Investment Summary

Due to the change of industry policy, Yutong saw net profit of 2017 decreased by above 20% yoy. The shrink NEV subsidy, the lengthened payback period and the price promotion undermined the company's profitability. While the company enlarged it market share and the bad debts will be partially reversed, which is helpful to the bottom-up of the FY2018 result.

Result in 2017 Fell by More Than 20%

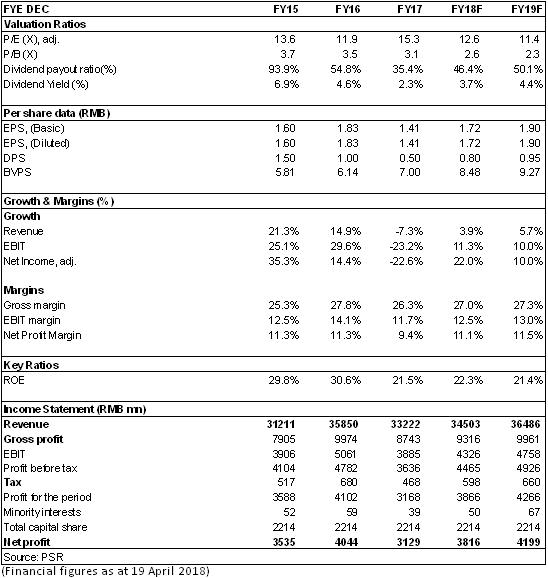

Yutong Bus reported revenue of RMB 33.222 billion in 2017, down by 7.33% year on year; net profit attributable to parent company was RMB 3.129 billion, down by 22.62% year on year; earnings per share was RMB 1.41, with a dividend of RMB 0.5 per share. The main reason for the lower-than-expected result was that the bus industry was undermined by the subsidy policy for new energy vehicles. We lowered our target price but maintain the accumulate rating.

Over Depression of the Industry, Market Share Increased Significantly

The Ministry of Finance issued a notice on December 30, 2016, in which the national subsidies for pure electric buses was reduced by RMB 200,000 per vehicle and local subsidy shall not be higher than half of the national subsidy, and there added one application requirement of 30,000 kilometers of operating mileage. Affected by changes in industry policies, the national annual sales of buses of 7 meters or more was 167,588 vehicles, down by 14%. The products of Yutong Bus mainly cover the large- and medium-sized bus markets, and sales were also dragged down, but it was better than the industry average, only falling by 5.24% year on year to 67,268 vehicles. However, the market share increased, occupying 28.8% in the large bus market with an increase of 2.9 ppts; a medium-sized bus market share was 44.2%, increasing by 4.9 ppts; and the market share of large- and medium-sized new energy bus was 28.3%, increasing by 3.4 ppts.

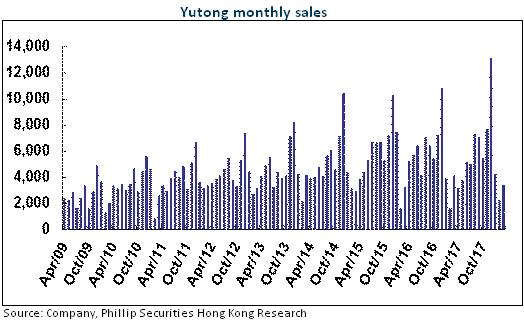

Sales up and Profit down in the Fourth Quarter

Since 2013, due to the special nature of the new energy vehicle industry, the fourth quarter was apparently the peak season, so that net profit produced in the fourth quarter of Yutong Bus took up half of the whole year's result on average. In 2017, due to sluggish sales in the first three quarters, the company carried out more aggressive promotional activities in the last quarter in order to complete sales targets set up at the beginning of the year, which resulted in reduced profitability. On the basis of an increase of 12% in sales in the fourth quarter, the net profit fell by 31% year on year. Gross margin for the year was 26.32%, down by 1.5 ppts year on year.

Three Fees Rose

The 30,000-kilometre application condition has lengthened the payback period of state-subsidy funds repayment of receivables of the company, which has had a significant impact on the company's funds and accounts receivable. The company's interest expenses in 2017 were RMB 333 million, increasing enormously by 279% compared to that of RMB 88 million in the same period of the previous year, consequently the financial expenses increased by 79% to RMB 490 million; while the provision for bad debts of accounts receivable amounted to RMB 507 million, increasing by 40.44% compared with that of RMB 361 million in the same period of the previous year. The final net profit margin turned out to be 9.54%, deceasing by 1.9 ppts year on year. However, with the application condition reduced to 20,000 kilometers in 2018, the payback period of state-subsidy funds repayment of the company is expected to be shortened, bad debts will be partially reversed and financial pressure will be eased. In a word, the result in 2018 is expected to pick up.

Under New Subsidy Policy, It's Time to Reshuffle and Expand the Industry

In 2018, the further adjustment to the national new energy passenger vehicle subsidy policy will push up the entry of the industry, accelerate the survival of the fittest, and the industry structure will continue to be optimized, which will benefit industry leaders such as Yutong Bus to continue to expand market share.

In terms of technology, the company's core technologies such as energy saving are in a leading position. The core technologies including finished vehicle safety and control technology, finished vehicle lightweight technology, and vehicle networking service platform have made breakthroughs, greatly improving the product competitiveness. And compared with 2016, energy consumption of finished vehicle is reduced by more than 5% on average. The overseas projects of high-end products proceeded smoothly. In 2017, the company's new energy bus exports increased by 18% year on year to 8,142. Compared with foreign counterparts, the company's new energy products have significant technological maturity and scale advantages, and have already passed local certification. With brand and technology advantages, the future is well expected.

Investment Thesis

In general, the product unit price in 2018 may continue to be under pressure; however, with the further optimization of the industry structure and the test of time, companies with strong technical strength, high product quality, and comprehensive cost-effectiveness will take a leading position in the new energy bus market in the future. In addition, overseas markets are also expected to be beneficial to the growth of the company's result.

We forecast that the company's EPS in 2018/2019 will be RMB1.72 and RMB1.9, our target price is set unchanged at RMB25. It is equivalent to a prospective 2018/2019 PE of 14.5x and 13.2x respectively. We give ¡§Accumulate¡¨ rating. (Closing price as at 19 April 2018)

Financials

Click Here for PDF format...