Investment Summary

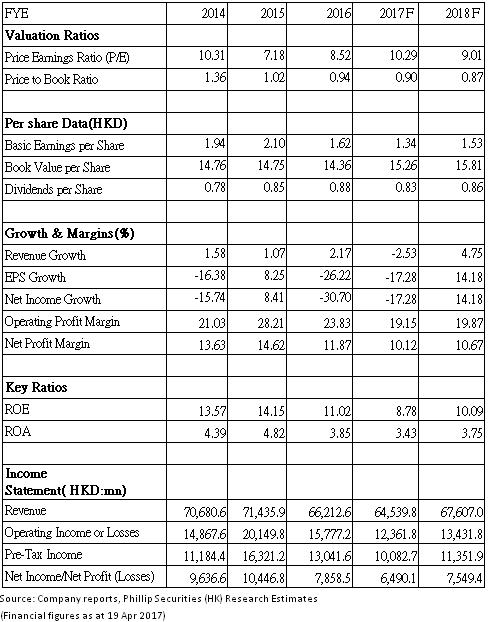

-The Net profit decreased 23.1%, mainly due to the coal power tariff cut and increased fuel costs. However, the dividend per share increased 3%, thanks to its generous dividend payout.

-The valuation is attractive, because both PE and PB ratio were significantly lower than the 10 years average. The FY2016 ROE was slightly lower than its 10 years average but still higher than its peers.

-China's power consumption accelerates in Q1 2017. China's coal price has dropped slightly recently, if the coal price continue to drop, will improve the group's earning power.

FY2016 result review

China Resources Power Holdings Company Limited mainly engaged in in the development, construction and operation of power plants, including large-scale efficient coal-fired generation units and various clean and renewable energy projects as well as development, construction and operation of coal mines.

Acorrding to the FY2016 result, the attributable operational generation capacity of the Group's coal-fired power plants amounted to 31,066MW, accounting for 85.9% of the Group's total attributable operational generation capacity, representing a decrease of 0.8% YoY. Wind, gas-fired, hydro and photovoltaic capacity amounted to 4,632MW, 77MW, 280MW and 130MW, respectively, and together accounting for 14.1% of the Group's total attributable operational generation capacity, representing an increase of 0.8% YoY.

The total gross generation volume of the Group's consolidated operating power plants amounted to 160,571,282MWh in 2016, representing an increase of 6.1%YoY.Thermal power generation increased 2.4%YoY, Wind power generation increased of 30.1% YoY. However, the arithmetic average on-grid tariff for the subsidiary coal-fired power plants decreased by RMB32.4/MWh, or approximately 7.7%, and the average unit fuel cost for the Group's consolidated operating coal-fired power plants in 2016 was RMB156.18/MWh, representing an increase of 6.8% YoY. Average standard coal cost for the Group's consolidated operating coal-fired power plants in 2016 was RMB509.86/tonne, representing an increase of 7.8% YoY. Since the coal power tariff cut and increased fuel costs, the group's profitability decreased significantly. As a result, for 2016, net profit amounted to approximately HK$7,708 million, representing a decrease of 23.1% YoY. Basic earnings per share for 2016 is HK$1.62, representing a decrease of 22.9% YoY. However, the average full-load equivalent utilisation hours of the subsidiary coal-fired power plants under the Group which were operational for the full year of 2016 reached 4,922 hours, representing an increase of 0.3% compared to 4,906 hours for the full year of 2015, and exceeding the national average utilisation hours for thermal power plants of 4,165 hours by 757 hours. Thanks to the generous dividend payout, the recommend final dividend was HK$0.75 per share for 2016. Including the interim dividend of HK$0.125 per share paid in October 2016, total dividend paid and proposed for 2016 is HK$0.875 per share, representing an increase of 23.1% YoY.

Although the net profit decreased by 23.1% YoY, the stock is only trading at 8.52x PE and 0.94x PB, and providing a fat dividend yield of 6.34%, which indicated that the valuation is attractive. The PE and PB ratio were significantly lower than the 10 years average, but the ROE was only slightly lower than its 10 years average and still higher than its peers.

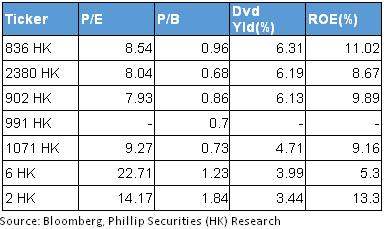

Peer Comparison

The table in above shows the simple peer comparison of the group.

In term of PE and PB, the group is less expensive than its international peers such as Power Asset Holdings (6 HK) and CLP Holdings (2HK).

In term of PB, the valuation is slightly more expensive than its Chinese peers such as Huaneng Power (902 HK), China Power (2380 HK),and Huadian Power (1071 HK). However, the group has a better earning power since its ROE was obviously higher than its peers.

In term of PE, the group is slightly more expensive than Huaneng Power, and China Power, but less expensive than Huadian Power (1071 HK).

The Valuation is attractive

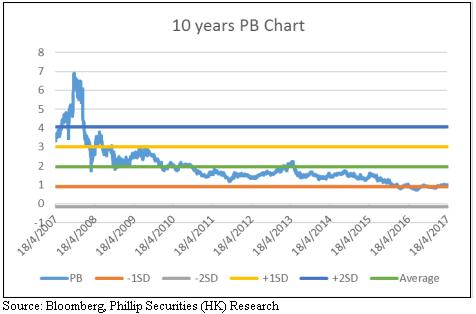

The chart below shows 10 years of PB ratio of the stock, the statistic started on 18/4/2007, with 2 standard deviations.

From the chart above, we can see that the PB valuation is significantly lower than the 10 years average. The average 10 years PB ratio is approximately 1.95x, which is around 103% higher than its current PB ratio. One standard deviation below is 0.90x, which indicated that the stock trades significantly below the 10 years average but slightly above 1 standard deviation. From the 10 years PB chart, we can see that the valuation of the stock is extremely fluctuate, but since it is trading at significant below the 10 years average, the downside risk possibly limited. In conclusion, in term of the PB ratio, the valuation is attractive.

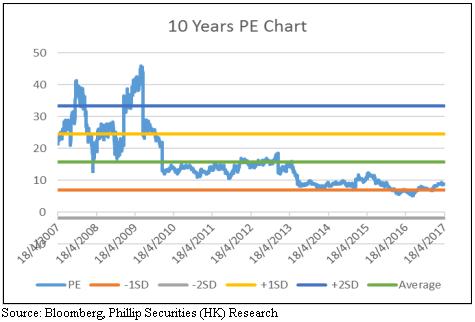

From the chart above, we can see that the PE valuation is significantly lower than the 10 years average. The average 10 years PE ratio is approximately 15.74x, one standard deviation below is 6.97x, which indicated that the stock trades significantly below the 10 years average but slightly above 1 standard deviation. From the 10 years PE chart, we can see that the PE valuation of the stock is also extremely fluctuate, but since it is trading at significant below the 10 years average, in the PE point of view, the downside risk possibly limited. In conclusion, in term of the EB ratio, the valuation is also attractive.

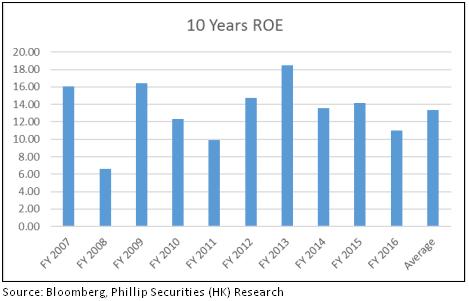

The chart in below shows the 10 years ROEs of the firm.

According to the bar chart in above, the ROE of 2016 was 11.02%, which is lower than the 10 years average ROE of 13.33%, However, the stock trades at only around 1x PB ratio currently, which is also lower than the PB in the 2008, but the ROE is significantly better than it was in the 2008 financial crisis period. In addition, ROE figures in last years were significantly more stable than its peers, during the 2008, the firm still generated operating profit, which peers suffered net loss in 2008.

Moreover, we used a simple Discounted Dividend Model for evaluating the intrinsic value. The annual market return of HSI that we use for the calculation is 7.16%, datas collected from 31th Dec 1995 to 31th DEC 2016. We used the 10 years China government bond yield of 3.38% as the risk free rate, and the historical Beta of the stock is 0.796. From that, we calculated that the required return of the stock is 6.39%. Our prudently forecasted dividend per share for next year is 0.83 HKD per share. Basic on the 10 years average ROE figure, and the dividend payout ratio will stays the same as 50%, we prudently estimated the ROE will be weaken by 50%, that the dividend growth rate is 3.33% As a result, we calculated the intrinsic value of HKD 27.12 per share. For margin of errors, we increase the required return of the stock by 2%, the calculated intrinsic value is still HKD 16.40 per share. Therefore, we believe that the stock is undervalued, and the downside risk of the stock is possibly limited.

China's power consumption accelerates in Q1

According to the National Development and Reform Commission, Power consumption rose 6.9% YoY in the first three quarters of this year, 3.7% higher than the same period last year. In 2016, the power industry in China experienced a complicated and changing market environment. In 2016, the national total electricity consumption rose by 5.0% YoY. Although the growth rate increased significantly as compared with 2015, the national power generation installed capacity as at the end of 2016 recorded a year-on-year increase of 8.2%, which was even higher than the growth rate of national total electricity consumption, indicating an oversupply of national power supply. The higher power consumption in Q1, should ease the overcapacity issue in China.

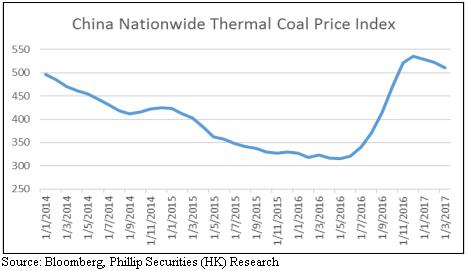

China Nationwide Thermal Coal Price Index dropped slightly

Since the China government has been implemented a successful coal supply-side structural reform, including the strictly production limitation and reduction policy in major coal producing areas, as well as intensified the inspection on illegal coal mines and closure and suspension of mines. In 2016, the coal price increased roughly more than 60%, according to the data from Bloomberg.

However, the China Nationwide Thermal Coal Price Index dropped slightly to 511.29 per tonne in Mar 2017. Moreover, According to a report released by Cqcoal on 19/04/2017, the Bohai-Rim Steam-Coal Price Index (BSPI), a leading indicator for Chinese coal prices, decreased for 4 consecutive weeks to 599RMB per tonne.

Valuation

Taking all the points mentioned above into consideration, China Resources Power's target price is therefore $16.40, with Accumulate rating assigned, represents 1.07x FY17 expected PB and 1.03x FY18 expected PB. (Closing price as at 19 APR 2017)

Risks

-Risks relating to the power demand in China, the overall power demand could keep declining if the economic growth slows down.

-Risks relating to coal market, the fluctuation on the coal price will bring certain degree of risks to the fuel cost control.

-Risks relating to electricity tariff, it could cause uncertainty on the firm's revenue.

-Risks relating to environmental protection policies, the national standards for energy saving environmental protection could pushed higher and the environmental protection restrictions for energy development is possibly more tightened.

Financials

Click Here for PDF format...