Investment Summary

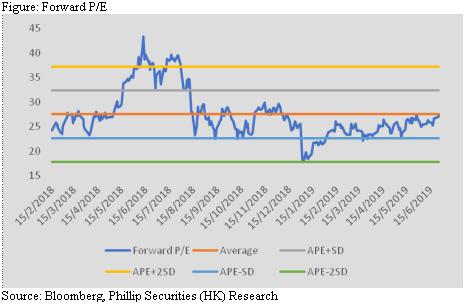

China Education Group has engaged in higher and vocational education. Under the management of the Group which are experienced in operating schools, we believe the potential improvement will be huge for the new acquired schools. However, the Group may be adversely affected by newly acquired schools, which makes the GPM reduce and the percentage of administration expenses to revenue rise. We believe it will take some time for the Group to improve the operation of the new schools. Based on the net profit attributable to owners in 2020, we assume a P/E ratio of 28x (the average of the past), deriving a TP of HK$14.01 and maintain an ¡§Accumulate¡¨ rating, with a potential upside of 13.53%.(Closing price at 26 Jun 2019)

Results Update

The Group announced interim results, wher revenue reached RMB 927 million, up by 71% YoY; net profit was RMB 344 million, increased by 34% YoY, while adjusted net profit was RMB 393 million, an increase of 42%. Gross profit margin decreased from 59.2% to 57.8%, about 1.4%, mainly due to the consolidation of newly acquired schools. The number of students in the seven schools reached 147,414, up significantly by 93%, mainly due to the addition of four schools during the group period. The organic growth was 6.3%, of which Jiangxi University of Technology rose by 11.2% YoY, while Guangdong Baiyun University and Baiyun Technician College remained a low single-digit growth. Regarding tuition fees, Jiangxi University of Technology, Guangdong Baiyun University, Baiyun Technician College, Zhengzhou Transit School and Songtian University have raised tuition fees in the 18/19 school year.

School Acquisition

On June 25, the group announced the acquisition of all the interest rights of the sponsorship of Sichuan International Studies University Chongqing Nanfang Translators College, at a consideration of RMB 1.01 billion. The school is located in Chongqing. In 2003, it became an undergraduate independent college co-organized with Sichuan International Studies University. It has two campuses, namely, Yubei and Lijiang, with a total area of 1,572 mu and offers 33 undergraduate majors, including a variety of foreign languages, international economics and trade, hotel management, advertising, Chinese international education, fine arts, music performances and so on. At present, there were 13,252 students in the school, all of whom are undergraduates, and the tuition is about RMB 14,000.

As of December 31, 2018, the total assets and net assets of Chongqing school were RMB 1.59 billion and RMB 540 million respectively. The school experienced a slight loss of RMB 19.85 million and RMB 4.005 million in both 2017 and 2018 respectively , while the financial costs for the corresponding year were RMB 61.23 million and RMB 65.57 million. Currently, the outstanding debt of the school is about RMB 510 million.

We believe that the potential of Chongqing school is huge. First, the existing school campus can accommodate of students 42% more. At the same time, the group said that because of the high standard of campus facilities, it does not require a significant amount of capex. In addition, the number of new students enrolled in schools in 2018 was about 3,500, an increase of about 150 or 4.4% from last year. Besides, the school's employment rate for graduates in the past three years is remarkable, all above 90%. From the perspective of good new enrollment and the remarkable employment rate of graduates, we believe that the quality of education for schools is high. In addition to the quality of education, there are currently only two private universities and six independent colleges in Chongqing, so the competition in the city is not very intense.

In addition, the current operating performance of the school can be further improved. First, financial costs could reduce fall sharply. Based on the data provided by the Group, the current interest rate of the school's debt is quite high, eroding most of the profits. After being acquired by the group, we believe that the school can enjoy lower interest rates, since the group announced on March 21 that it will issue a HK$2,355 million five-year convertible bond with an annual interest rate of only 2%. If the financial cost reduces, the school is expected to able to make a profit. Moreover, schools can also save brand usage fees and reduce labour costs by optimizing teacher-student ratio. In view of the fact that the current programs are all undergraduates, the group said that it could provide associate-degree programs in the future to raise its revenue.

The enterprise value of Chongqing school is about 1.51 billion (acquisition price plus 510 million outstanding loans and minus 10 million working capital), implying CY2019 EV/EBITDA about 12.2 times, we think the valuation is reasonable.

Earnings Forecast

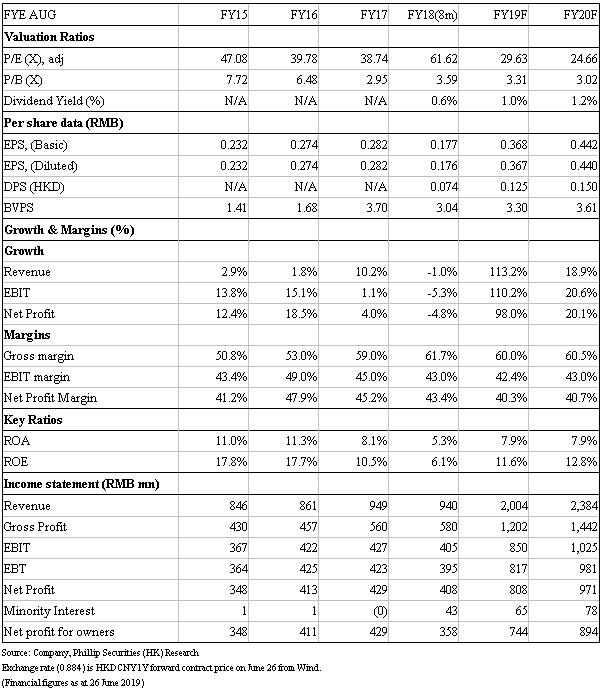

Due to the newly acquired schools, the Group's gross profit margin has dropped significantly. The administrative expenses as a percentage of revenue has also increased. We believe that it will take some time for the Group to improve the operation of the new schools. Therefore, the results in 2019 will be affected. In view of this, we cut the gross profit margin for 2019/20F by 2.3%/2.2%, and also increase the administrative cost as % of revenue in 2019/20F by 2%/2.7%, resulting in a decrease of 8.4%/10.3% in net profit for 2019/20F. Besides, we did not include Chongqing schools this time.

Valuation

Based on the net profit attributable to owners in 2020, we assume a P/E ratio of 28x (the average of the past), deriving a TP of HK$14.01, 9.7% lower than previous TP, due to the dropping GPM, rising percentage of administration expenses to revenue and the deprecation in RMB. We maintain an ¡§Accumulate¡¨ rating, with a potential upside of 13.53%.(HKD/CNY=0.884)

Risk

1. A plunge in birth rate in China

2. A sharp change in policies to education sector

3. The Group fails to improve the operation of the acquired schools

Financials

Click Here for PDF format...