Investment Summary

H1 Sales Volume Decreased by 15%, and the MGMT Cut Sales Target by 10%

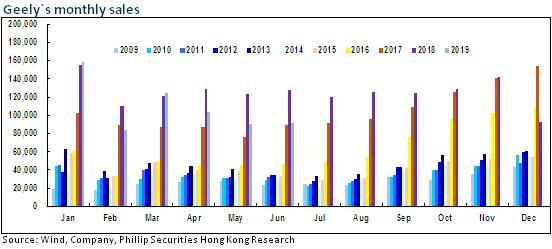

Because of the depression in the car market caused by the downturn in the economic boom, the sales volume potential of new models not fully exploited, the great challenge for its old models posed by the falling prices of the joint venture brand competing products and the increasing base, Geely Auto's strong double-digit yoy growth rate for 10 consecutive quarters has been interrupted since the fourth quarter of last year, and the overall decline is gradually expanding. In the fourth quarter of 2018/the first quarter of 2019/the second quarter of 2019, the sales volume of the Company dropped 13%/5%/25% yoy, respectively.

In H1 of 2019, the cumulative total sales volume of the Company is about 651,700 units, a decrease of about 15% yoy, reaching 43% of the original target of 1.51 million units. The Company lowered its sales volume target for the whole year by about 10%, from 1.51 million to 1.36 million, meaning that the total sales volume in H2 accounts for 42% of the new target, with a sharp yoy decrease to 3.5% and an average monthly sales volume of 118,000 units.

The Upward Trend of Vehicle Structure Remains

In terms of vehicle models, the major incremental sales volume contribution comes from the launch of the new models in 2018, including Bin Yue/Bin Rui/Bo Rui GE (+130,000 units), and new models in 2019, including Xing Yue/Geometry A/Jia Ji (+22,000 units). The sales volume reduction mainly comes from the older vehicle models, including Vision/Vision SUV/Vision S1/Vision X3/Vision X1 (-132,000 units), Bo Yue (-30,000 units), and the low-end vehicle models Emgrand/King Kong (-32,000 units). As the base is still low, the total sales volume of LYNK&CO series has increased by about 20% or 9,000 units, basically maintaining a steady pace. The implementation of the national VI emission standard ahead of schedule has accelerated the new and old models alternation process of the Company, with share of new models increasing and the model structure moving up further.

Profit Warning of 40% less Profit in H1 Was Issued, and the Profit Was Affected by the Decrease in Scale and Sales Promotion to Clear Inventory

At the same time, the Company issued a H1 performance warning. It is estimated that the net profit will decrease by 40% from RMB6.67 billion in the same period last year to about RMB4 billion, a decrease far greater than the decrease in sales volume. Sales volume of old models have fallen sharply and sales volume potential of new models are to be developed, resulting in insufficient capacity utilization rate. Depreciation cost increases due to release of new models/engine capacity. Pressure on promotion and price reduction of national V vehicles to clear inventory increases. We believe that for the above-mentioned reasons, the sales volume decreased sharply. We estimate that gross profit margin may decline by more than three ppts in H1.

Pressure Eases in H2

However, thanks to the vigorous inventory removal, the channel inventory of the Company decreased significantly. In June, the channel inventory decreased by 31,000 units, thus reducing the brand pressure. The inventory of national V vehicles has been nearly cleared up. The Company achieved full coverage of national VI vehicles in May. The price of national VI vehicles is RMB3000-20,000 higher than that of national V vehicles. At present, the terminal price discount has been reduced somewhat compared with before, and the gross profit margin is expected to recover. However, considering the promotion in June satisfied partial demand and the off-season of the industry in the third quarter, it remains to be seen whether the recovery in the economic boom will continue.

It is worth mentioning that 2019 will be the year when Geely's new energy strategy is fully launched. New energy and electrified versions of various models will be launched one after another, including LYNK&CO 02/03 PHEV, Binyue PHEV, Jia Ji PHEV, and FY11PHEV. New energy and electrified vehicles accounted for 67,919 of the total sales in 2018, up 173% Y-o-Y, accounting for 4.5% of the total sales. With the accelerated introduction of PMA platform vehicles, the proportion of new energy vehicles will gradually increase in the future.

Investment Thesis

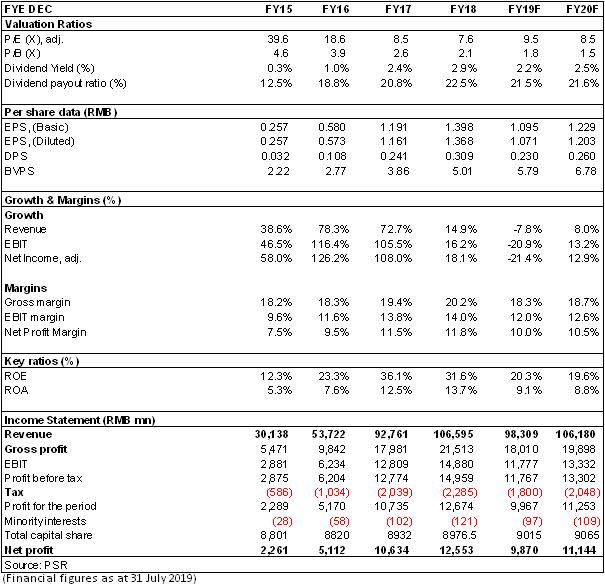

In view of the latest sales volume and profit warning, we lower our EPS estimate. We expect that with the economic slowdown in the short to medium term, the domestic car market will enter an era of adjustment. Although we are optimistic about the long-term development potential of the Company, we believe that the current company has a reasonable valuation and lacks substantial benefits in the short term. We revised our target price to HK$12.66, equivalent to 9.9/8.9 P/E ratio in 2019/2020, and we give the rating of Hold. (Closing price as at 31 July 2019)

Financials

Click Here for PDF format...