|

|

HOPE EDU(1765)

Analysis¡G

The Group is one the largest private higher education group in China in terms of the number of students enrolled for higher education, providing quality education and professional training to students. The Group is currently operating with 9 schools, including three independent colleges, five higher vocational colleges and one technical college. As of 31 Dec 2018, the number of student enrollment was 86,033, up by 14%, while that of new student enrollment was 31,025, rose significantly by 43%. The annual result in 2018 showed the revenue reached RMB 1.03 bn, increased by 36.8% and the core net profit jumped to RMB 310 mn, with an YoY increase of 43%. On March 5 this year, in the second session of the 13th National People`s Congress, the government work report proposed a reform and improvement of the examination methods for higher vocational colleges, and encouraged more senior high school graduates and retired military personnel, laid-off workers, migrant workers, etc to attend vocational education. This year, the student enrollment expansion of a million, we believe that the group will benefit from this expansion.

Strategy¡G

Buy-in Price: $1.05, Target Price: $1.50, Cut Loss Price: $0.85

Mos Food Services, Inc. (8153.JT)

Mos Food Services, Inc. was established in 1972. Expands restaurants via the franchise system. Includes brands, such as the hamburger specialty restaurant, ¡§Mos Burger¡¨, as well as ¡§Mother Leaf¡¨, ¡§MOSDO¡¨, ¡§mia cucina¡¨,¡§AEN¡¨, ¡§chef`s V¡¨, and ¡§GREEN GRILL¡¨, etc. Also carries out subsidiary businesses such as, hygiene control, financial/insurance agency business, and the leasing/rental of equipment, etc. For FY2019/3 results announced on 10/5, net sales decreased by 7.2% to 66.264 billion yen compared to the previous period, operating income decreased by 86.1% to 517 million yen, and net income fell into the red with ¡¶907 million yen from the previous period`s 2.385 billion yen. Repercussions from the food poisoning incident in a Mos Burger restaurant in Aug 2018 have emerged. It has fallen into the red due to the record of impairment loss and compensations for franchise operations. For its FY2020/3 plan, net sales is expected to increase by 5.6% to 70 billion yen compared to the previous year, operating income to increase by 3.1 times to 1.6 billion yen, and net income to go into the black at 1 billion yen. On 6/6, company announced the establishment of a major Filipino milling company and a joint venture company. Their first outlet will begin operations in the outskirts of Manila within fiscal year 2019. It has been 7 years since their last overseas advancement, and this will be the 9th country. Recommend to buy at ¥2210, target price ¥2610, cut loss if drop below ¥1650.

|

|

|

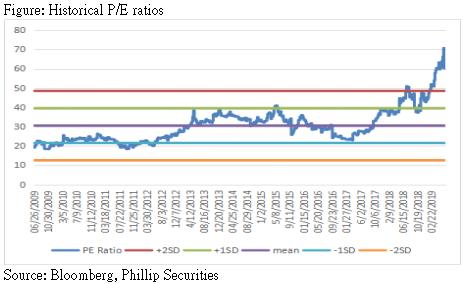

Vitasoy(345.HK) - Growth in 2H slowing down, but still with medium and long-term growth potential

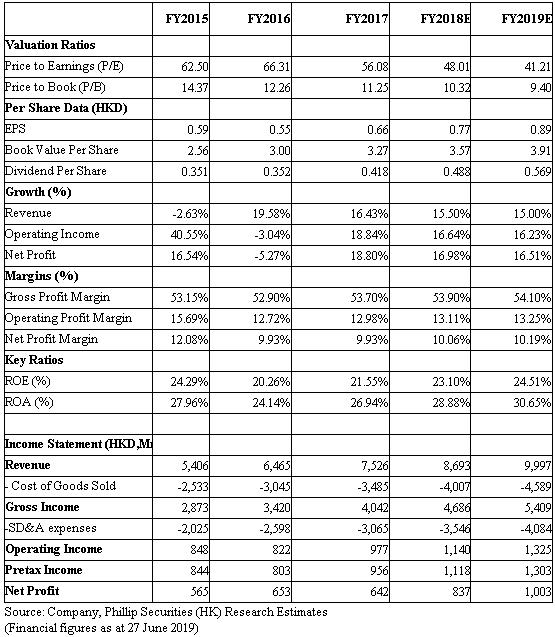

Investment SummaryRevenue of FY2018 increased by 16% y.o.y. On a constant currency basis, revenue and profit attributable to equity shareholders increased by 18%, which is in line with our expectations. Profit attributable to shareholders for the year increased by 20% y.o.y. which is lower than our expectation as the operation expenses are higher than we expected, and RMB depreciation. The company 's revenue of 2H increased by 9.2% y.o.y. which is significantly slower than 1H i.e. 22%. GPM remained at 53%. The profit attributable to equity shareholders fell by 5.7% y.o.y. It increased by 30.4% y.o.y. in 1H. We expect that Vitasoy will continue to maintain steady growth this year, but the pace of growth will be more moderate, and growth will mainly be driven by sales. As the company is expected to continue to invest in branding and infrastructure, the short-term profit growth is expected to be moderate. However, we are still optimistic about Vitasoy in medium and long-term. China business is expected to continue to maintain rapid growth with the spread of channels and brand acceptance. The more mature Hong Kong market is expected to maintain steady growth. GPM of FY2018 improved 0.8 ppt to 53.7%. According to the management team, raw material soybean price are not expected to rise sharply. The company has signed long-term contacts with suppliers to lock the price, so that soybean price can remain stable. Operation expenses for the year increased by 18.3% y.o.y. accounting for an increase of 0.6 ppt to 41.25% of revenue. Vitasoy China grew revenue by 25%, with broad-based growth across portfolio, channels and geographies. In local currency, its revenue and profit increased by 27% and 35% respectively. According to the management team, to enhance brand awareness and equity credentials as the business expands, it has increased spending on advertising on both Vitasoy and Vita brands in view of the increasingly competitive market to secure long-term success. It has also piloted smaller scale initiatives that it intends to launch this fiscal year. For HK operation ( HK, Macau and exports), revenue increased by 5% y.o.y. Profit from operations decreased by 4% as the company executed its announced program of infrastructure upgrade and new organisational capabilities to support the next phase of growth. Both Vitasoy and Vita brands grew revenue, together with health focused innovation, particularly its low/no sugar product ranges. For other markets, Australia and New Zealand business delivered 10% and 4% growth on revenue and profit respectively in local currency. Depreciation of the Australian dollars contracted revenue growth to4% and offset increment of profit. Singapore grew revenue by 7% in HKD terms, but operating profit was reduced as the company invested in brand equity and organisational capabilities. Vitasoy maintained its market leadership position in the tofu market. We expect EPS of FY2019 will be HKD0.77, with target price HKD38.3,and target price-earnings ratio 50times . (Closing price at 27 June 2019) Valuation and RiskWe expect EPS of FY2019 will be HKD0.77, with target price HKD38.3,and target price-earnings ratio 50 times .Potential risks include China market expansion missing expectations, raw material prices fluctuate significantly, and market competition has deteriorated.(Closing price at 27 June 2019)

Financials

Click Here for PDF format...

| Recommendation on 2-7-2019 | | Recommendation | Neutral | | Price on Recommendation Date | $ 36.800 | | Suggested purchase price | N/A | | Target Price | $ 38.300 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|