Investment Summary

he Group announced a profit warning, where the net profit attribute to the owner in 2019H1 decreased by 30%-40%. However, the revenue increased by 15%-20% and the revenue from cloud services also rose by 50%-60%. During the period, Cosmic developed well. It acquired 28 new clients in the first half this year, with RMB 1.1 mn average price. Slower growth in traditional ERP and increase in R&D leads to a drop in net profit. We believe if the Cloud services is going well, the reason to buy still exists, even though the growth of traditional ERP dropped. We give a TP of $8.90, 3.4% lower than previous, updating to ¡§Buy¡¨ recommendation, with 25.5% potential upside. (Closing price at 10 Jul 2019)

Result update

The Group announced a profit warning on 6 July, where the net profit attribute to the owner in 2019H1 decreased by 30%-40% and the Group has incurred a investment loss of RMB 18 mn. However, the revenue increased by 15%-20% and the revenue from cloud services also rose by 50%-60%.

Strong growth of Cloud services with high renewal rate

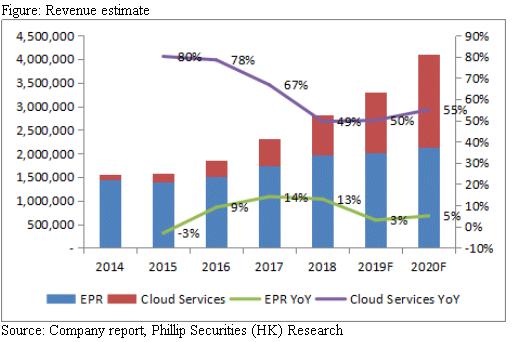

The cloud services business grew by 50%-60% YoY, slightly higher than our estimate (50%). During the period, Cosmic developed well. It acquired 28 new clients in the first half this year, whereas there were only about a dozen last year. The average price of the contracts are RMB 1.1mn, and the clients were all with revenue more than 10bn. As the Cosmic become more mature, the capacity of dealing with the demand of large clients for the Group will be enhanced. Since the average price of the contract of Cosmic is higher, we expect Cosmic will become the major growth driver in cloud services. In addition, the management also stated that the renewal rate remained high. Guanyi Cloud,recorded a negative growth last year, resumed its growth in the first half after the adjustments from the Group, about 20% .

Slower growth in traditional ERP and increase in R&D leads to a drop in net profit

Based on the median from the range provided by the Group, it is expected the growth of traditional ERP to be about 3%, lower than our estimate (9%). We believe the drop in the growth of traditional ERP were 1) the clients delay or reduce its IT expenditure due to the concern on the economic downturn in the first half and 2) the demand of traditional ERP is shifting to Cloud services. The management stated that there are some projects delayed, where we believe it should relate to the former reason and it should be a short-term impact. But, the latter is a longer-term impact. Cloud services are the future trend. As the focus of the group shifts to cloud services, the gradual decline in traditional ERP business growth is likely to happen. The Group targeted 60% proportion of Cloud services to the total revenue in 2020, so if the Cloud services is going well, the reason to buy still exists, even though the growth of traditional ERP dropped.

As the Group keeps spending on R&D in Cloud services, such as Cosmic this year, leading to a loss in Cloud services. The traditional ERP then serves as an important role to support the R&D in Cloud services. As a result, once the growth of traditional ERP decreased, the net profit will also drop.

Earnings forecast

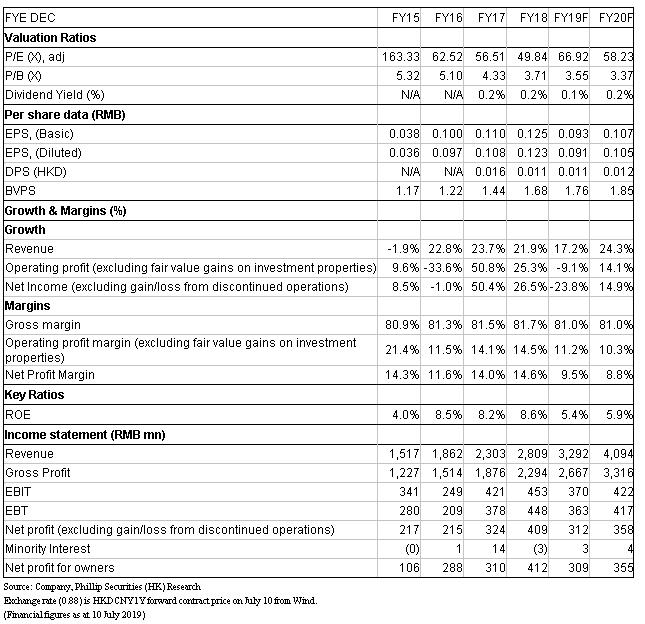

In view of the dropped growth in traditional ERP for the first half, we lower the estimated growth of traditional ERP in 2019F/20F by 6%/1%. Besides, as the Group will increase its investment in Cloud services, we lifted the estimated proportion of selling and marketing expenses to revenue in 2019F/20F both by 1% and that of research and development costs to revenue in 2019F/20F both by 1.5%. As a result, the expected net profit attributable to the owner in 2019F/20F dropped by 20.3%/21.6% respectively.

Valuation

We adopted sum of the parts valuation by dividing the business into three parts: 1) Traditional ERP business (P/E), 2) Cloud business (P/S), and 3) Investment real estate business (book valuation). We forecast the earnings per share of the traditional ERP business in 2019F to be RMB 0.109, 5.2% lower than the previous estimate in reflection of the slower growth in the first half, with target PE ratio 15x; the revenue of cloud services per share in 2018 would be RMB 0.386. We maintain the target PS ratio to be 13x; for the investment real estate business, the book valuation is used, and the valuation per share is RMB 0.55. Finally, a net cash is RMB 0.46 per share in 2018. A target price of HK$8.90 was derived, 3.4% lower than previous target price. As the slump in stock price, we upgrade to ¡§Buy¡¨ recommendation, with 27.1% potential upside. (HKD/RMB: 0.88)

Risk

1.Slower-than-expected growth in cloud products

2.The economy of China slows down

3.Cloud ERP may take away the existing customers of traditional ERP, particularly SME

Financials

Click Here for PDF format...