturing, pharmaceutical distribution and pharmaceutical retail businesses, accounted for 16.8%, 80.2% and 2.9% of the total revenue, respectively. From 2013 to 2018, the company's revenue maintained rapid growth at a compound annual growth rate of 10.16%, and remained at around 10% in recent years. In 2018, the company achieved a gross profit of HKD 34.93 billion, a YoY increase of 23.5%. The overall gross profit margin was 18.4%, an increase of 2% YoY. From 2013 to 2018, the company's compound annual growth rate of gross profit was 11.63%, slightly higher than the growth rate of income. We believe that the company's steady growth is due to the company's continuous optimization of its business and product structure, focusing on core products, integrating distribution of retail resources and continuously promoting the development of DTP business. We also believe that the company's high quality and stable endogenous growth will continue to promote the performance in the future.

With strong integration capabilities, extended development continues to expand growth space

As the fifth largest pharmaceutical manufacturer and the third largest pharmaceutical distributor in China, the company has strong resource integration capabilities and financial strength. In recent years, the company has completed several successful M&A integration cases in different fields such as pharmaceutical manufacturing and distribution. For example, the company restructured CR Sanjiu in 2007 and positioned it as the main business platform for OTC drugs and Chinese medicines, realizing the leading position of OTC drugs and TCM in the market. The net profit of CR Sanjiu has increased by 301.4% from 2006 to 2010; additionally, after the company acquired Beijing Pharmaceutical in 2010, the company integrated its pharmaceutical distribution business through CR Pharmaceutical Commercial, and acquired more than 60 regional pharmaceutical distributors to further expand its distribution network. From 2010 to 2015, the revenue of CR Pharmaceutical Commercial achieved a compound annual growth of 54%, and net profit achieved a compound annual growth of 68%.

In the future, the company will make full use of the opportunity during the integrated period of pharmaceutical industry, and utilize the pharmaceutical industry fund to achieve forward-looking layout in the fields of biopharmaceuticals, innovative drugs, pharmaceutical retail and other fields and foster new business growth points. The pharmaceutical manufacturing business will invest high-growth therapeutic areas such as cardiovascular, anti-tumor, biopharmaceuticals, and general health, focus on competitive products with exclusive varieties or high technology thresholds, and selectively acquired enterprises with differentiated product portfolios or supplemented with existing core products. In the pharmaceutical distribution and retail business, the company will further consolidate its leading position in the industry by investing or acquiring distribution companies with high-quality customer resources and quality pharmaceutical retailers.

Manufacturing and commercial drivers boost performance

The company has one of the most comprehensive pharmaceutical product portfolios among all pharmaceutical manufacturers in China, covering a range of therapeutic areas with good growth potential, such as cardiovascular system, cold and cough, anti-infection, reproductive health, alimentary tract and metabolism, dermatology and pediatrics. From 2011 to 2016, CR Sanjiu was one of the only three pharmaceutical companies named among the ¡§Most Valuable Chinese Brands¡¨ for six consecutive years by WPP; and Dong-E-E-Jiao was named as one of the 50 ¡§Best China Brands¡¨ by Interbrand (an international leading brand consultancy) in 2014 and 2015 because of its strong brand recognition and large market share in China. As of the end of 2018, the company manufactured more than 430 pharmaceutical products, of which more than 260 are included in NRDL. The company continued focus on core products, and optimize product structure. In 2018, 49 products exceed HKD 100 million in revenue, an increase of 10 compared to 2017; among which 7 products achieved annual revenue over HKD 1 billion, same with 2017.

The company continued to increase investments in research and development activities in 2018. As of 31 December 2018, the company had 222 research and development projects, including 32 projects regarding innovative drugs, mainly focusing on research and development areas such as cardiovascular system, metabolism and endocrine, respiratory system, tumor and immunity, psychiatric and neurological system, anti-infection, blood and genitourinary system. One of the oncology drugs is in phase II clinical research, while another respiratory system Category 1 innovative drug has initiated IND (Investigational New Drug) application process with the U.S. FDA. In addition, 11 projects were pending for registration approval by NMPA. In 2018, the company obtained 33 patents; ten products has been approved by NMPA for clinical trials, and four products has been approved by NMPA for production. Meanwhile, the company conducted multi-directional strategic collaboration with the National Center for Nanoscience and Technology of Chinese Academy of Sciences, Union Institute of Materia Medica, Nankai University, WuXi AppTec, Fujifilm Corporation in Japan, Pharmaron and Peking University School of Pharmaceutical Sciences in various therapeutic areas, including oncology, immune diseases, anti-infection and respiratory system. In addition, the company in-licensed a number of research stage new products from overseas that carry significant clinical and market value, including two Class 1 innovative chemical drugs and one biosimilar drug which are in therapeutic areas of respiratory system and digestive system. Furthermore, the Group introduced a product, Spherotide, a long-acting microsphere-based injectable drug developed by Swedish company Xbrane. The company have commenced over 40 consistency evaluation projects, and eight products have completed bioequivalence clinical trials.

The company is a leading provider of pharmaceutical supply chain solutions in China, providing upstream and downstream customers with logistics, distribution, marketing and other value-added services for pharmaceutical products. The company further strengthened distribution network coverage. In 2018, the company expedited distribution network in western provinces (adding coverage of Gansu), which not only made sustained efforts to expand the distribution network in terms of width and depth, but also penetrated markets at community-level to consolidate and promote competitive edge in regional markets. By the end of 2018, the distribution network has covered 28 provinces, serving over 90,000 downstream customers, including 6,581 Class II&III hospitals, and 51,505 primary medical institutions, customer coverage further improved. In addition, business structure of the company further optimized by leveraging the opportunity of the ¡§two-invoice system¡¨, revenue of direct business increased to 75% of total distribution business, a YoY increase of 9%.

The company has also continuously improved its service model and created new profit growth points: the company has adopted the ¡§high-value drug direct delivery¡¨ service model ( DTP model) introduced by well-known multi-national pharmaceutical companies for high-end special medicine products, effectively improving the gross profit of individual pharmacies; in 2015, the company launched online and offline sourcing services to the distributors and pharmacy customers in the online comprehensive service platform of Henan, effectively expanding the local business.

Financial Forecast and Valuation

Financial Performance

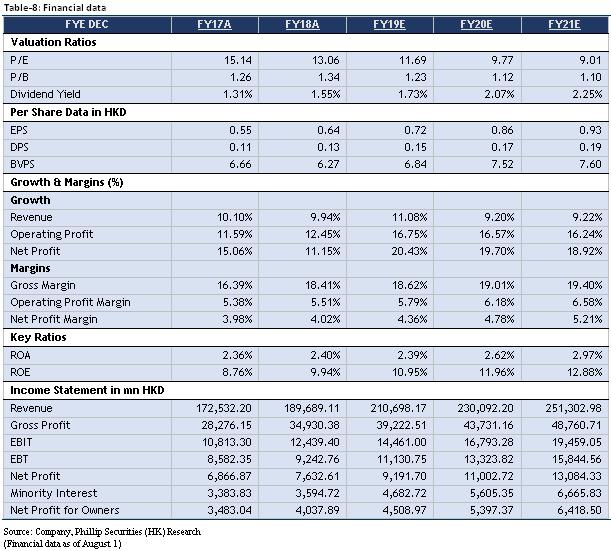

In 2018, the company recorded income of HKD 189.7 billion, representing an increase of 9.94% YoY; realized gross profit of HKD 34.9 billion, increasing by 23.5% YoY; realized gross profit margin of 18.41%, increasing by 2.03% YoY; realized net profit attributable to owners of HKD 4.0 billion, increasing by 15.9% YoY. From the historical data, the company's overall profit level has maintained a steady growth, of which the gross profit margin increased from 17.23% in 2013 to 18.41% in 2018, it is mainly because the company continues to optimize the product structure and business structure, especially affected by pharmaceuticals and distribution businesses. The gross profit margin of the pharmaceutical business increased significantly from 57.72% in 2013 to 64.75% in 2018, and the gross profit margin of the distribution business increased from 6.63% in 2013 to 7.32% in 2018, which also shows a good profitability of the company's two core businesses.

After the company went public in 2016, the liability-to-asset ratio fell to 59.47%. In recent years, it has gradually increased and close to the level before being listed. According to the company's management, the company's long-term debt level will remain below 50%. In terms of expense rate, the company's overall expense rate showed a steady upward trend, which was mainly affected by the ¡§two-invoice system¡¨. The company's selling expense increased significantly reaching 9.67% in 2018. Beneficial from the company's effective internal cost control, administrative expense has declined slightly, and the proportion of R&D expense has remained stable.

Financial Forecast

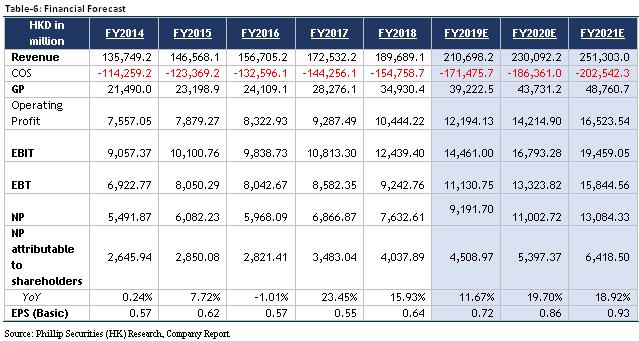

It is estimated that the company's revenue in FY19/FY20/FY21 will be HKD 210.7/230.1/251.3 billion, representing increases of 11.08%/9.20%/9.22% YoY; gross profit will be HKD 39.2/43.7/48.8 billion, representing increases of 12.29%/11.50%/11.50% YoY; net profit attributable to shareholders will be HKD 4.5/5.4/6.4 billion, representing increases of 11.67%/19.70%/18.92% YoY; corresponding EPSs are HKD 0.72/0.86/0.93. As a leading comprehensive pharmaceutical enterprise in China, the company would continue the combination of organic growth with external acquisition, with the drivers of manufacturing and commercial businesses. And the company will keep optimizing the product portfolio and business model, and strengthening the integration of the industry chain. We are optimistic about the company's future development.

Valuation

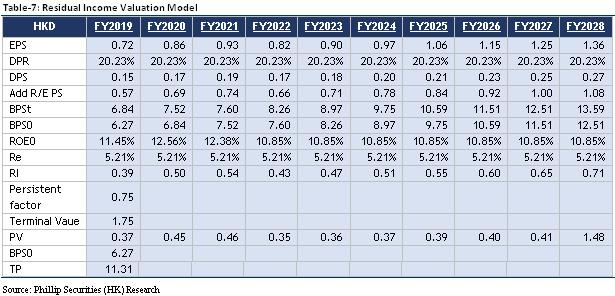

Based on our residual income valuation model, assuming the cost of equity is 5.21% and resistance factor is 0.75, considering the effect of Dong-E-E-Jiao, we give a TP of HKD 11.31, corresponding to FY19/FY20/FY21 15.76x/13.17x/12.14x PE with a 34.79% potential upside compared with CP of HKD 8.39 as of August 1, 2019. Wind data shows that the company's expected PER of 11.59x in FY19 is attractive compared to the industry average PER 26.27x, we initiate coverage on CR Pharm and recommend ¡§BUY¡¨ investment rating.

Risk

1. Policy risk of pharmaceutical industry

2. Slowdown of external acquisition

Financials

Click Here for PDF format...