|

CEB WATER(1857)

Analysis¡G

China Everbright Water (1857) is the largest Central State-Owned Enterprise operating in the wastewater treatment industry in the PRC, providing a comprehensive range of environmental water services. Its business spans wastewater treatment, water environment treatment, integrated utilization of water resources and water ecological protection. As of December 31, 2018, it had 85 projects in operation. The Group generally achieves its growth through three major ways: (i) obtaining new projects from local governments; (ii) project upgrade and expansion and (iii) acquisitions. Currently, its share price is still about 30% below the listing price of HK$2.99. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $2.10, Target Price: $2.40, Cut Loss Price: $1.95

|

HAIDILAO(6862)

Analysis¡G

In 2015, 2016 and 2017, it ranked first in the Chinese hot pot cuisine market. In 2017, the market share was 2.2%. The number of restaurants owned and operated is 320, including 296 in mainland China and 24 restaurants in Taiwan, Hong Kong and overseas in Singapore, Korea, Japan and the United States. In 2017, same store sales increased 14% y.o.y., the average spending per guest was RMB 97.7, and the overall table turnover rate was 5.0 times per day.In 2018, the revenue increased by RMB59.55billion to RMB16.969 billion, the same store sales increased by 6.2%, and the net profit increased from RMB1.027 billion to RMB1.646 billion.China's hot pot restaurant market grew at a CAGR of 11.6% from 2013 to 2017, and is expected to grow at a CAGR of 10.2% from 2017 to 2022. It is the fastest growing segment of Chinese catering and has the largest market share. 2017 The annual market share is 13.7%. From 2013 to 2017, China's catering service market revenue grew at a CAGR of 10.7%, and is expected to grow at a CAGR of 9.6% by 2022.

Strategy¡G

Buy-in Price: $ 33.20, Target Price: $ 38.00, Cut Loss Price: $29.00

|

|

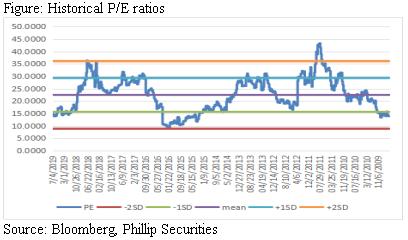

Sasa(178.HK) - Hong Kong's political situation affecting the market sentiment. Rent costs to be expected being further controlled.

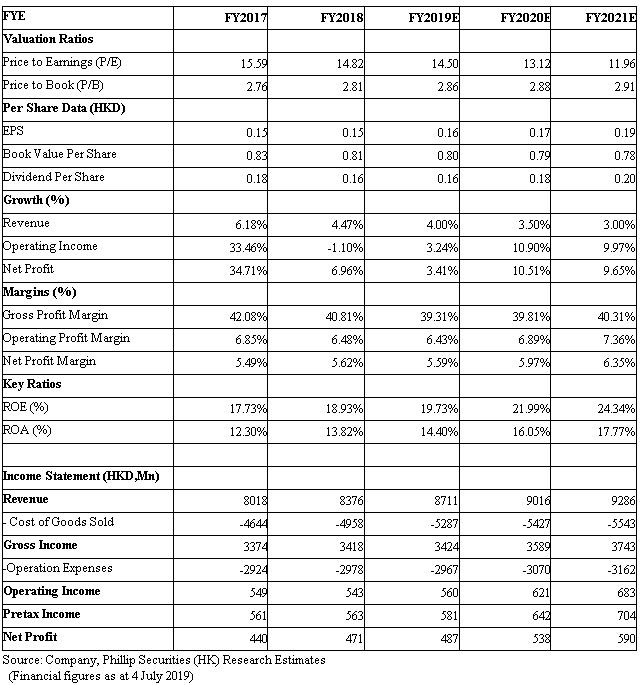

Investment SummarySasa's FY2018 full-year revenue increased by 4.5% y.o.y., but fell by 5% in 2H of the year. The Hong Kong and Macau market fell by 5.8%, while same-store sales fell by 7.3%, compared with 18.5% in 1H. According to the management team, in the first month of FY2019 (April), the Hong Kong and Macao market continued to have a significant decline in revenue. In May, the decline was less than 4%. During June 1st to 8th before the mass demonstration, the decline was over 3% which was similar to May. During the large-scale demonstrations and conflicts from June 9 to 16, the number of mainland tourists dropped significantly, and the decline in revenue expanded to nearly 20%. At the same time, consumer sentiment was affected by RMB depreciation due to the Sino-US trade war as well as a decline in both the stock and property markets, which began in late June 2018. The average sales per transaction decreased by 3.0% in 2H. During the year, a number of pharmacies selling skincare and cosmetic products aggressively opened new stores in tourist hot spots, which intensified competition. The result was that growth in the number of transactions by Mainland customers dropped from 21.8% in 1H to 1.0% in 2H. The number of transactions by local customers also changed from positive growth in the first half to a decline of 7.0% in 2H. The launch of the HK Section of the Express Railway Link and the Hong Kong-Zhuhai-Macau Bridge did not contribute to greater traffic in its retail stores. Nevertheless, the company believes that the two mega infrastructure projects will eventually drive the economic development of the Greater Bay Area and boost the consumption power of both local customers and tourists. It will continue to seize the opportunities offered by the region's vast economic potential. In Q1 of FY2018, sales from trendy products in HK and Macau markets outperformed those of house brand products. This resulted in a drop in the house brand mix from 39.8% to 35.8% in 1H. The house brand mix in 2H improved to 37.3% while GPM declined to 40.8%. Thanked for the decrease in rent and staff costs as a percentage of revenue, which led to a slight expansion in operating profit margin. We expect that due to the keen market competition, this year's GPM will be subject to pressure of 1 to 2 ppt, and the proportion of rent to income is expected to fall further. Last year, the ratio was 11.8%. According to the management team, instead of focusing on GPM, this year it will focus more on improving sales. It will decide the pace of new store opening on the rent situation. The new stores will probably be street shops, and it is expected to help increase the market share. The company is improving its product portfolio. Facing the keen market competition, it will target more expensive big-name skin care products sales, and has grown very well so far. And the health food business is also believed can help deal with the competition. Turnover of the e-commerce business increased by 2.2%, of which Mainland China contributed over 90% of sales in the segment, demonstrating a growth rate of 10.6% over the previous year. Third party platforms were the key contributor to the sales of this segment, accounting for nearly 60% of sales. Excluding non-recurring expenses, losses from online operations narrowed from HK$29.6 million in the previous year to HK$24.8 million. The company began operating an online store on HKTVmall in Hong Kong at the beginning of 2019, and collaboration with other third-party platforms is under consideration. Turnover for the mainland China operations slightly decreased by 1.9% , while SSS in local currency terms dipped by 1.1%. The company has improved sales of own brand products and organised marketing promotion activities to stimulate sales, prompting overall sales and same store sales to rebound in Q4. We lower the target price of Sasa to 2.5, the target price-earnings ratio is 16 times(Closing price at 4 July 2019) Valuation and RiskWe give Sasa Accumulate rating, the target price-earnings ratio is 16 times, and the target price is lowered to HKD2.5. Potential risks include HK's political environment getting worse which heavily hit consumer sentiments of Chinese tourists and visitors,and local consumption not as strong as expected. (Closing price at 4 July 2019)

Financials

Click Here for PDF format...

| Recommendation on 8-7-2019 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 2.280 | | Suggested purchase price | N/A | | Target Price | $ 2.500 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|