Investment Summary

China's comprehensive water supply service provider, with operating scale leading domestically

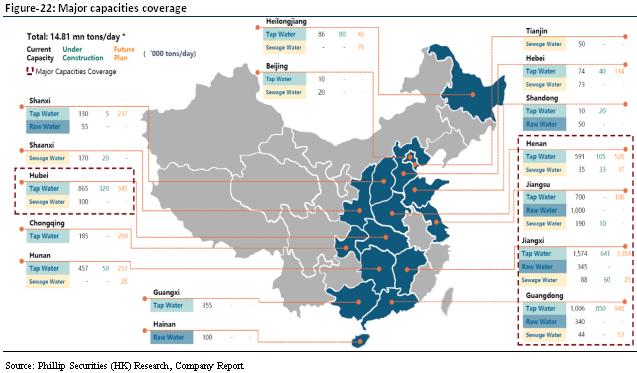

The company is China's leading water supply business operator and the only Hong Kong listed water company with a focus on tap water business. As of September 2018, the company's urban water supply operation and construction has connected with about 4.4 million users, the potential service population is about 22 million, and the total length of water pipes is 137,000 kilometers. As of March 2019, the company's current water treatment capacity is about 8.94 million tons/day, a capacity of about 2.24 million tons/day is under construction, and a future expansion capacity is about 3.62 million tons/day.

Organic growth combined with outreach M&A, core business maintains rapid development

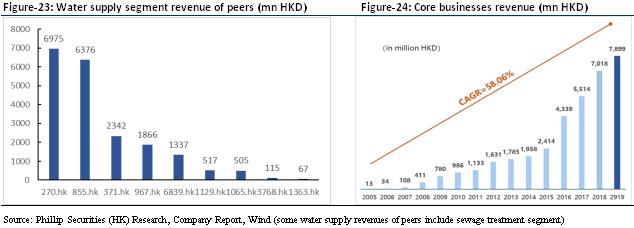

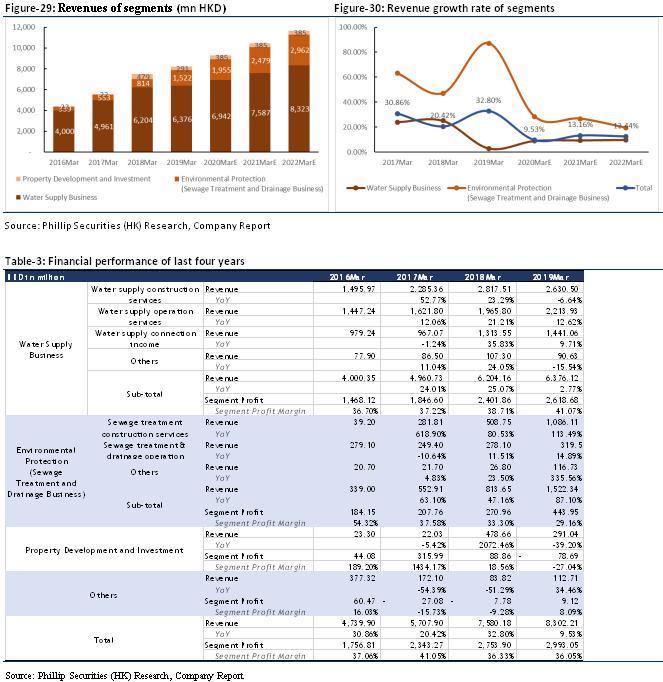

As of March 31, 2019, the company recorded a revenue of HKD 8.3 billion, showing a steady increase of 9.5% YoY compared with last year's HKD 7.6 billion. The revenue from water supply business was HKD 6.4 billion and it increased by 2.77% YoY due to the decrease in water supply construction and the slowdown in water supply operation growth. The revenue from environmental protection business was HKD 1.5 billion. Due to the significant increase in sewage treatment construction, the revenue from environmental protection business increased by 87.1% YoY. In addition, due to the decline in the fair value of the property invested by the company, property development and investment revenue was HKD 291 million, representing a YoY decrease of 39.2%. Overall, the company's water supply and environmental protection revenue has grown at a CAGR of 22.1% in the past four years, and as China's urbanization rate and water supply demand continue to increase, the company's core business has maintained rapid growth. In addition, through disposal of non-core assets, the company could generate around HKD 3 billion cash, which will be used in development of core businesses.

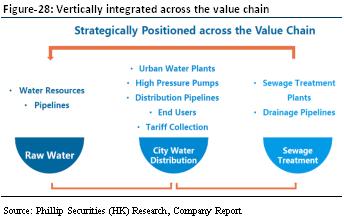

TOO model promotes co-operation with the government, strategically covered across the entire value chain

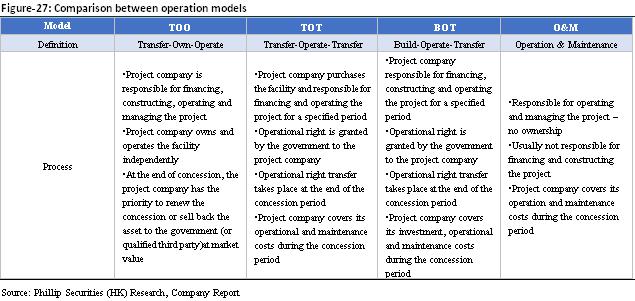

Most of the company's projects adopt the TOO model (Transfer-Own-Operate), that is, the company invests in the acquisition of the completed water supply project and undertakes the operation and maintenance of the project. The property rights of the assets (including water plants, pipe networks and land) belongs to a specially established project company. The project company improves asset profitability by reducing leakage rate and providing value-added services. The company provides end-to-end water supply solutions to governments and customers through vertical integration across the entire value chain, from the construction of raw water networks, to the distribution of urban water supplies, to drainage and sewage treatment operations.

Initial coverage with TP of HKD 10.58 and investment rating of ¡§BUY¡¨

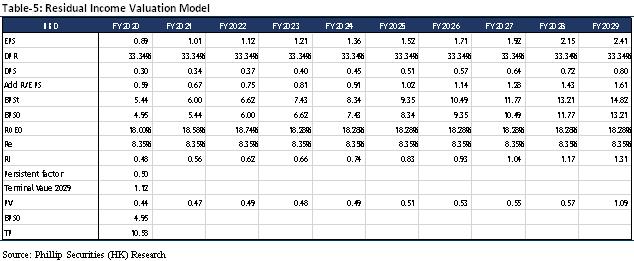

Based on our residual income valuation model, we initiate coverage on China Water Affairs with a TP of HKD 10.58, corresponding to FY20/FY21/FY22 11.87x/10.47x/9.41x PE with a 44.40% potential upside compared with CP of HKD 7.33 as of July 17, 2019, and recommend ¡§BUY¡¨ investment rating.

Industry Analysis

Strong demand in China's water industry

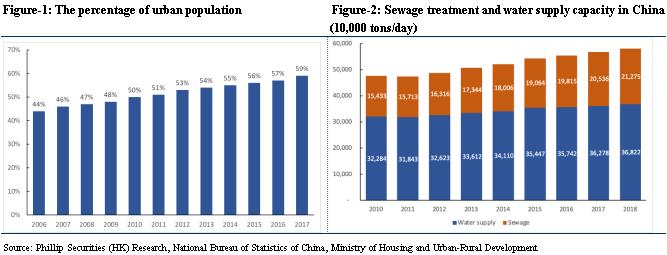

According to the National Bureau of Statistics of China, the proportion of urban population in China was 59% in 2017, and it showed an increasing trend year by year. The growth of urbanization in China has created long-term demand for water and sewage treatment business. According to ¡§2018 Urban and Rural Construction Statistical Yearbook¡¨, by the end of 2017, the urban water penetration rate has reached 98.3%, and the county water penetration rate has also reached 92.87%. In recent years, the construction of water supply facilities has approached saturation, and the total urban water supply in China has remained basically stable, maintaining a growth rate of 1%-3%. In terms of sewage treatment, by the end of 2017, China had built 8,591 sewage treatment plants in cities, country seats and towns, with the sewage treatment capacity of about 207 million m3/day, and the growth rate was between 4%-6% in recent years.

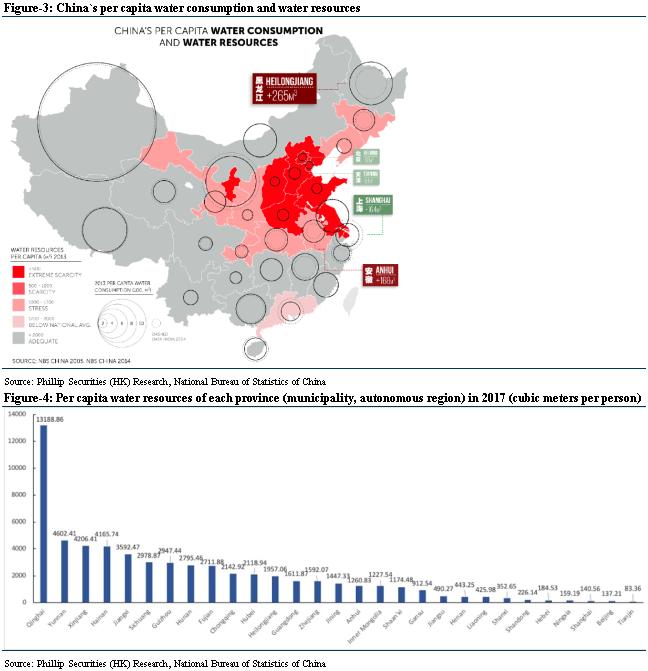

China is one of the most water-deficient countries in the world, recognized by the UN as one of the 13 countries with water shortage, over 400 out of 660 cities suffer from water shortage in China. Acute inadequacy of natural water supply and uneven distribution of water resources lead to severe water shortage in the northern and part of the eastern areas in China. According to the National Bureau of Statistics of China, the amount of water resources per capita in China has decreased year by year. In 2018, China's average per capita freshwater resources was 2,007.57 m³, down 3.2% YoY, and only one third of the global average.

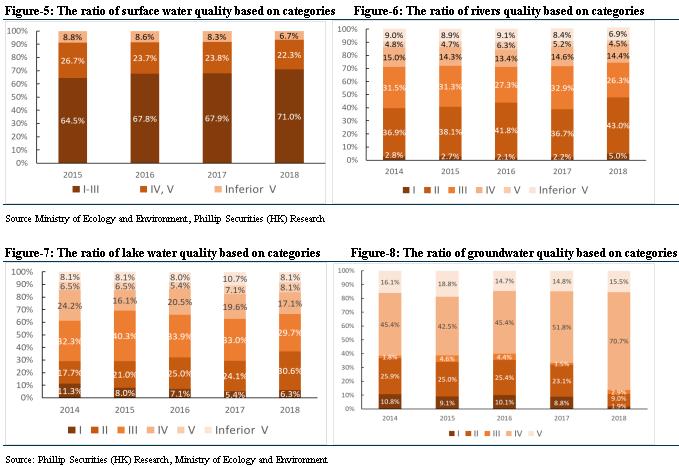

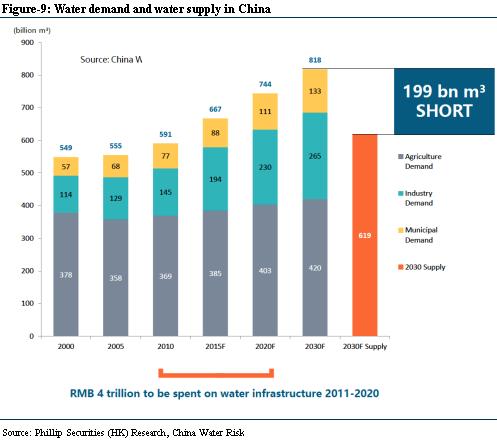

The rapid development of urbanization and industrialization has led to a sharp increase in demand for water resources in China. At the same time, the industrialization process has led to an increase in water pollution. According to the China Ecological Environment Bulletin" issued by the Ministry of Environmental Protection, the proportion of Class I~III of surface water was 74.3%, the proportion of Class inferior V was 6.9%; Class I~III, IV~V and inferior V of river was accounted for 74.3%, 18.9% and 6.9%, respectively; Class I~III, IV~V and inferior V of lake water was accounted for 66.6%, 25.2% and 8.1%, respectively; Class I~III, IV and V of groundwater was accounted for 13.8%, 70.7% and 15.5%, respectively; the water quality is not optimistic. According to expectation of China Water Risk, by 2030, China's water supply will be much lower than demand, and will cause a shortage of 199 billion m3. Comprehensively, the water supply and sewage treatment market in China has strong demand and insufficient supply, and there are many long-term opportunities in the future water supply and sewage treatment business.

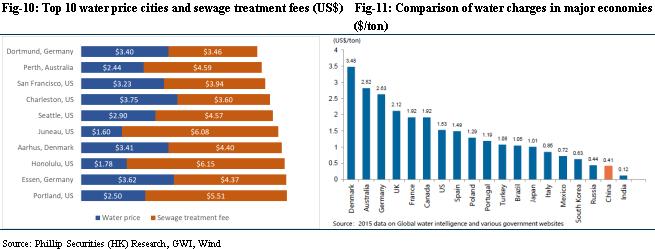

On the other hand, China's water price is at a relatively low level. According to the 2017 Global Water Price White Paper released by GWI, water price in China is much lower than that of other countries in the world. The highest water price in China is less than one tenth of the most expensive city in the world, and sewage treatment fees are also much lower than that of the top ten cities with the most expensive water prices in the world. There is still much space for improvement in the water price and sewage treatment fees in China.

Driven by policy, water environment treatment market still has huge room for development

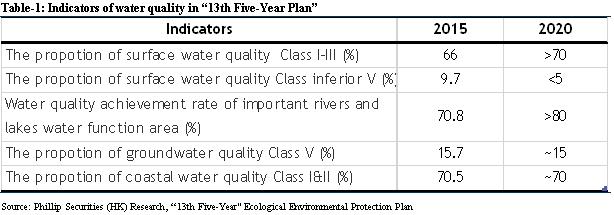

According to the ¡§13th Five-Year Plan for Ecological Environmental Protection¡¨ issued by the State Council in November 2016, by 2020 the proportion of the water quality of centralized drinking water sources at or above the prefecture level reaching or exceeding Class III will be more than 93%; the trend of increasing pollution will be initially curbed, the proportion of groundwater with extremely poor quality is controlled at around 15%; the proportion of black and odorous water in urban built-up areas is controlled within 10%, and other cities strive to eliminate heavy black and odorous water bodies; rivers near coastal provinces (districts, cities) into the sea basically eliminate the inferior V water; all county towns and key towns have sewage collection and treatment capacities, urban and county sewage treatment rates reach 95% and 85%, respectively; prefectural and above cities basically realize the complete collection and treatment of sewage; improving the level of sewage recycling and sludge disposal, vigorously promote sludge stabilization, harmlessness and resource treatment and disposal, and achieves harmless treatment and disposal rate of municipal sludge at prefecture level at 90%, the Beijing-Tianjin-Hebei region reach 95%; the utilization rate of reclaimed water in the water-deficient city reaches more than 20%, and the Beijing-Tianjin-Hebei region reaches more than 30%; promote the construction of sponge city, which can reach the area of utilizing 70% of the rain more than 20% of the total area, and the water-deficient cities of the prefecture level and above all meet the national water-saving city standard requirements, Beijing-Tianjin-Hebei, the Yangtze River Delta and Pearl River Delta regions should complete one year ahead of schedule. The ¡§13th Five-Year Plan¡¨ of ecological environmental protection water environment quality mainly includes the following indicators:

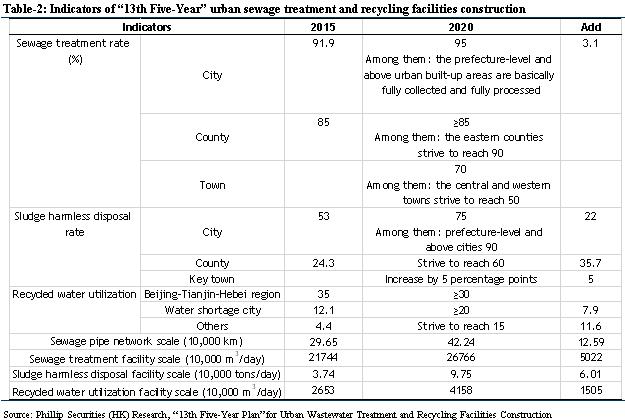

According to the ¡§13th Five-Year Plan for Urban Wastewater Treatment and Recycling Facilities Construction¡¨ jointly prepared by the National Development and Reform Commission and the Ministry of Housing and Urban-Rural Development in December 2016, as of 2015, the national urban sewage treatment capacity has reached 217 million cubic meters/day, the urban sewage treatment rate reached 92%, and the county sewage treatment rate reached 85%. During the ¡§13th Five-Year Plan¡¨ period, the newly added sewage pipe network was 125,900 kilometers, including 66,200 kilometers of city and 29,200 kilometers of county and 30,500 kilometers of town; the old sewage pipe network transformation is 27,700 kilometers, including 15,800 kilometers of city, 0.73 million kilometers of county, 0.46 million kilometers of town; 28,800 kilometers of merged pipe network, 17,000 kilometers of city, 11,700 kilometers of county seat. The newly-added sewage treatment facilities have a scale of 50.22 million cubic meters per day, of which the city has a scale of 28.56 million cubic meters per day, the county has 10.71 million cubic meters per day, and the town has 10.95 million cubic meters per day. the scale of the sewage treatment facilities was upgraded to 42.2 million cubic meters per day, including 36.39 million cubic meters per day in the city and 5.81 million cubic meters per day in the county; new sludge (water-containing 80% wet sludge) has a harmless disposal scale of 60,100 tons/day, including 45,600 tons/day for the city, 9,200 tons/day for the county, and 5,300 tons/day for the town; The newly-added reclaimed water utilization facility has a scale of 15.05 million cubic meters per day, of which 12.14 million cubic meters per day of the city and 2.91 million cubic meters per day of the county.

In terms of investment, the ¡§13th Five-Year¡¨ urban sewage treatment and recycling facilities construction has invested a total of about RMB 564.4 billion. Among them, the investment in various types of facilities construction was RMB 560 billion, and the investment in supervision capacity building was RMB 4.4 billion. In the construction investment, the newly-built supporting sewage pipe network was invested RMB 213.4 billion, the old sewage pipe network transformation investment was RMB 49.4 billion, the rain-sewage pipe network transformation investment was RMB 50.1 billion, and the newly added sewage treatment facility investment was RMB 150.6 billion. The investment in sewage treatment facilities was RMB 43.2 billion, and the investment in new or modified sludge treatment and disposal facilities was RMB 29.4 billion, and the investment in newly added reclaimed water production facilities was RMB 15.8 billion. During the ¡§13th Five-Year Plan¡¨ period, the investment in construction of cleaning the black and odorous water body at the prefecture level and above was about 170 billion yuan, which has been included in the planned key construction task investment.

In addition, in December 2016, the ¡§13th Five-Year Plan for Water Conservancy Reform and Development¡¨ issued by National Development and Reform Commission stated that by 2020, the total annual water supply for the country will be controlled within 670 billion m3, and RMB10,000 GDP water consumption and RMB10,000 industrial added value will decrease 23% and 20%, respectively compared to that of 2015. The leakage rate of urban public water supply network in China is controlled within 10%, and the urban and industrial water usage rate reach more than 85%. In rural areas, the rural tap water penetration rate reaches more than 80%, and the rural centralized water supply rate reaches over 85%. The water quality achievement rate and water supply security level should be further improved. In terms of water price, the urban residents` water ladder price system and non-resident water use exceeds quota and progressive price increase system should be fully implemented, in order to expand the water price difference between the high water consumption industry and other industries. And also establish a price incentive mechanism that encourages the use of unconventional water resources.

The water industry is less concentrated and the market capacity is still expanding

According to research by the Qianzhan Industrial Research, there are more than 4,000 waterworks in China, more than 3,500 sewage treatment plants, and many water companies. However, the industry concentration is quite low: the operating scale market share of CR5 is 11%, and CR10 is 16.5%, and the market concentration in the water distribution is relatively low. In the sewage treatment industry, the market share of CR5 wastewater treatment enterprises is 19%, and the market share of CR10 is 27.2%. Compared with the water distribution market, the concentration of the sewage treatment market is relatively high. Excessive market fragmentation restricts the technological progress of the water industry and the intensification of services. It is expected that the industry leaders will carry out more mergers and acquisitions in the future, break the technical and geographical restrictions and form a competitive landscape dominated by several major water groups through the expansion.

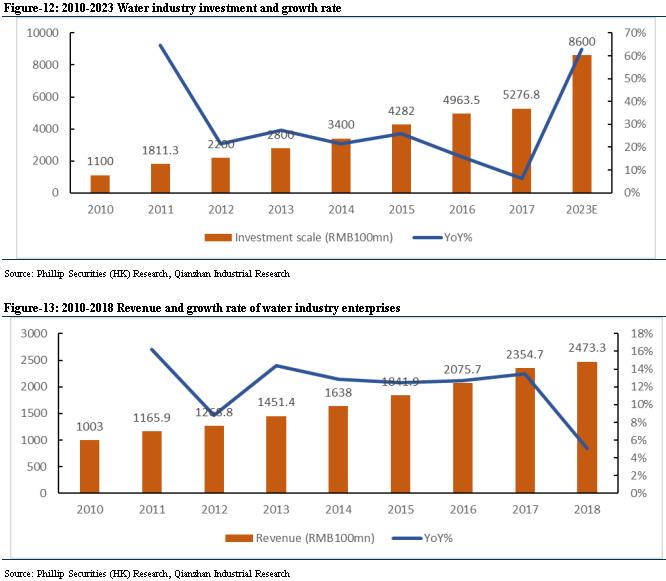

As a weak cyclical industry, the water industry is highly correlated with factors such as economic growth level, population size and urbanization process. In recent years, the regulatory requirements for industry have been continuously strengthened, and the fields of black-odorous water treatment, construction of sponge cities, and township sewage treatment have grown rapidly. Overall, the scale of investment in the water industry has continued to increase, and there still have space for development in market capacity. According to Qianzhan Industrial Research, the annual growth rate of investment in the water industry during the ¡§Twelfth Five-Year Plan¡¨ period was 24%. It is estimated that by 2023, the annual investment amount of water industry in China will exceed RMB860 billion.

Company Analysis

Company Profile

The company which is listed on the Main Board of The Stock Exchange of Hong Kong Limited (Stock Code: 0855), is a leading market-oriented and cross region water supply operator in China and the only Hong Kong listed water company focusing on tap water. By investing, building and operating water affairs projects in China, the company has rapidly built its reputation as one of the largest integrated water affairs operators providing raw water, tap water, sewage treatment and related value-added services. To date, the company's businesses span in 13 provinces, 3 municipal cities, and over 60 cities in mainland China, covering around 20 million people, and connecting 4.75 million users. Total daily capacity of the company is around 14.8 million m3, and integrated water treatment capacity exceeds 8 million m3 per day. Since 2009, the company has been included in the FTSE Environmental Opportunities Asia Pacific Index. In 2016, the company was included in the first batch of Shenzhen-Hong Kong Stock Connect by HKEX. In 2019Q1, the revenue of the company was HKD 8.302 billion, with a YoY increase of 9.53%; net profit was HKD 3.464 billion, with an increase of 5.91% YoY; net profit contributed to owners was HKD 1.369 billion, an increase of 20.05% YoY.

Key Business Analysis

As a one-stop water services solution provider, the company has a very diversified business portfolio, ranging from urban water supply, sewage treatment, installation of water pipes and electronic meter systems, to water resources management. The company aims at providing services for all segments of the entire water services industrial chain, and associated value-added services. The main businesses of the company are water supply business, environmental protection business, property development and investment business.

1. Water supply business

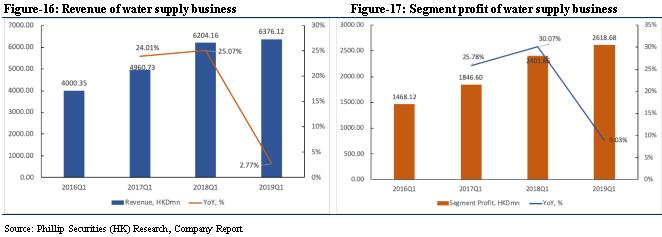

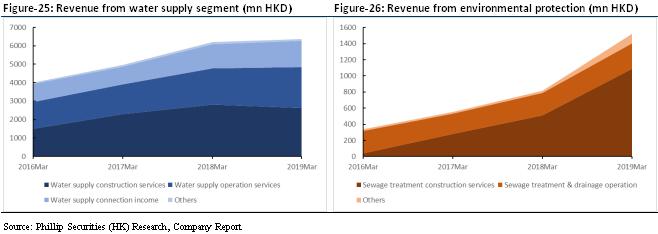

As of 31 March 2019, water supply projects of the company are well spread in various provincial cities and regions across mainly China, including Hunan, Hubei, Henan, Hebei, Hainan, Jiangsu, Jiangxi, Shenzhen, Guangdong, Beijing, Chongqing, Shandong, Shanxi and Heilongjiang. In 2019Q1, the revenue from water supply segment (including city water supply, water related connection works and construction services) amounted to HKD 6,376.12 million (2018Q1: HKD 6,204.16 million), representing a steady increase of 2.8% YoY. The water supply segment profit amounted to HKD 2,618.68 million (2018Q1: HKD 2,401.86 million), representing a steady increase of 9.0% as compared with the last corresponding year. This was mainly because of increase in volume of water sold, procurement of more construction and connection work driven by the continuation of urban-rural integration and the promotion of the Public-Private Partnership model in the water sector and the additional contribution from the new water projects during the year.

2. Environmental protection business

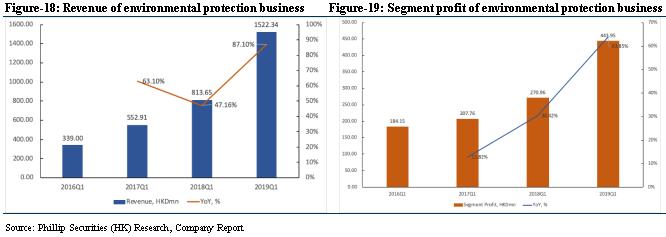

Environmental protection projects of the company are well spread in various provincial cities and regions across China, including Beijing, Tianjin, Shenzhen, Guangdong, Henan, Hebei, Hubei, Jiangsu, Jiangxi, Shaanxi and Heilongjiang. In 2019Q1, the revenue from environmental protection segment (including sewage treatment and drainage operating and construction, solid waste and hazardous waste business, environmental sanitation and water environment management) amounted to HKD 1,522.34 million (2018Q1: HKD 813.65 million), representing a significant increase of 87.1% YoY. The environmental protection segment profit amounted to HKD 443.95 million (2018Q1: HKD 270.96 million), representing a significant increase of 63.8% YoY. This was mainly because of upgrade of facilities for higher operating standard and procurement of more water environmental renovation construction services.

3. Property development and investment business

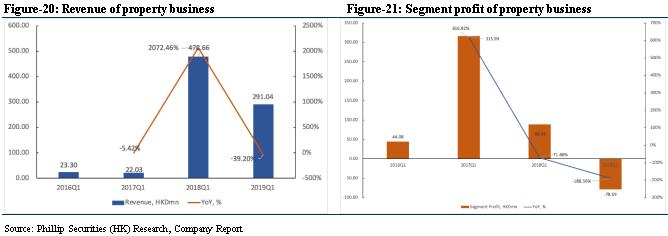

The company held various property development and investment projects which are mainly located in Beijing, Chongqing, Jiangxi, Hunan, Hubei and Henan provinces of mainland China. In 2019Q1, the revenue from the property business segment amounted to HKD 291.04 million (2018Q1: HKD 478.66 million), with a decrease of 39.20% YoY. The total property business segment loss amounted to HKD 78.69 million (2018Q1: segment profit amounted to HKD 88.86 million). This was mainly due to the decrease in sales of property projects with high gross profit margin in current year.

�Investing Highlights

China's comprehensive water supply service provider, with operating scale leading domestically

The company is China's leading water supply business operator and the only Hong Kong listed water company with a focus on tap water business. As of September 2018, the company's urban water supply operation and construction has connected with about 4.4 million users, the potential service population is about 22 million, and the total length of water pipes is 137,000 kilometers. As of March 2019, the company's current water treatment capacity is about 8.94 million tons/day, a capacity of about 2.24 million tons/day is under construction, and a future expansion capacity is about 3.62 million tons/day.

The company's business is mainly based on water supply business, and it also operates environmental protection and property development & investment businesses. As of March 31, 2019, the company's core business income was HKD 7.9 billion, representing an increase of 12.55% YoY; segment profit was HKD 3.1 billion, showing an increase of 14.58% YoY. From 2005 to 2019, the CAGRs of company's core businesses revenue and segment profit were 58.06% and 109.14% respectively.

Organic growth combined with outreach M&As, core business maintains rapid development

As of March 31, 2019, the company recorded a revenue of HKD 8.3 billion, showing a steady increase of 9.5% YoY compared with last year's HKD 7.6 billion. The revenue from water supply business was HKD 6.4 billion and it increased by 2.77% YoY due to the decrease in water supply construction and the slowdown in water supply operation growth. The revenue from environmental protection business was HKD 1.5 billion. Due to the significant increase in sewage treatment construction, the revenue from environmental protection business increased by 87.1% YoY. In addition, due to the decline in the fair value of the property invested by the company, property development and investment revenue was HKD 291 million, representing a YoY decrease of 39.2%. Overall, the company's water supply and environmental protection revenue has grown at a CAGR of 22.1% in the past four years, and as China's urbanization rate and water supply demand continue to increase, the company's core business has maintained rapid growth. In addition, through disposal of non-core assets, the company could generate around HKD 3 billion cash, which will be used in development of core businesses.

The company continues to enhance its water supply capacity through outreach mergers and acquisitions, and based on its mature operation experience and management capabilities, the company is capable to improve the overall operation efficiency of the newly acquired water plants in short time. As of March 2019, the company's total daily design water supply capacity was approximately 13.49 million tons, and sewage treatment capacity was 1.11 million tons. In addition, the company entered into an agreement with Kangda International Environmental Co Ltd Kangda Holdings Co., Ltd. and Mr. Zhao Silian on April 3, 2019, pursuant to which the company agreed to acquire 600,000,000 ordinary shares at par value of HKD 0.01 per share (accounting for 29.52%) of Kangda International Environmental Co Ltd (6136.HK) at a total consideration of HKD 1.2 billion. Kangda International and its subsidiaries are mainly engaged in urban water treatment, comprehensive water environment management and rural water improvement. After the completion of the acquisition, the company will continue to focus on the water supply business and develop the environmental protection business. The company is optimistic about the future synergy with Kangda International and it is believed that the company will fully participate in the business operation of Kangda International in the future.

TOO model promotes co-operation with the government, strategically covered across the entire value chain

Most of the company's projects adopt the TOO model (Transfer-Own-Operate), that is, the company invests in the acquisition of the completed water supply project and undertakes the operation and maintenance of the project. The property rights of the assets (including water plants, pipe networks and land) belongs to a specially established project company. The project company improves asset profitability by reducing leakage rate and providing value-added services.

The company provides end-to-end water supply solutions to governments and customers through vertical integration across the entire value chain, from the construction of raw water networks, to the distribution of urban water supplies, to drainage and sewage treatment operations. At the same time, the company will actively grasp the tremendous room for value added services, such as pipeline maintenance and water meter installation. By arranging the entire industry chain and operating a stable and growing utility business, the company continues to increase its operation scale and has a strong resistance to the impact of the economic cycles.

�Financial Forecast and Valuation

Financial Performance

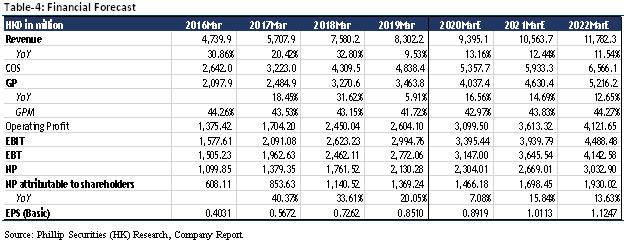

As of March 31, 2019, the company's revenue was HKD 8.3 billion, representing an increase of 9.53% YoY; gross profit was HKD 3.5 billion, showing a growth of 5.91% YoY; gross profit margin was 41.72%, decreasing 1.43%; net profit attributable to shareholders was HKD 1.4 billion, increasing 20.05% YoY. From the historical data, the overall income and gross profit of the company maintained a relatively steady growth. It is expected that as the market liquidity improves, China's urbanization rate continues to increase, and the demand of water supply and sewage treatment continues to expand, the company will continue to have good opportunity in the water industry.

Regarding the water supply business, we believe that the revenue from the water supply construction business will remain stable in the next three years, and the water supply operation and connection businesses will maintain a CAGR of approximately 13%-15%. Overall, the water supply business is expected to remain a CAGR of around 9.29% in the next three years. For the environmental protection business, with the completion of the pre-construction project and the integration of Kangda International, it is expected that the company's environmental protection business will have a CAGR of approximately 24.84% in the next three years. We also believe that as the company's endogenous growth and outreach mergers and acquisitions continue to accelerate, the unique TOO model continues to be implemented, and the cooperation with the government is further consolidated, the coverage of entire industry chain continues to expand, the company's business will bring better synergy and continuous performance and profit growth.

Financial Forecast

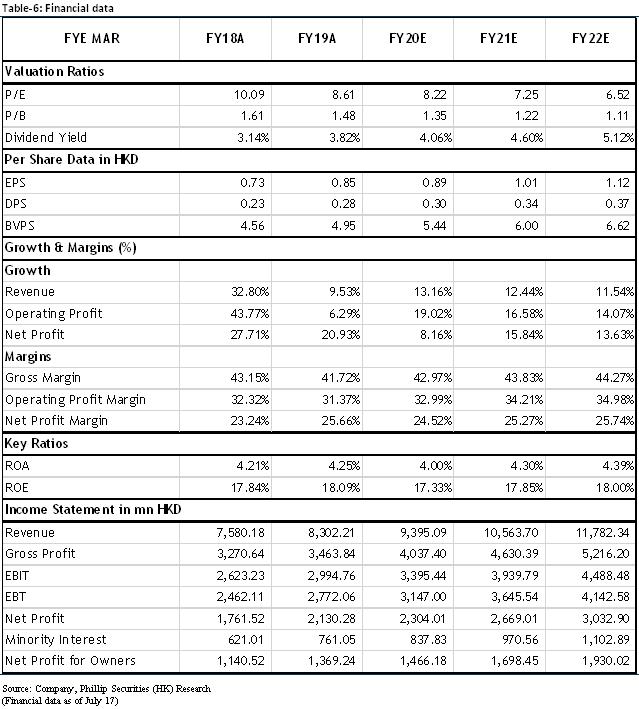

It is estimated that the company's revenue in FY20/FY21/FY22 will be HKD 9.40/10.56/11.78 billion, representing increases of 13.16%/12.44%/11.54% YoY; gross profit will be HKD 4.04/4.63/5.22 billion, representing increases of 16.56%/14.69%/12.65% YoY; net profit attributable to shareholders will be HKD 1.47/1.70/1.93 billion, representing increases of 7.08%/15.84%/13.63% YoY; corresponding EPSs are HKD 0.8919/1.0113/1.1247. As a leading water supplier, the company will continue to adhere to the combination of endogenous growth and outreach mergers and acquisitions, cover the entire value chain of the water supply industry, and continue to play the unique advantage of the TOO model. We are optimistic about the company's future development.

Valuation

Based on our residual income valuation model, assuming the cost of equity is 8.35% and resistance factor is 0.5, we give a TP of HKD 10.58, corresponding to FY20/FY21/FY22 11.87x/10.47x/9.41x PE with a 44.40% potential upside compared with CP of HKD 7.33 as of July 17, 2019. Wind data shows that the company's expected PER of 6.48x in FY2020 is attractive compared to the industry average PER 10.60x, we initiate coverage on China Water Affairs and recommend ¡§BUY¡¨ investment rating.

Risk

1. Water supply capacity fails expectations

2. Growth of water price fails expectations

3.Slowdown of M&A

Financials

Click Here for PDF format...