Property Development Portfolio Spans across China

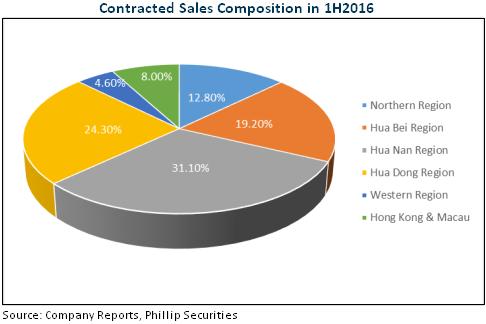

China Overseas Land & Investment is a nationwide property developer in China. In general, China Overseas engages evenly in the developed regions of China, with a main focus on the development in cities in Hua Nan Region and Hua Dong Region, such as Shenzhen, Guangzhou and Shanghai. In 1H2016, the contracted sales in these two regions account for 55.4% of the total sales in terms of revenue. In particular, China Overseas can be distinguished from the typical mainland Chinese property developer by the fact that they have a long strategic presence of engaging in the Hong Kong property industry. In 1H2016, Hong Kong contributes to about 8% of the contracted sales in terms of revenue.

In the Kai Tak Development programme, China Overseas has launched its first project in the programme in September 2016. The first phase of One Kai Tak was launched in September and the flats available were sold quickly. China Overseas acquired the land at a price of HKD5,427 and HKD4,913 per square foot in 2013. With the recent land acquisition by other companies in Kai Tak being priced at HKD13,500 per square foot, China Overseas is expected to be benefit from that expensive land acquisition and is expected to have a larger pricing power in the latter phases of One Kai Tak project, which in Phase 1 the average price per square foot is about HKD14,900, after including all discount. The expected completion date of One Kai Tak is in the third quarter of 2017 and therefore the revenue associated with One Kai Tak is expected to be recognised in 2017 or later.

Huge Project and Land Reserve

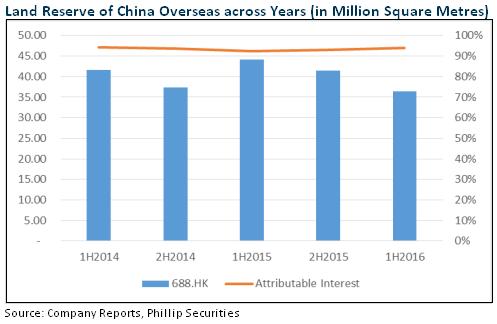

During 1H2016, 48 properties, with a total GFA of 7,130,000 square metres were completed. There were 24 major construction projects, with a total GFA of 5,802,000 square metres, of which 2,326,000 square metres, or 40.1% of the major property's GFA contributed by Hua Nan Region and Hua Dong Region. China Overseas has a huge land reserve and regularly has over 35 million square metres of GFA across years. Up to November 2016, China Overseas has acquired land in Jinan, Hong Kong, Nanchang and Changchun, providing an additional GFA of 7.25 million square metres to the land reserve.

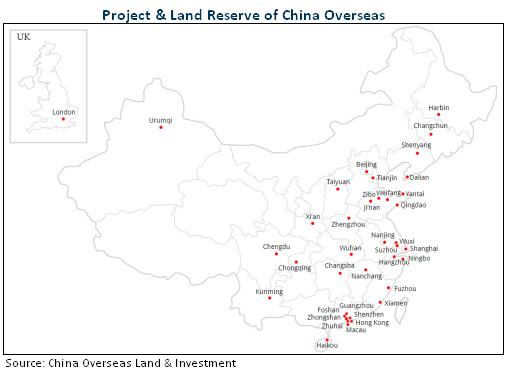

The majority of the land and projects of China Overseas are located in the Eastern part of China.

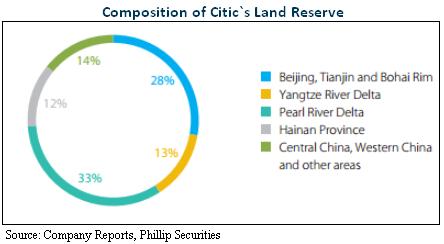

China Overseas has also completed the acquisition of Citic Property in September 2016 and Citic Property could inject 30 million square metres of land resources into China Overseas. From this acquisition, we expect China Overseas to benefit from Citic Property's land reserve, which is mainly located in the developed region such as Pearl Delta Region and Beijing, Tianjin Region. According to the 2015 annual report of Citic, the property segment of Citic is composed of the following land:

Besides, China Overseas has an associate company called China Overseas Grand Oceans, which concentrates on the development projects in the Tier 3 Cities. Recently, Grand Oceans has acquired the Tier 3 Cities assets of China Overseas at a consideration of CNY3,516Mn. We expect China Overseas to continue to focus on Tier 1 and Tier 2 Cities and enjoy the higher profit margin and demand in these cities.

Financial Overview

Contracted sales of China Overseas has been strong for years and has risen from HKD112Bn in 2012 to HKD207Bn in 2016 Jan-Nov, a rise of 85% during the period. Recognised sales has risen significantly too, from HKD64.6Bn in 2012 to HKD140.1Bn in 2015.

China Overseas has strong sales as well as profitability. Of the property developers of the same size and the same strategy, China Overseas has greater gross profit margin than the others have. This is probably due to China Overseas being concentrated on Tier 1 and Tier 2 City development and the Tier 3 City development, which generally has a lower profit margin, is left to its associate company, Grant Oceans, which only had a gross profit margin of 18.1% in 1H2016 and 15.6% in 2015.

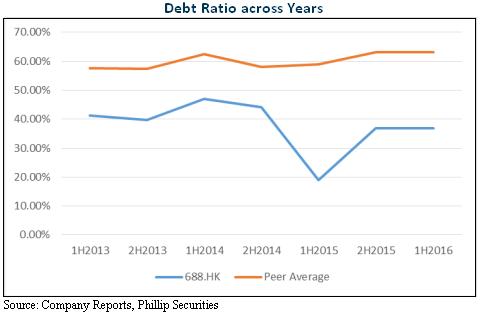

Apart from profitability, China Overseas has better gearing ratio than its peers, with Total Debt to Total Capital ratio currently maintaining at around 36%. In comparison with the other nationwide property developers, which have a much higher debt ratio, with some having up to 80%, China Overseas clearly is at a better and much healthier position than its peers are.

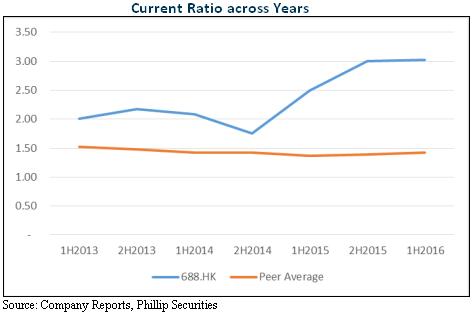

China Overseas also has much better liquidity than its peers, mainly caused by the realization of inventory of properties.

Valuation

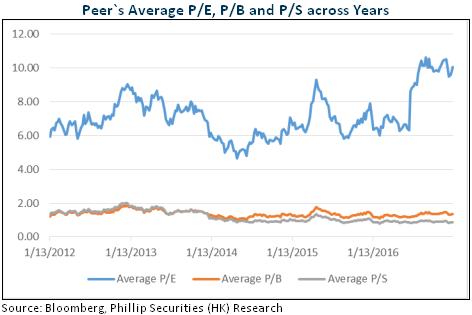

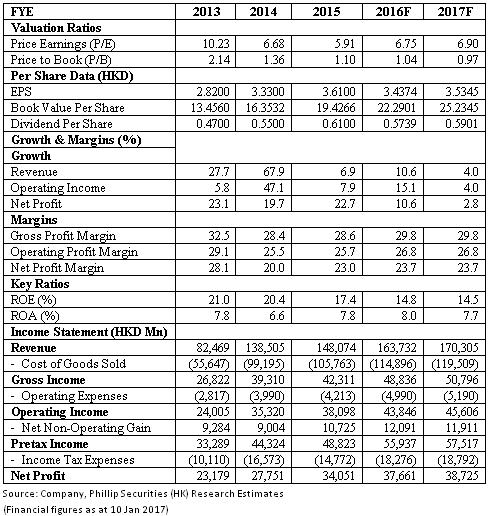

The peer average P/E, P/B and P/S are 7.17x, 1.38x and 1.20x respectively. China Overseas's target price is therefore HKD24.40, with Accumulate rating assigned. (Closing price as at 10 Jan 2017)

Risk

Tightening policy in the property market

Delay in opening of new hotels

Financials

Click Here for PDF format...