Investment Summary

Comprehensive solution provider with complete industry chain in Power sector

The company is an ultra-large group company providing comprehensive solutions and full-chain services in the energy, power, infrastructure and real estate industries in China and all over the world. Its main business covers the fields of energy, power, waterworks, railways, ports, municipal engineering, urban rail, ecological environment protection and housing construction, it has a complete industrial chain integrating planning consultation, assessment and review, survey and design, engineering construction and management, maintenance and investment operation, technical services, equipment manufacturing and building materials. It provides customers with one-stop integrated solutions and full lifecycle management services, and it also participates in power engineering construction projects in more than 80 countries and regions in China and overseas.

The main force of ¡§One Belt One Road¡¨ construction, international business is expected to recover

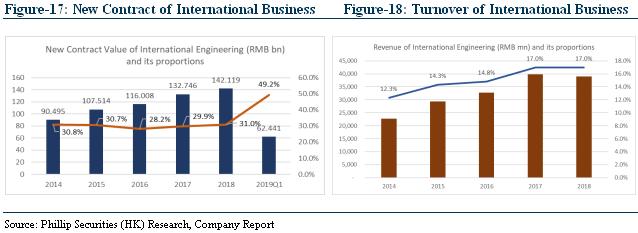

In the first quarter of 2019 and 2018 full year, the company achieved brilliant results in the international business: in the first quarter of 2019, the company signed total RMB126.886 billion of the new contract, completing 26.41% of the planned annual new contract, decreasing by 4.76% YoY; the value of international new contracts signed was RMB62.441 billion, representing a significant increase of 48.92% YoY. In 2018, the value of international new contracts was RMB142.119 billion, accounting for 31% of the company''s new contracts signed in the year, increasing 7.06% YoY; among them, the number of newly signed contracts for international power projects reached RMB118.434 billion, increasing 26.18% YoY; the international contracting project realized a new contract value of RMB131.8 billion, an increase of 17.79% YoY; the ¡§One Belt One Road¡¨ market achieved a new contract value of RMB106.673 billion, a YoY increase of 37.97%. It is expected that the company will continue benefitting from the ¡§One Belt One Road¡¨ policy, and as the main force of construction, the company will have more overseas orders in the future.

Rapid growth of non-power business helps to expand the ¡§mega building¡¨ market landscape

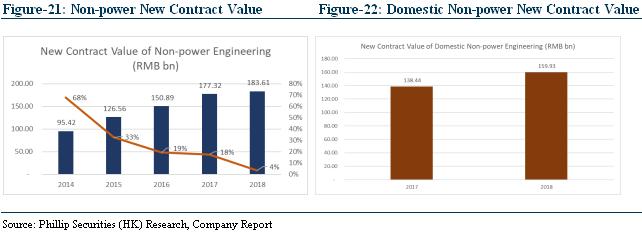

The company extensively develops domestic non-power fields such as transportation, municipal, ecological and environmental protection, mining, shantytown renovation, park development, and housing construction. In 2018, the company''s new contract value of non-power engineering business was RMB183.613 billion, representing a YoY increase of 3.55%, accounting for 39.75% of the total value of contracts signed throughout the year. Among them, the domestic non-power engineering business realized a new contract value of RMB159.928 billion, accounting for 50% of the company''s new domestic contract value for the first time, an increase of 15.52% YoY. The newly signed contract value of PPP project exceeded RMB100 billion for two consecutive years. Due to the higher gross profit margin of non-power services compared to the traditional power business, it¡¦'s expected that the rapid development of the company''s non-power business will strongly support the company''s revenue and gross profit.

Initial coverage with TP of HK$ 1.19 and investment rating of ¡§BUY¡¨

Based on the valuation level of sector average, we initiate coverage on China Energy Engineering Corp. with 6.96x/6.44x FY19/FY20 PER and 0.64x/0.58x FY19/FY20 PBR and ¡§BUY¡¨ investment rating, corresponding to TP HK$ 1.19 with a 29.3% potential upside compared with current price HK$ 0.92 as of June 11, 2019.

Industry Analysis

Global power generation is growing steadily, new energy power generation will dominate in the future

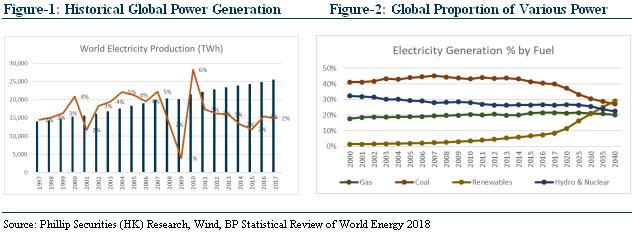

From 1997 to 2017, global power generation increased from 14,002 TWh to 25,551 TWh, corresponding to a CAGR of 3.1%, and it¡¦'s expected to continue maintaining stable growth. According to the statistics of the International Energy Agency (IEA), the total population of the countries along the ¡§One Belt One Road¡¨ is about 4.6 billion, and the electricity consumption per capita is 1,600 kWh/year, which is much lower than the global average of about 3,100 kWh/year. It is estimated that by year 2030, the new installed capacity will exceed 1 billion kW, with a CAGR of 4%. In terms of power generation, fossil fuel power generation still dominates in various power generation modes. In 2017, coal-fired power generation accounted for 39.9% of all kinds of power generation, and gas-fired power generation accounted for 21.6%. However, due to national policies and power generation efficiency, the proportion of coal-fired power generation is decreasing year by year. According to the statistics of BP Statistical Review of World Energy 2018, it is estimated that by 2040, renewable energy generation will account for 29% of power generation of the whole year, which will exceed coal-fired power and become the main power generation method.

Power industry''s growth tends to be stable, and clean energy power generation is growing rapidly in China

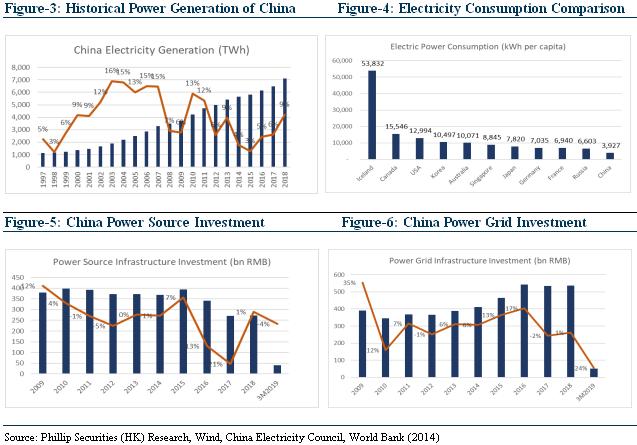

Electricity is a basic industry related to the national economy and the people''s livelihood, the power industry has maintained rapid growth for a long time in China. From 1997 to 2018, the annual power generation increased from 1,136 TWh to 7,112 TWh, with a CAGR of 9.1%. At the same time, the cumulative installed capacity of power generation increased from 254 GW to 1,900 GW, with a CAGR of 10.1%. At present, China''s annual power generation and installed capacity are the highest in the world. In the first quarter of 2019, the power source infrastructure investment was RMB40.6 billion in China, with a decrease of 4% YoY. The power grid infrastructure investment was RMB50.2 billion, decreasing by 24% YoY. The total power investment was RMB90.8 billion, decreasing by 16% YoY. It¡¦'s expected that China will accelerate the progress of power investment in the second quarter of 2019 and the investment of power generation project of China is expected to be RMB273.21 billion, with an increase of 0.4% YoY. The power grid project is expected to invest in RMB540.72 billion, increasing by 0.64% YoY. The total investment of power industry is expected to be RMB813.93 billion, representing an increase of 0.56% YoY, and the development is relatively stable. According to the ൕth Five-Year Plan for Power Development" in China, it is estimated that the total electricity consumption will reach 6.8-7.2 TWh in 2020, with a CAGR of 3.6%-4.8%; the total installed capacity will reach 2 billion kW, with a CAGR is 5.5%; the per capita electricity consumption is 4,860-5,140 kWh, with a CAGR of 3.2%-4.4%. According to the -2019 National Electricity Supply and Demand Situation Analysis and Forecast Report" and the World Bank data, the per capita electricity consumption of 4,956 kWh in 2018 China is still significantly lower than that of western developed countries, the power industry has a space for development.

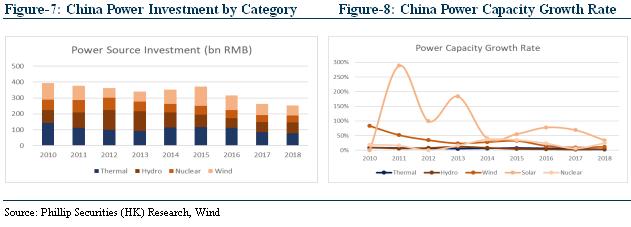

With the introduction of energy conservation and emission reduction and clean energy development policies in China, the proportion of non-fossil energy consumption will increase to 15% in 2020, and the proportion of non-fossil energy power generation capacity will increase to 39%, and non-fossil energy power generation will increase to 31%, according to the ¡§13th Five-Year Plan for Power Development¡¨. Specifically, the wind power installed capacity will reach 210 million kW, solar power installed capacity will reach 110 million kW, nuclear power installed capacity will reach 58 million kW, and conventional hydropower installed capacity will reach 340 million kW. As the development of new energy power continues to accelerate, in 2018, the growth rates of solar, nuclear, wind, hydro and thermal power generation capacity were 34%, 25%, 13%, 3% and 3%, respectively. Judging from the investment in different power projects, the investment in traditional thermal power tends to decrease and the investment in new energy power is expected to continue growing.

China''s infrastructure investment remains stable, and the global non-power market is vast

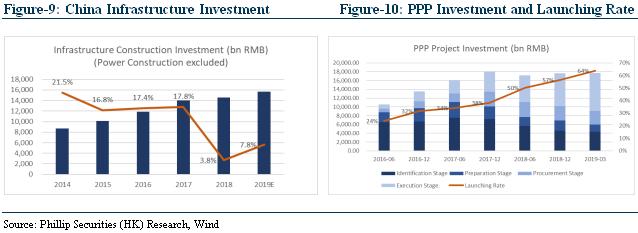

After high-speed growth in many years and affected by the city''s investment and financing difficulties, China''s infrastructure investment (excluding power) increased by only 3.8% YoY in 2018, which hit a record low. In order to stabilize investment in related fields, the Chinese State Council issued the ¡§Guiding Opinions of the General Office of the State Council on Maintaining Efforts to Remedy Shortcomings in Infrastructure Field¡¨ on October 31, 2018, and proposed to prevent the ups and downs in infrastructure investment; on December 29, the 13th National People''s Congress Standing Committee seventh meeting also approved a new debt limit of RMB1,390 billion for infrastructure investment shortfalls, including a new general debt limit of RMB580 billion and a new special debt limit of RMB810 billion; China Development and Reform Commission also pointed out that as the country increased the support for the infrastructure sector, infrastructure investment is expected to maintain a medium-speed growth in 2019 when looking into the fixed assets investment situation in 2019. According to the prediction of the Chinese Academy of Social Sciences, the fixed assets investment of the whole society will reach RMB81.4 trillion in 2019, with a nominal growth of 5.6% and an actual increase of 0.4%. Among them, real estate investment and infrastructure investment will increase by about 6.3% and 7.8%, respectively, continuing to be the main force for stable investment and stable growth.

According to the China PPP service platform project management library, by the first quarter of 2019, the total number of PPP projects in China reached 12,569, and the total planned investment amounted to RMB17.69 trillion. The PPP project launching rate gradually increased from 24% in June 2016 to 64% in March 2019. Affected by strict supervision policies such as No. 92, No. 54 and asset management new regulations, the number and scale of PPP projects in 2018 experienced a downward trend compared with 2014 to 2017. However, with the end of the ultra-large clean-up of the PPP project library and the demand for PPP projects caused by infrastructure remedying shortcomings, it is expected that the scale and launching rate will maintain steady growth in the future.

In addition, according to the Global Infrastructure Outlook released by the Global Infrastructure Hub (GIH), global infrastructure investment will reach 3.7 trillion US dollars per year by 2040, of which Asia and Africa countries account for 60% (about 2.2 trillion US dollars), the infrastructure construction has a vast market.

Company Analysis

Company Profile

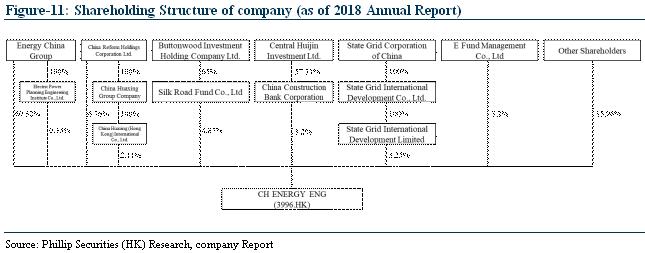

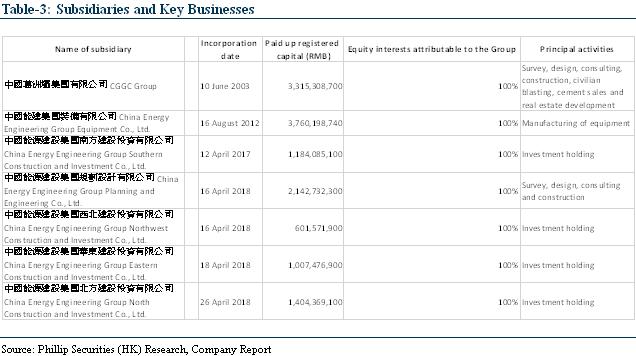

The company is a comprehensive and ultra-large group company offering holistic solutions and full-chain services in energy power, infrastructure and real estate sectors in China and the world at large. It is a joint stock company founded on December 19, 2014 with limited liability established and co-sponsored by China Energy Engineering Group Co., Ltd. (a central enterprise supervised and administered by the State-owned Assets Supervision and Administration Commission of the State Council) and its wholly-owned subsidiary Electric Power Planning and Engineering Institute Co., Ltd. Its businesses cover energy power, waterworks and waterworks, railways and highways, ports and navigation channels, municipal engineering, urban rail, eco-environment protection and housing construction. Since establishment, the company won more than 600 science and technology awards at state and provincial levels, 6 China Construction Engineering Luban Prizes and 25 National Quality Engineering Gold Awards. As of the end of 2018, the company had 2 state-level enterprise technology centers, 4 academician expert workstations, 10 post-doctoral research and development workstations, 46 provincial research institutions and 84 high and new technology enterprises. It had a total of 8,787 patents in force. The company has set up over 200 branch offices in more than 80 countries and regions across the world with its businesses extending to over 140 countries and regions outside China. On 10 December 2015, the company issued H shares under the initial public and got listed on the main board of The Stock Exchange of Hong Kong Limited (Stock Code: 3996).

The history of the Company dates back to the 1950s, when the predecessors of most of its subsidiaries engaged in the business of survey and design, construction and contracting, and equipment manufacturing in the power industry were established. On September 28, 2011, pursuant to the Approval from the State Council on the Issues Regarding the Establishment of China Energy Engineering Group Co., Ltd., Energy China Group, the Controlling Shareholder of the company, was established as a wholly state-owned company consisting of CGGC Group, CPECC and survey and design enterprises, construction enterprises, and building and repairing enterprises owned by State Grid Corporation of China and China Southern Power Grid company Limited, respectively, in 15 provinces and regions in the PRC at the time. On December 19, 2014, the company was established as a joint stock company with limited liability in the PRC. During the Reorganization, Energy China Group injected all of its principal businesses and assets into our company, and we have developed into one of the largest comprehensive solution providers for the power industry in China and globally.

Key Business Analysis

The company is one of the largest comprehensive solution providers in the power industry in China and in the world. It provides customers with one-stop integrated solutions and full lifecycle management services. With a strong business advantage across the entire industry chain, particularly in the field of survey and design, the company can provide customized integrated solutions for power projects. The business of the company is mainly divided into the following sections:

1. Survey, design and consulting services business

The survey, design and consulting services business is a core and pivotal business segment of our overall business. The company provides provide survey and design services for large-scale power generation projects, covering all major power sources, and grid projects in China and abroad. In addition, the company also provides a broad range of consultancy services, including policy consultation for the power industry and evaluation, assessment and supervision of power projects. The subsidiary of the company, CPECC, is a national power design group which owns 6 regional power design institutes. We also own 14 out of 31 provincial power design institutes in China and one power design institute in Lithuania.

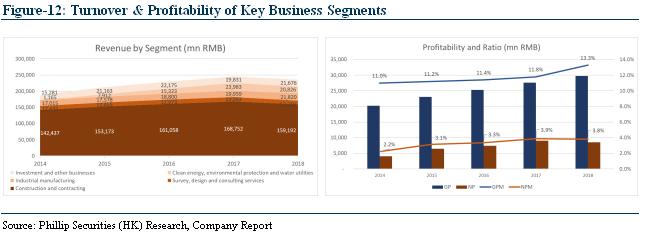

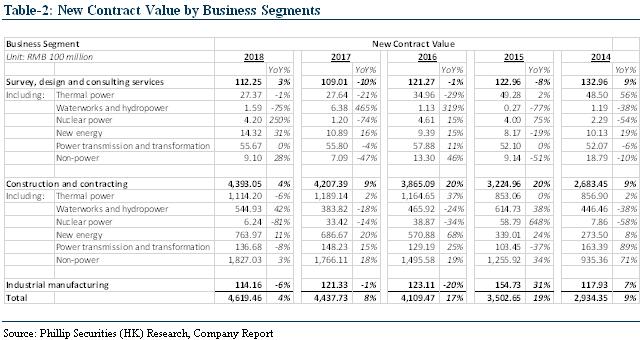

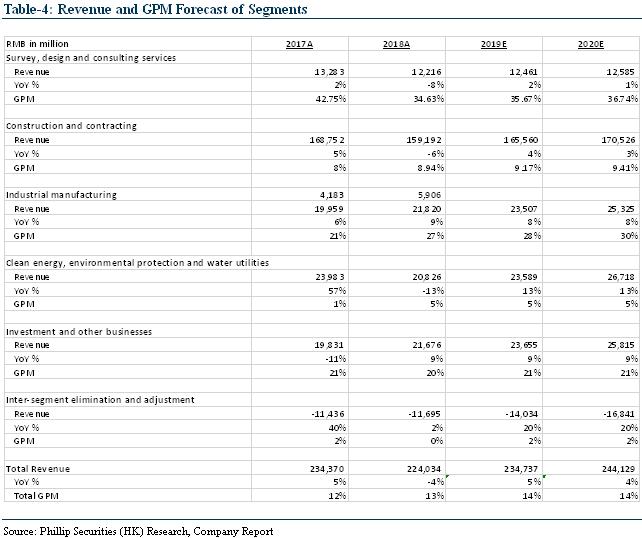

In 2018, the revenue before inter-segment elimination of survey, design and consulting services business was RMB12.22 billion, representing a YoY decrease of 8.03%. The newly signed contract value of the survey, design and consulting services business was RMB11.225 billion, a YoY increase of 2.97%, accounting for 2.43% of the new contract value for the whole year of the company. As of December 31, 2018, the outstanding contract value of the survey, design and consulting services business was RMB31.161 billion.

1. Construction and contracting business

The construction and contracting business is the core and largest business segment of the company. The company has world-class construction and contracting capabilities. It primarily undertakes large-scale power generation projects, covering all major power sources, and power grid projects in China and abroad. In addition, it undertakes other infrastructure projects. The company is one of the largest power construction and contracting service providers in China, providing engineering construction services through 32 subsidiaries including CGGC Group and their respective subsidiaries. By 2018, the company has set up over 200 branch offices in more than 80 countries and regions across the world with its businesses extending to over 140 countries and regions outside China.

In 2018, the revenue before inter-segment elimination of the construction and contracting business segment was RMB159.919 billion, a YoY decrease of 5.66%. The new contract value of the construction and contracting business was RMB439.305 billion, a YoY increase of 4.41%, accounting for 95.1% of the total new contract value. Among them, 1) the newly signed contract value of thermal power construction and contracting business was RMB111.42 billion, representing a decrease of 6.3% YoY, which was affected by the decline of investment in domestic coal-fired power construction, while the scale of thermal power project construction business still maintained the global leading level; 2) the value of new contracts of waterworks and hydropower project construction and contracting business was RMB54.493 billion, a YoY increase of 41.97%. Among which, the value of new contracts in China and overseas increased by 72.36% and 26.99% respectively; 3) the new contract value of nuclear power construction and contracting business was RMB624 million. a decrease of 81.33% YoY, as a result of the tender projects for domestic nuclear power construction decreasing stage-by-stage; 4) the new contract value of the new energy construction and contracting business was RMB76.397 billion, an increase of 11.26% YoY, shinning out in China¡¦'s and the global new energy construction market at large; 5) the newly signed contract value of the power transmission and transformation construction business was RMB136.68, a decrease of 7.79% YoY; 6) the new contract value of non-power construction and contracting business was RMB182.703 billion, a YoY increase of 3.45%, accounting for 39.75% of the new contracts for the whole year in the company, which became an important growing point for the company''s business. On December 31, 2018, the outstanding contract value of the construction and contracting business was RMB1,027.161 billion.

2. Industrial manufacturing business

The industrial manufacturing business mainly includes cement production, civil explosives and equipment manufacturing businesses. The company is the largest supplier of auxiliary equipment for power plants in China with a full range of product offerings and advanced technology. The company engage in the design, manufacturing and sales of equipment for various segments of the power industry, and have the ability to provide complete sets of equipment for large power plants. The products of company include auxiliary equipment for power plants, power grid equipment, steel structure and energy-efficient equipment. The company is one of the three largest designers and manufacturers of flue gas and dust removal equipment (for 1000 MW and above generation units) in China. It is also the only enterprise in China which is capable of designing and producing seawater filter and cathode protection systems for 1000 MW nuclear power plants. It has constructed the world¡¦'s first vertically mounted drum filter trial platform. The company independently developed ¡Ó800 kV UHV dry-type flat wave reactor, 1000 kV UHV AC series compensation damping reactor, and casting technology for ceramic-metal composite wear-resistant parts employed advanced technologies in their respective fields. The company designs, develops and manufactures various power equipment through CEEEC and other subsidiaries, and has received nearly 100 awards for self-developed products and technologies.

CEEEC, the core subsidiary in equipment manufacturing, is a member of Nuclear Power Equipment Localization R&D Joint Center, and the first domestic enterprise holding the Civilian Nuclear Pressure Equipment Manufacturing License issued by the National Nuclear Safety Administration. The civil explosives business is mainly conducted through one subsidiary, Gezhouba Explosive Company. The company conducts cement production business mainly through its subsidiary, Gezhouba Cement Company. As one of the 60 large cement groups supported by government, Gezhouba Cement Company has the largest production base of specialty cement in China.

In 2018, the revenue before inter-segment elimination of industrial manufacturing business was RMB21.82 billion, representing a YoY increase of 9.32%. Specifically, the revenue before inter-segment elimination of cement manufacturing business was RM8.90 billion, representing a YoY increase of 33.23%; the revenue before inter-segment elimination of civil explosives business was RMB3.18 billion, representing a YoY increase of 4.95%; the revenue before inter-segment elimination of equipment manufacturing business was RMB9.74 billion, representing a YoY decline of 4.98%.

1. Clean energy, environmental protection and water utilities business

The clean energy environmental protection and water utilities business included businesses such as clean energy environmental protection and water utilities. In 2018, the revenue before inter-segment elimination of the business was RMB20.83 billion, representing a YoY decrease of 13.16%. Among which, the revenue before inter-segment elimination of clean energy business was RMB1.31 billion, representing a YoY increase of 3.15%; the revenue before inter-segment elimination of environmental protection business was RMB18.06 billion, representing a YoY decrease of 18.65%; the revenue before inter-segment elimination of waterworks business was RMB1.46 billion, representing a YoY increase of 186.27%.

1) The company sped up the approval and construction paces of new energy investment projects in China, and boosted a number of wind power projects such as in XilinGol League in Inner Mongolia, Xinfeng in Guangdong and Ruyang in Henan, PV projects such as the aquaculture-solar hybrid project in Qingyuan, Guangdong, and the greenhouse-roof solar power generation project in Yongjia, Zhejiang, as well as a number of ongoing engineering projects such as the comprehensive use of straw in Suihua, Helongjiang, and the biomass combined heat and power generation project in Ye County, Henan. The Hai Duong fossil-fuel power project in Vietnam invested by the Company represents so far the biggest single investment in thermal power project by a Chinese company in Vietnam, and the project is under construction as scheduled. The SK hydropower project in Pakistan is so far the largest hydropower project invested and constructed by a Chinese enterprise in overseas markets, and also a key project in the first priority list for the China¡VPakistan Economic Corridor development. The projects are under construction as scheduled.

2) The company¡¦'s comprehensive strength in the renewable resource business ranks among the top industry-wide. It owns advanced sorting, cleaning, and processing technologies and extends its business reach with the environmental protection industrial park as the center. It gradually structures a national recycling, processing and sales system for renewable resources which is capable of recycling and reusing a vast majority of types of renewable resource across the country. The company invested to acquire Rizhao Sainuo Environment Science and Technology Company Limited, paving the way for the Company to march into waste water treatment membrane manufacturing sector, in which the company¡¦'s core technologies boast leading advantages nationwide.

3) In 2018, the company¡¦'s waterworks operation and management capabilities were continuously strengthened. The company operated and managed 58 water plants, 1,000-plus kilometers of pipes and 33 pump stations. Its designed water handling capacity is up to 3 million tonnes/day and is distributed across Beijing, Tianjin, Shandong, Henan, Hebei, Hunan, Hubei, Sichuan, Zhejiang and other regions, with its business layout becoming increasingly improved. The company actively develops international waterworks projects in Brazil and other places, and has completed the acquisition of 100% equity interest in San Noronso Water Supply project in Brazil, with a concession right lasting 25 years. The project is capable of supplying 410,000 tonnes of water per day and was officially put into commercial operation in July 2018, delivering sound operational benefits.

1. Investment and other business

The company invests in other infrastructure projects (such as roads) and engages in real estate development. In 2018, the revenue before inter-segment elimination of investment and other businesses was RMB21.68 billion, representing a YoY increase of 9.30%. Among which, the operating revenue of real estate business was RMB7.44 billion, representing a YoY increase of 17.91%; the revenue of expressway business was RMB1.92 billion, representing a YoY increase of 20.75%; the revenue of financial business was RMB240 million, representing a YoY increase of 200.00%; the revenue of other businesses was RMB12.08 billion, representing a YoY increase of 1.94%.

As one of the 16 enterprises approved by SASAC to engage in real estate business as one of their principal businesses, CGGC, one of the company¡¦'s subsidiaries, engages in real estate development operations through two real estate subsidiaries with Grade A qualifications in Beijing and Wuhan, namely, Gezhouba Real Estate Company, one of the Top 100 real estate enterprises in China, and China Gezhouba Group Properties Co., Ltd..

In 2018, the company¡¦'s expressway operation business welcomed steady growth, with its brand presence further enhancing. The total mileage of expressway operated by the company was 457 kilometers, including G55 (Xiangyang, Hubei-Jingzhou section), G45 (Hubei Macheng-Xishui section), Sichuan Neijiang-Suining expressway and Shandong Jitai expressway connection, the operations of which were in good condition with the traffic flow growing significantly on a YoY basis. The 10 in-construction expressways undertaken by the company including the Sichuan Bawan Expressway and the Shaanxi Yanchang-Huanglong Expressway stretch for a total of 1,077 kilometers and are progressing as scheduled.

The financial business of the company includes the financial business for financial companies (loans, entrusted loans and guarantees for member enterprises), finance leases and industrial funds. In 2018, the capital concentration of the company was significantly elevated YoY, and the deposit balances and the loan balances by financial companies increased by 86.2% and 112.38% YoY, respectively. The company joined hands with commercial banks in launching syndicated loans to activate external financing, which has played an important role in bringing down the company¡¦'s liability level and financial expense. The company set up fund management joint ventures with advantageous enterprises in the industry to utilize social capital to boost the company¡¦'s businesses in new business models and investment businesses of the company.

Investing Highlights

Leading enterprise in power industry, the number of patents continues to grow

The company is in the Fortune¡¦'s Global 500 and the China Enterprise Confederation¡¦'s Top 500 Chinese Enterprises. The company took the 12th place in the 2018 ENR Top 250 Global Contractors, the 21st place in the ENR Top 250 International Contractors, the 4th place in the ENR Top 150 Global Design Firms, and the 18th place in the ENR Top 225 International Design Firms, which is the leading enterprise in power industry in China and globally. According to Frost Sullivan¡¦'s report, in 2014, the top three power engineering and construction enterprises in China accounted for 66.5% of new contract value of overseas power contracting projects. Among the three enterprises mentioned above, Energy China ranked first, with a new contract value of USD10.6 billion and a market share of 35.6%. Companies ranked second and third had a market share of 25.1% and 5.9%, respectively. In terms of the domestic market, the survey and design market share of fossil-fuel power plant (in terms of completed contract value in 2014), 330 kV and above power transmission lines and UHV transmission lines (in terms of length installed in 2014) and the conventional islands for nuclear power plants (in terms of the total installed capacity of all units put into operation or under construction as of March 31, 2015) were all ranked the first, accounting for 81.1%, 52.6%, 73.7% and 90.8%, respectively; the power construction market share of fossil-fuel power and hydropower plants (in terms of completed contract value in 2014) and the conventional islands for nuclear power plants (including both installation and civil works, in terms of installed capacity of the construction and operation as of March 31, 2015) accounted for 57.6%, 22.8%, 59.8% and 29.7%, respectively, which is in a leading position in the industry.

The company has a significant competitive advantage in the power construction market, especially in the fossil-fuel and nuclear power construction market, and the total installed capacity of the power plants constructed by the company from 2012 to 2014 exceeded 160 GW, ranking first in the world. In the field of fossil-fuel power, the company participated in the construction of 69 units out of the 75 fossil-fuel power generation units of 1000 MW in China. In the field of hydropower, the company participated in the construction of 27 power stations out of the 45 large-scale power stations of 1200 MW and above, accounting for 75.1% of the total installed capacity of those large-scale power stations in China as of the end of 2014.

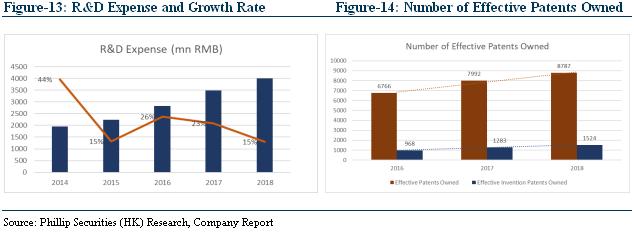

In 2018, the research and development expenses amounted to RMB4,004 million, representing a YoY increase of 14.54%. The company focused on the scientific and technological research and development work in clean fuel-fired power generation, new energy, intelligent power grids, environmental protection, engineering safety and other fields, and obtained 1,280 patent licenses, including 229 invention patents, with the patents in force of the company adding up to 8,787, including 1,524 invention patents. For the latest three years, the number of effective patents owned by the company increased significantly from 6,766 in 2016 to 8,787 in 2018, with an average annual growth rate of 13.96%. Specifically, the effective invention patents owned increased from 968 in 2016 to 1,524 in 2018, with an average annual growth rate of 25.47%. We believe that the increasing investment of R&D and effective application of patents can help the company overcome technical difficulties, effectively seize the technical commanding heights of the industry, and continue creating significant economic and social benefits to the company.

Order reserve is sufficient, international business is growing rapidly

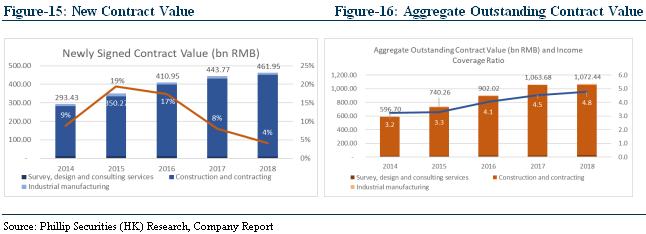

In 2018, the new contract value was RMB461.946 billion, an increase of 4.1% YoY, which was because that company decided to improve the quality of the projects contracted. Among them, the domestic new contract value was RMB319.827 billion, representing an increase of 2.83% YoY; the international new contract value was RMB142.119 billion, a YoY increase of 7.06%. As of year 2018, the outstanding contract value was RMB1,072.436 billion, an increase of 1% YoY. The income coverage ratio was 4.8x, compared with 4.1x and 4.5x in 2016 and 2017, respectively. The reserves are in good condition and the short-term growing performance of the company is promising.

In the first quarter of 2019, the new contract value was RMB126.86 billion, accounted for 26.41% of the annual new contract value planned, with a decrease of 4.76% YoY. The domestic new contract value was RMB64.445 billion, representing a YoY decrease of 29.41%; the international new contract value was RMB62.441 billion, representing a significant increase of 48.92% YoY. As for business, the new contract of power engineering business was RMB82.919 billion, a YoY increase of 13.77%, which was affected by a large increase of international new contracts and reduction of domestic contracts; the new contract value of the non-power engineering business was RMB43.967 billion, representing a decrease of 27.14% YoY. Because of the adjustment of power supply structure, PPP policy and lagging effect, the overall new contract value in Q1 2019 decreased. The company believes it¡¦'s a temporary phenomenon, the number of new domestic contracts will be greatly improved in the Q2 and Q3 of 2019.

In 2018, China¡¦'s enterprises signed 7,721 new contracts of overseas contracted engineering projects in countries along the ¡§One Belt and One Road¡¨, with a value of 125.78 billion US dollars, accounting for 52% of all the newly signed contracts of overseas contracted engineering projects of China in the same period, registering a YoY decrease of 12.8%. A turnover of 89.33 billion US dollars was completed, accounting for 52.8% of the total amount of the same period, up by 4.4% YoY. The international business in the first quarter of 2019 and year 2018 achieved brilliant results. In 2018, the company signed new international contracts valuing RMB142.119 billion throughout the year, accounting for 31% of the company¡¦'s annual newly signed contracts in total, up by 7.06% YoY. The company¡¦'s international businesses developed rapidly, with the direct new contracts with foreign organizations valuing RMB125.9 billion, up by 23.11% YoY. The new contracts of international power engineering projects valued RMB118.434 billion, up by 26.18% YoY. The company newly signed international EPC contracts valuing RMB131.8 billion, up by 17.79% YoY. In ¡§One Belt and One Road¡¨ market, the company¡¦'s newly signed contracts valued RMB106.673 billion, up by 37.97% YoY. We expect the company will continue benefitting from the ¡§One Belt One Road¡¨ policy, and as the main force of construction, the company will have more overseas contracts.

Non-power business performance is outstanding, helping to expand the ¡§mega building¡¨ market landscape

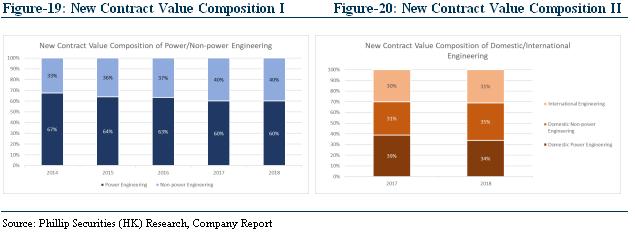

In 2018, the newly signed contracts of non-power engineering business amounted to RMB183,613 billion, a YoY increase of 3.55%, accounting for 39.75% of the newly signed contracts for the whole year. Among them, the domestic non-power engineering business realized a new contract value of RMB159.928 billion, accounting for 35% of the new contract value for the whole year, and accounting for 50% of the domestic new contract value for the first time, representing an increase of 15.52% YoY. Among which, the newly signed contracts for domestic businesses of new business models valued RMB106.417 billion, accounting for 23.04% of the company¡¦'s annual newly signed contracts in total.

In 2018, the company highlights the development of a grand construction market landscape and stays close to the requirements for developing non-power engineering businesses to optimize and adjust organizational structures, and bring the synergy of the CGGC Group, CPE, the construction investment companies and the platform company into play. The company keeps augmenting resource input in non-power engineering businesses and seizes the market opportunities brought about by the Xiong¡¦`an New Area, the military-civilian integration, the Grand Protection of Yangtze River, the Guangdong-Hong Kong-Macao Greater Bay Area, the Hainan Free Trade Zone, the ¡§One Belt One Road¡¨ construction, and international capacity cooperation to further empower the company¡¦'s construction and contracting businesses. In 2018, the newly signed contract value of the non-power construction and contracting business was RMB182.703 billion, a YoY increase of 3.45%, accounting for 39.55% of the annual new contract value in total, becoming a key growing point of the company.

The company strives to open up domestic non-power sectors including the transport, the municipal administration, the eco-environmental protection, mining, shantytowns transformation, park development, housing construction and other domestic non-power sectors. In 2018, the domestic non-power construction and contracting business achieved a new contract value of RMB159.028 billion, a YoY increase of 15.46%. The newly signed contract value of the PPP project exceeded RMB100 billion for two consecutive years, accounting for 23.04% of the annual new contract value in 2018. We believe that the rapid growth of non-power engineering business can not only increase the gross profit margin, but also accelerate the transformation of the domestic business of the company and build a ¡§mega building¡¨ market landscape.

Financial Forecast

Revenue and Profits Forecast

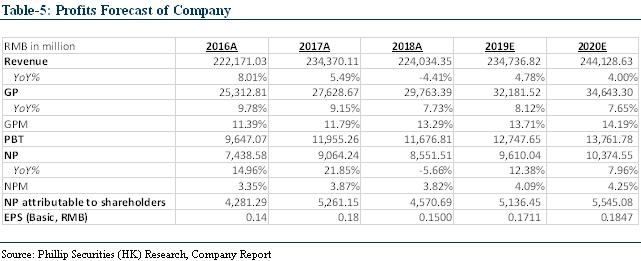

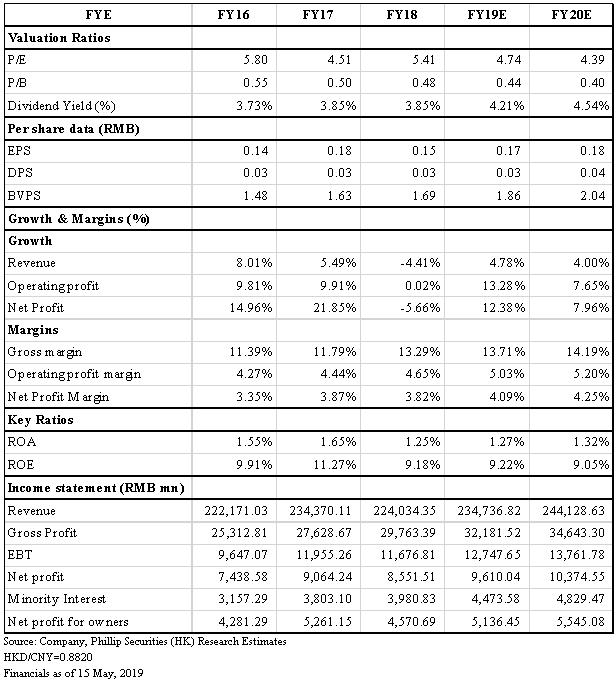

Revenue in FY19/FY20 are expected to be RMB 234.737 billion/RMB 244.129 billion, representing YoY growth of 4.78%/4.00%. Net profits to owners are expected to be RMB 5.136 billion/RMB 5.545 billion in FY19/FY20, representing increase of 12.38%/7.96% on a YoY basis. Due to the effective cost control, we think the GPM and NPM would remain stable in FY19/FY20. As a leading enterprise in China and global power construction markets, company¡¦'s outstanding contract value to income coverage ratio is 4.8x, showing a sufficient reserve of contracts. We are optimistic about the future of the company given the sufficient contracts backlog, rapid development of non-power and international businesses.

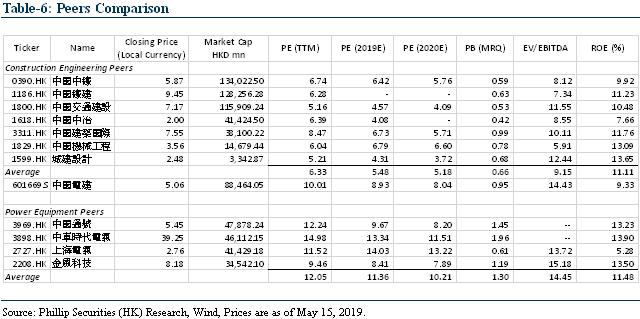

Valuation

According to Wind data, the average PE (TTM) of Hong Kong market Construction and Engineering sector is 6.33x, PB (MRQ) is 0.66x; PE (TTM) of Hong Kong market Power Equipment sector is 12.05x, PB (MRQ) is 1.30x as of May 15, 2019. Based on our estimates, given the sufficient aggregate contract value, recovery of international business, rapid development of non-power engineering business as well as the influence of trade war, we initiate coverage on China Energy Engineering Corp. with 6.96x/6.44x FY19/FY20 PER and 0.64x/0.58x FY19/FY20 PBR, corresponding to TP HK$ 1.19 with a 29.3% potential upside compared with current price HK$ 0.92 as of June 11, 2019, and recommend ¡§BUY¡¨ investment rating. (HKD/CNY=0.8820).

Risk

1. International business fails expectations

2. China infrastructure investment fails expectations

3. China electricity investment fails expectations

Financials

Click Here for PDF format...