|

|

|

*Advertisement* |

|

|

|

|

|

25 May, 2017 (Thursday) |

|

|

DYNAGREEN ENV(1330)

Analysis¡G

In 2016, Dynagreen witnessed a year-on-year increase in environmental revenue of 49%, amounting to RMB1.874 billion, which was mainly benefited from the growth of 63.9% in construction revenues and 31.3% in operating revenue. Net profit recorded a year-on-year increase of 57%, reaching RMB0.356 billion, which outperformed market expectation. Specially, from the perspective of income structure, operating revenue accounted for more gradually in the past three years, reaching 31.6% in 2015 but dropped to 27.8% in 2016. This was mainly resulted from the increasing proportion of construction revenue caused by more construction projects in the year. In respect of earnings quality, overall gross profit margin slightly fell by 2% to 31%, which was mainly attributable to the increase in the construction business with lower gross profit margin. The net profit ratio increased by 1% to 19.01%, which was partly benefited from the decrease of period expense ratio and increase in refund of value-added tax during this period. ROE kept increasing for the third consecutive year and reached the peak at 13.0% in 2016, which reflected the improvement of operations in the company, leading to the rising of earnings quality. 1)In respect of valuation, the present price is equivalent to a 12x PE and a 1.52x PB. This value is at a lower level among the same trades in Hong Kong stocks. 2) The waste incineration industry still has wide development space. Also, the company has abundant projects at hand and keeps improving the operating level, which can ensure the steady increase in the next two years. 3) A-share IPO will motivate the company to adopt valuation and restore market. We`ll keep an eye on the progress of IPO. We estimate, from 2017 to 2018 the net profit attributable to the patent company will reach 4.4/5.47, respectively, equivalent to an EPS of 0.42/0.52, respectively, and a PE of 9.4/7.6, respectively. We give a target price of HKD5.64 and the buy rating.

Strategy¡G

Buy-in Price: $4.13, Target Price: $5.64, Cut Loss Price: $3.40

|

| |

|

SAIC Motor (600104.CH) - Brief review of the financial result

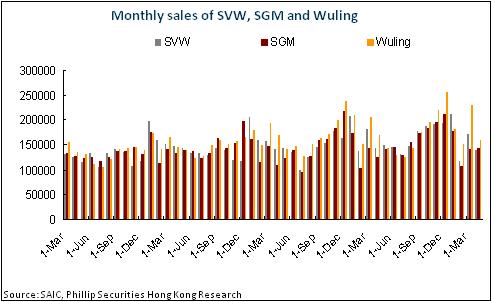

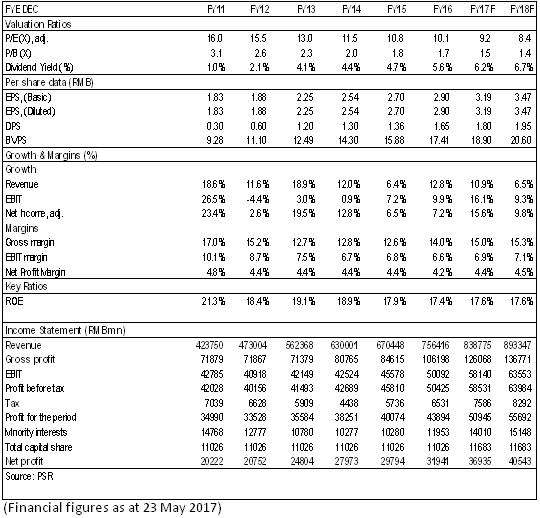

Dividend Rate Is Higher Than ExpectationIn 2016, Shanghai Automotive Industry Corporation recorded a revenue of RMB756.4 billion, representing a year-on-year increase of 12.8%. Net profit attributable to shareholders stood at RMB32 billion, with a year-on-year increase of 7.43%. Profits are in line with our expectation. Earnings per share was RMB2.9. The figure was RMB2.7 in last year. The dividend per share was RMB1.65 in cash, with a payout ratio of 56.8%, 9 points higher than our previous expectation. In Q1 2017, the company reported a revenue of RMB196.28 billion, a year-on-year increase of 6%. Net profit attributable to the shareholders stood at RMB8.26 billion, a year-on-year increase of 4.1%. Net profit excluding non-recurring profit and loss was RMB8.17 billion, a year-on-year increase of 11%. Earnings per share was RMB0.71, a little lower than RMB0.72 in the same period last year. The increase of share issuance caused dilution. JVs Reported Mix Results in Their PerformanceIn 2016, Shanghai Automotive Industry Corporation sold 6,489,000 vehicles, a year-on-year increase of 9.95%. The target of 6.17 million vehicles has been fulfilled, with a completion rate of 105%. The sales volume of SAIC Volkswagen increased by 10.5% year on year to 2,002,000 vehicles; that of SAIC GM by 7.7% year on year to 1,887,000; that of SGM-Wuling increased by 4.4% year on year to 2,130,000. In terms of financial data, the revenue of SAIC Volkswagen rose by 4.6% to RMB228.55 billion, and the net profit of SAIC Volkswagen was up by 3.1% to RMB25.68 billion. The revenue of SAIC GM increased by 14% to RMB202.9 billion, and the net profit of SAIC GM went up by 2.3% to RMB16.95 billion, which is quite stable. The net profit of SGM-Wuling increased by 3.6% YoY to RMB5.198 billion and that of Huayu soared by 27% YoY to RMB6.076 billion. In Q1 2017, the whole sales volume of SAIC was 1,656,000 vehicles, a year-on-year increase of 3%. Due to the temporary shortage of parts, the sales volume of SAIC Volkswagen dropped by 4.7% year on year. However, high-priced models, such as Teramont (approx. RMB400,000), Tiguan L (approx. RMB300,000) and Kodiak (approx. RMB200,000) are expected to sell well. It is estimated that the increase speed of profits will grow gradually. The sales volume of SAIC GM increased by 2.3% while new models such as Chevrolet Equinox and new version GL8 met with sufficient orders. The quarterly sales of Cadillac rocketed by about 80%, which is expected to sustain steady growth rate and profit improvement. The sales volume of SGM-Wuling reached 563,000 vehicles, a year-on-year decrease of 0.7%. The increase of Baojun SUV will be offset by the drop of mini MPV and minivan. We expect that the whole sales will be basically flat this year.

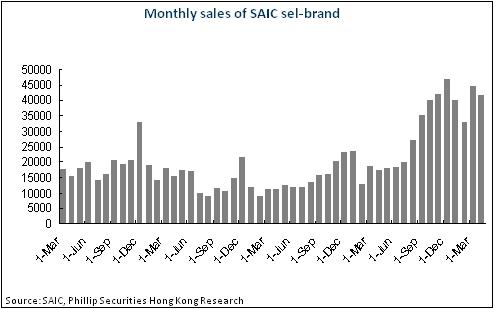

Self-Owned Brands Maintained Robust Growth Momentum.The performance of self-owned brands of SAIC is getting better, with explosive sales growth. In 2016, the sales volume increased by 89% to 322,000 vehicles. In the first quarter of 2017, the sales volume jumped by 112% to 118,000 vehicles. The strong sales momentum mainly comes from Roewe RX5, whose monthly sales exceeded 15,000. New models such as Roewe i6 and MG ZS is meeting with stable sales now, which are expected to have a share in the updated car market in the future. Along with gradual match of manufacturing capacity, the self-owned brands of SAIC are very likely to achieve a breakthrough in the sales volume, with an expected year-on-year increase of more than 90%.

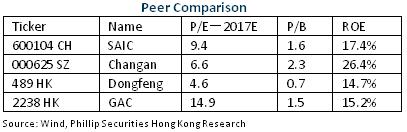

Investment ThesisWe hold that driven by new product cycle and improving product structure, the company's better-than-expected growth is worth looking forward to. A relatively high cash dividend rate (about 55%) is expected to continue with its abundant cash flow. We adjust the profit forecast, giving the target price of RMB32.67, equivalent to 10.2/9.4x estimated P/E ratios in 2017/2018. The "Accumulate" rating is given. (Closing price as at 23 May 2017)

Financials

Click Here for PDF format...

| Recommendation on 25-5-2017 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 29.230 | | Suggested purchase price | N/A | | Target Price | $ 32.670 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | Goldpac Group | 3315 | 27/03/2017 | Buy | 3 | 2.4 | | O-Net Technologies | 877 | 27/09/2016 | No Rating | | 4.02 | | | SAIC Motor | 600104 | 25/05/2017 | Accumulate | 32.67 | 0.000 | | China auto sector Quarterly report | | 18/05/2017 | Market Perform | | | | | | Wisdom Sports Group | 1661 | 11/07/2016 | Buy | 3.3 | 2.18 | | NetDragon | 777 | 16/06/2016 | Buy | 28.4 | 22.9 | | | Tonghua Dongbao | 600867 | 24/05/2017 | BUY | 27.08 | 21.34 | | China Resources Sanjiu | 000999.CH | 17/05/2017 | Accumulate | 35.38 | 29.71 | | | TK Group | 2283 | 20/03/2017 | Accumulate | 2.8 | 2.38 | | TK Group | 2283 | 10/01/2017 | Buy | 2.8 | 2.18 | | | Luye Pharma | 2186 | 22/03/2017 | Buy | 6.3 | 4.95 | | Harmonicare | 1509 | 17/01/2017 | Buy | 5.53 | 4.45 | | | HN RENEWABLES | 958 | 27/02/2017 | Buy | 3.5 | 2.72 | | CONCORD NE | 182 | 24/10/2016 | Buy | 0.6 | 0.39 | | | L`OCCITANE | 973 | 22/05/2017 | Accumulate | 17 | 15.3 | | L`OCCITANE | 973 | 19/05/2017 | Accumulate | 17 | 15.3 | | | JNBY | 3306 | 13/04/2017 | Accumulate | 6.6 | 5.95 | | CECEP COSTIN New Materials Group | 2228 | 18/10/2013 | Buy | 5.6 | 4.23 | | | Chinasoft International Ltd | 354 | 10/04/2017 | Buy | 5.8 | 4.61 | | Chinasoft International | 354 | 26/10/2016 | Buy | 4.86 | 3.72 | | | KWG Property | 1813 | 23/05/2017 | Accumulate | 6.55 | 5.6 | | Hongkong & Shanghai Hotels | 45 | 10/05/2017 | Accumulate | 10.48 | 9.14 | | | ND Paper | 2689 | 05/04/2017 | Accumulate | 9.5 | 8.35 | | ND Paper | 2689 | 09/03/2017 | Accumulate | 11.65 | 10.02 | | | DONGJIANG ENV | 895 | 15/05/2017 | Buy | 14.8 | 12.16 | | China Tianying | 000035.SZ | 09/05/2017 | Buy | 9.3 | 7.05 | | | Great Eagle | 41 | 16/05/2017 | Neutral | 39.3 | 38.5 | | K. Wah International | 173 | 27/04/2017 | Accumulate | 5.8 | 5.06 | | | IGG | 8002 | 21/11/2014 | Accumulate | 3.95 | 3.44 | | HC INTERNATIONAL | 2280 | 06/11/2014 | Buy | 14.92 | 8.8 | | | Jinjiang Hotels | 2006 | 08/07/2016 | Accumulate | 2.98 | 2.49 | | CUTC | 600358 | 08/03/2016 | N/A | | 10.41 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2017 Phillip Securities (HK) Ltd. All Rights Reserved.

|