Investment Summary

Perfect World engaged in Film and TV series creation as well as Gaming development in China, together with strong game development and film production capabilities. Assuming a target P/E of 23x in 2019, we derived a TP of $34.25, 9.1% lower than previous TP. Due to the recent slump in stock price, we update to a ¡§Buy¡¨ rating, with a potential upside of 34.5%. (Closing price at 18 June 2019)

Annual result update

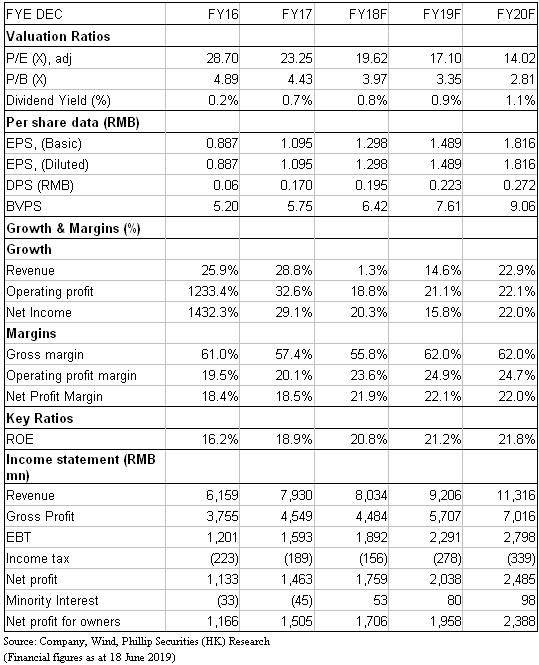

The Group announced its 2018 annual results and the first quarter of 2019. In 2018, the Group's revenue was RMB 8.034 billion, a slight increase of 1.3% YoY. Among them, the gaming business revenue declined slightly by 4%, about RMB 5.42 billion, we believe that the decline was due to the suspension of the gaming license approval. The revenue from the film and television business recorded a growth of 14.6%, reaching RMB 2.61 billion. During the period, the gross profit margin decreased from 57.4% to 55.8%. The net profit attributed to owners was RMB 1.71 billion, a YoY increase of 13.4%.

In the first quarter of 2019, the revenue reached RMB 2.04 billion, up by 13.3%; the net profit attributed to owners was RMB 490 million , a YoY of 35%. Gross profit margin reached 68.1%, an increase of 6.8% YoY.

Business update

Regarding PC games, the group's classic PC games "Zhu Xian" and "Perfect World International Edition" continue to bring stable income. During the period, the group launched a PC and console dual-platform game "Subnautica", which is a submarine survival game, similar to "Minecraft". Currently, "Subnautica" has a 94% favorable rate in Steam, a gaming platform, and the score from the game rating website IGN was also 9.1 points, showing is widely welcomed by players. In addition, the Group is also developing the different PC games for example "Zhu Xian New World", "Perfect World" host version and PC and console dual-platform games "DON`T EVEN THINK", "Torchlight II", "Magic The Gathering", etc. , we believe it will bring new momentum to the gaming business.

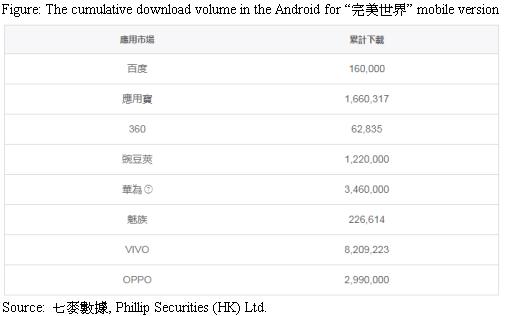

In relation to mobile games, the mobile games launched in 2018 performed well, such as ¡§½ü¦^³Z¡¨, ¡§¯P¤õ¦pºq¡¨ and ¡§ªZªL¥~¶Ç¤â¹C¡¨. In addition, in 2019, the ¡§§¹¬ü¥@¬É¡¨ mobile version developed by the group was officially launched, and the results were excellent. The number of new users on the 12-hour exceeded 2.6 million. It reached the first in iOS free list on the first day, then reached the top in free list and the best-selling list on the forth day. According to the forecast of ¡§¤C³Á¼Æ¾Ú¡¨, the cumulative download volume in the Android has reached 18 million times as of 18 June. In addition, according to ¦÷°¨¼Æ¾Ú, ¡§§¹¬ü¥@¬É¡¨ mobile version ranked third on May in terms of revenue, only after "¤ýªÌºaÄ£" and "©M¥ºë^". The group will also launch mobile games such as ¡§¯«ÀJ«L«Q2¡¨, ¡§·s¯«Å]¤j³°¡¨, ¡§·s¯º¶Æ¦¿´ò¡¨, ¡§§Úªº°_·½¡¨. Due to the suspension of the gaming license approval, the revenue of gaming revenue has dropped, but we believe game revenue growth will resume as the approval restarted again in 2019.

The growth of Group's TV drama revenues was robust in 2018, a YoY increase of 55%. During the year, the Group launched a series of high-quality TV series such as ¡§§Q¤b¥XÀ»¡¨, ¡§¯P¤õ¦pºq¡¨, ¡§©¿¦Ó¤µ®L¡¨, ¡§Âk¥h¨Ó¡¨, ¡§¨«¤õ¡¨, ¡§»»e¨I¨IÂu¦p¡¨, and achieved satisfactory results. Among them, ¡§¯P¤õ¦pºq¡¨ recorded the third highest number of views among online dramas in 2018, more than 8 billion; the online views of ¡§Âk¥h¨Ó¡¨ also hit 10 billion;¡§»»e¨I¨IÂu¦p¡¨ ranked the first in both program rating and online views, where the views exceeded 1.5 billion. It also won many awards such as the Bull Ear Prize, Weibo Annual Hot Drama, and Yien's Most Valuable Drama. In the first quarter of 2019, works such as ¡§«C¬K°«¡¨ and ¡§¶X§ÚÌÁÙ¦~»´¡¨ have been launched. We believe that film and television revenue will rise steadily this year.

Valuation

As the revenue growth was lower than expected , we lower the revenue in 2019F by 7.1%, but we believe the Group will regain its growth in 2019 thanks to the more positive industry environment and its latest mobile game. Assuming a target P/E of 23x in 2019, we derived a TP of $34.25, 9.1% lower than previous TP. Due to the recent slump in stock price, we update to a ¡§Buy¡¨ rating, with a potential upside of 34.5%.

Risk

1. Lower-than-expected growth in Mobile gaming

2. Giant entering the film & drama production

3. Loss in production team

Financials

Click Here for PDF format...