Sectors:

Air, Automobiles (Zhang Jing)

TMT, Education, Finance (Terry Li)

Retail, Manufacturing (Tracy Ku)

Pharmaceuticals, Energy, Environment (Leon Duan)

Automobile & Air (Zhang Jing)

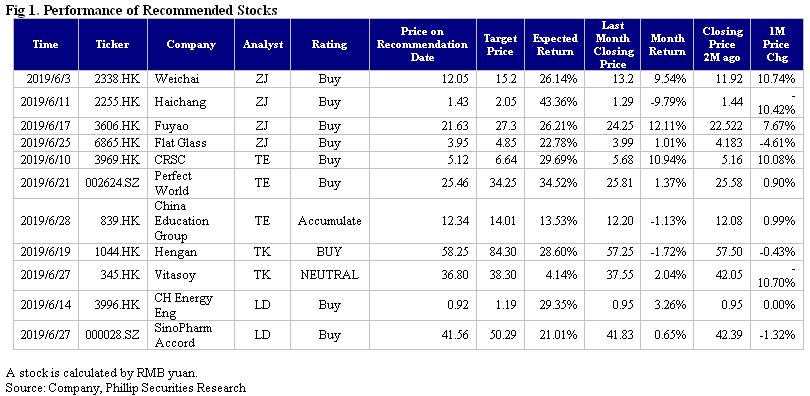

This month I released 4 updated reports of Weichai (2338.HK)¡AHaichang Ocean Park (2255.HK)¡AFuyao Glass (3606.HK) and Flat Glass (6865.HK), which got success by their unique Competitive edge. Among them, we recommend Fuyao Glass first.

After years of cultivation, Fuyao's overseas business started to develop. Overseas revenue in 2018 reached RMB8,312 million, a significant increase of 28% yoy, which was mainly due to the climbing capacity of US factories. In Q1 of 2019, the overseas revenue continued to grow rapidly and recorded a growth rate of 17% yoy. Fuyao Glass announced on January 15 to acquire the German Company SAM for EUR58.85 million. The Company started to set about consolidation from March 1 and set foot in the automotive aluminum trim strip industry. After the integration, it is expected to achieve integrated supply of aluminum trim strips and automotive glass, improve the added value of products and expand the customer base. Looking ahead, as the North American business steps on the right track, the Russian business has bottomed out and recovered, and the domestic market share continues to increase, we are optimistic that the Company's overall performance will maintain a stable growth in the future.

TMT, Education & Finance (Terry Li)

I released four reports on CRSC (3969.HK), Perfect World (002624.SZ) and China Education Group (839.HK). We highly recommend China Education Group. The Group also released the total aggregate amount of external contracts signed for the first quarter. As of 31 Mar 2019, the total aggregate amount of external contracts signed was RMB 7.48 bn, up by 16.1% YoY, in which the amount of external contracts signed in Railway was RMB 3.98 bn, up by 22.5% YoY; the amount in Urban Transit was RMB 1.86 bn, increased by 14.4%. Besides, in February this year, the National Development and Reform Commission released the National Fixed Assets Investment Development Trend Monitoring Report and the 2019 Investment Situation Outlook', indicating that infrastructure investment is expected to maintain a medium-speed growth in 2019. We believe that infrastructure projects such as transportation will be rebounded in 2019 to offset the impact from foreign trade. Finally, the plan of listing on the Science and Technology Innovation Board (STI) and has been accepted by the Shanghai Stock Exchange. As the average valuation of the A-share market is higher than that of the Hong Kong stock market, we expect the Group's valuation in STI Board to be higher than the current Hong Kong market, and could drive up the valuation in Hong Kong market in the future.

Retail & Manufacturing (Tracy Ku)

This month I released the first coverage report of Hengan(1044) and Vitasoy(345). Among the two, I recommend Vitasoy. Revenue of FY2018 increased by 16% y.o.y. On a constant currency basis, revenue and profit attributable to equity shareholders increased by 18%, which is in line with our expectations. Profit attributable to shareholders for the year increased by 20% y.o.y. which is lower than our expectation as the operation expenses are higher than we expected, and RMB depreciation. The company 's revenue of 2H increased by 9.2% y.o.y. which is significantly slower than 1H i.e. 22%. GPM remained at 53%. The profit attributable to equity shareholders fell by 5.7% y.o.y. It increased by 30.4% y.o.y. in 1H.

We expect that Vitasoy will continue to maintain steady growth this year, but the pace of growth will be more moderate, and growth will mainly be driven by sales. As the company is expected to continue to invest in branding and infrastructure, the short-term profit growth is expected to be moderate. However, we are still optimistic about Vitasoy in medium and long-term. China business is expected to continue to maintain rapid growth with the spread of channels and brand acceptance. The more mature Hong Kong market is expected to maintain steady growth.

GPM of FY2018 improved 0.8 ppt to 53.7%. According to the management team, raw material soybean price are not expected to rise sharply. The company has signed long-term contacts with suppliers to lock the price, so that soybean price can remain stable. Operation expenses for the year increased by 18.3% y.o.y. accounting for an increase of 0.6 ppt to 41.25% of revenue.

Vitasoy China grew revenue by 25%, with broad-based growth across portfolio, channels and geographies. In local currency, its revenue and profit increased by 27% and 35% respectively. According to the management team, to enhance brand awareness and equity credentials as the business expands, it has increased spending on advertising on both Vitasoy and Vita brands in view of the increasingly competitive market to secure long-term success. It has also piloted smaller scale initiatives that it intends to launch this fiscal year.

For HK operation ( HK, Macau and exports), revenue increased by 5% y.o.y. Profit from operations decreased by 4% as the company executed its announced program of infrastructure upgrade and new organisational capabilities to support the next phase of growth. Both Vitasoy and Vita brands grew revenue, together with health focused innovation, particularly its low/no sugar product ranges.

Pharmaceuticals, Energy & Environment (Leon Duan)

I released two reports on CH Energy Eng (3996.HK) and SinoPharm Accord (000028.SZ). We highly recommend SinoPharm Accord. The company's distribution business is concentrated in the Guangdong and Guangxi provinces, with Sinopharm Group Guangzhou/Guangxi companies as the core companies, ranking the first in the two markets, comprehensively covering the Grade-III and Grade-II medical institutions and retail chain terminals in Guangdong and Guangxi, covering more than 4,000 medical institutions. With the changes in the market environment, the company has transformed and innovated in the distribution field, and actively expanded its business development areas, clearly focused on the development of four business directions including retail direct sales, equipment consumables, retail diagnosis and treatment, and primary care. The company has improved supply chain management efficiency and reduced operating costs to ensure that earnings are growing through informatization reform. In 2018, the retail direct sales increased by 34% YoY, equipment consumables increased by 29% YoY, retail diagnosis and treatment increased by 49% YoY, and primary care increased by 17% YoY. As a large-scale pharmaceutical retail enterprise in China, Guoda Drugstore has 28 regional chain companies and established the logistics and distribution network including Shanghai National Logistics Center and 23 provincial and municipal distribution centers. In July 2018, Guoda Drugstore completed the introduction of Walgreens Boots Alliance (WBA), and became a Chinese-foreign joint venture after the equity transfer. WBA is a large-scale pharmacy retailer in the world. It provides health care services through the operation of pharmaceutical wholesale and community pharmacies. It also has advanced chain pharmacy management and DTP pharmacy operation experience.

Click Here for PDF format...