|

|

|

*Advertisement* |

|

|

|

|

|

24 Oct, 2016 (Monday) |

CHINARES CEMENT(1313)

Analysis¡G

China Resources Cement Holdings (1313) has released the unaudited financial results for the nine months ended 30 September 2016. Although its turnover and profit attributable to shareholders declined 11.5% and 34.6% respectively as compared to the same period last year, the consolidated gross profit margin improved from 24.4% in the same period last year to 25.3%. Profit attributable to shareholders for the third quarter reached HK$580 million (it recorded net loss of 248 million in the same period last year), substantially higher than the profit of HK$6.6 million and HK$250 million in the first and second quarter this year. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $3.00, Target Price: $3.35, Cut Loss Price: $2.85

|

|

ZTE(763)

Analysis¡G

The R&D expense ratio of ZTE reached up to nearly 15% in 1H16, and the investment was distributed mainly to products like 5G products, high-end routers, LTE, SDN, core chips, etc. and will serve as technical support for mid- and long-term development. We hold estimation that the growth will keep high within the next two years. Firstly, China Unicom and China Telecom have entered a period of rapid development in building the 4G network, which will sustain the steady development of domestic communications device market. Meanwhile, with rising 4G infrastructure in emerging markets, the Company, equipped with technological and branding advantages, will gain benefits in the mid and long term. Secondly, the requirements of cloud computing, big data, the Internet of Things and so on for data flow is increasing by geometric progression and the construction of broadband and transmission networks is fastening, which will trigger demands for optical network products in an all-round manner.

Strategy¡G

Buy-in Price: $10.76, Target Price: $12.50, Cut Loss Price: $10.20

|

| |

|

CONCORD NE (182. HK) - Expansion of Power Generation Business to the South China, Substantial Profit Contribution

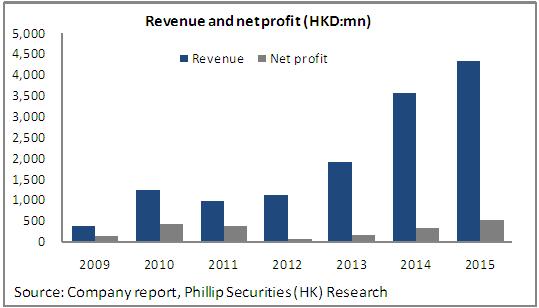

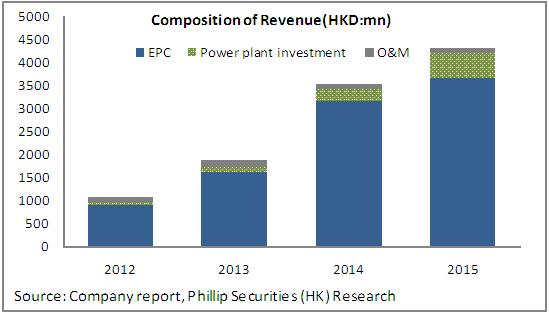

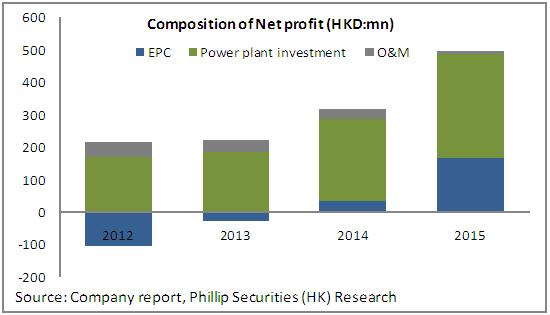

EPC Business Contributed to 50% Drop in Total RevenuesIn the first half of 2016, the revenues of Concord New Energy dropped by 51.5% year-on-year to RMB1.052 billion, whereas the profit attributable to shareholders increased by 10.1% to HK$279 million. During the period, the company adjusted its business models, significantly reduced the size of EPC business and increased the proportion of BT business. As a result, revenue from EPC business plummeted by 68.7% year-on-year to RMB584 million, representing 55.5% of the total revenue from last year's 85.8%. Although the plunge in revenue and profit of the EPC segment contributed to poor overall performance, the performance of wind power segment was impressive and the significant increase in profitability drove up the overall profit. Meanwhile, the company also took a wide range of measures to control costs, that is, lowering equipment costs while improving the efficiency of equipment operation. Therefore, net profit margin saw a substantial increase of nearly 15 percentage points to 26.5%.

Expansion of Power Generation Business to South China, Substantial Increase in Profit ContributionInstalled capacity and power generation of the company grew steadily, resulting to significant increase in proceeds from power generation. The revenue derived from power generation business soared by 71.1% over the previous year to RMB428 million, and the net profit surged by 80.8% over last year to RMB207 million, so power generation business was the core profit source of the company. During the period, new grid-connected attributable installed capacity amounted to 122MW, representing a year-on-year increase of 106.8%. The newly installed power capacity throughout the year is expected to be 300-400MW. The attributable installed capacity of continued projects and new construction projects stood at 788MW, up by 40% year-on-year. Besides, attributable power generation reached 1,096.85GWh, a year-on-year increase of 38.4%. By the end of the period, the company owned 52 grid-connected power plants with attributable installed capacity of 1,401MW, around 2/3 of which was situated in areas without curtailment. The attributable installed capacity is projected to reach 2,500MW by 2018. Presently, the company primarily wholly owns or controls new power generation projects in the central and south areas without curtailment, and gradually reduces the assets in areas with curtailment by sales and replacement. With the improvements in overall asset quality, the operating income from the power generation segment will witness a continued surge. Enhanced Financing Capacity and Independent Power Generation CapacityThrough exploring a vast variety of financing channels, the company's financing capacity was significantly enhanced. To be specific, in the first half of the year, it issued the first domestic green bond worth RMB500 million and short-term commercial paper worth RMB600 million, and signed long-term loans worth RMB1.8 billion. The financing fund will be used to independently develop new power plants. We expect that the company will have sufficient capital guarantee. Also, with rich reserves of resources, its power plant development business will experience a rapid development and the attributable installed capacity of independent power generation will see a substantial increase. Valuation and RatingAs a number of ultra-high voltage (UHV) transmission lines will be put into operation in 2017, the grid curtailment in the industry will be gradually improved, and the power generation utilization hours are projected to gradually increase due to the implementation of government-subsidized purchase policies. Under the continuous optimization and adjustment of asset structure, the company's revenue from and profit contribution of power generation business are constantly increasing, leading to further growth in overall profits. Furthermore, since the end of last year the company has repurchased a total of 212 million shares and the continuous share repurchase also helps to boost investor confidence. But the policy of cutting on-grid price imposes pressure on the company's valuation. Given the PV projects held by the company are basically located in the areas without curtailment, we believe that the company's net profit in 2016 and 2017 will be basically unaffected. Therefore, we give the company the target price of HK$0.60 and the "Buying" rating. (Closing price as at 19 October 2016)

Risk WarningsThe implementation of policy falls short of expectations; Operating of power plants under construction fails to meet expectations; Changes in curtailment policy;

Financials

Click Here for PDF format...

| Recommendation on 24-10-2016 | | Recommendation | Buy | | Price on Recommendation Date | $ 0.390 | | Suggested purchase price | N/A | | Target Price | $ 0.600 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | O-Net Technologies | 877 | 27/09/2016 | No Rating | | 4.02 | | O-Net communications | 877 | 26/10/2010 | BUY | 7.15 | 6 | | | BAIC | 1958 | 20/10/2016 | BUY | 9.8 | 7.93 | | BAIC | 1958 | 19/10/2016 | BUY | 9.8 | 7.93 | | | | Wisdom Sports Group | 1661 | 11/07/2016 | Buy | 3.3 | 2.18 | | NetDragon | 777 | 16/06/2016 | Buy | 28.4 | 22.9 | | | Kangmei Pharmaceutical | 600518 | 05/10/2016 | BUY | 20.1 | 16.22 | | China Traditional Chinese Medicine | 570 | 13/09/2016 | Accumulate | 4.4 | 3.98 | | | Guangzhou Baiyunshan Pharma | 874 | 18/10/2016 | Buy | 24.48 | 19.16 | | Guangzhou Baiyunshan Pharma | 874 | 17/10/2016 | Buy | 24.48 | 19.16 | | | CONCORD NE | 182 | 24/10/2016 | Buy | 0.60 | 0.000 | | SINGYES SOLA | 750 | 14/10/2016 | Buy | 5.1 | 4.12 | | | 361 Degrees | 1361 | 26/08/2016 | Buy | 3.2 | 2.48 | | Poly Culture | 3636 | 25/08/2016 | Accumulate | 23.5 | 19.84 | | | SMIC | 981 | 28/09/2016 | Accumulate | 1 | 0.86 | | Byaa Interactive | 434 | 05/07/2016 | Accumulate | 3 | 2.71 | | | ¤Ñ¼w¤Æ¤u | 609 | 06/09/2016 | ¼ÈµLµû¯Å | | 1.95 | | Fortune REIT | 778 | 23/08/2016 | No Rating | | 9.65 | | | HUADIAN FUXIN | 816 | 07/10/2016 | Buy | 2.51 | 1.84 | | Dynagreen | 1330 | 26/09/2016 | Buy | 5.52 | 4.14 | | | Goldpac Group | 3315 | 18/02/2015 | N/A | | 4.77 | | IGG | 8002 | 21/11/2014 | Accumulate | 3.95 | 3.44 | | | Jinjiang Hotels | 2006 | 08/07/2016 | Accumulate | 2.98 | 2.49 | | CUTC | 600358 | 08/03/2016 | N/A | | 10.41 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2016 Phillip Securities (HK) Ltd. All Rights Reserved.

|