|

|

|

*Advertisement* |

|

|

|

|

|

26 May, 2016 (Thursday) |

MAN WAH HLDGS(1999)

Analysis¡G

Man Wah Holdings (1999) has announced the final results for the year ended 31 March 2016. Benefited from its continual efforts in product innovation, productivity enhancement and channel expansion, the Group continued to maintain a steady revenue growth trend. Its total revenue rose by 11.8% to HK$7.32 billion. Net profit attributable to shareholders increased 23.4% to HK$1.32 billion. The overall gross profit margin increased from 35.6% to 39.5% year -on-year, mainly attributable to revenue growth and the fall of main raw material prices. EPS increased 22.7% to HK68.3 cents. It is currently trading at 14.5 times historical P/E. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $9.70, Target Price: $11.50, Cut Loss Price: $8.90

|

|

ZTE(763)

Analysis¡G

ZTE Corporation realized the revenues of RMB100.1 billion in 2015, a year-on-year increase of 23%; net profit stood at RMB 3.21million, a year-on-year increase of 21.8%. The export restrictions imposed on ZTE by the U.S. Department of Commerce cut net profit by about RMB0.57 billion. Excluding the factor, the net profit stood at RMB3.78 billion, a year-on-year increase of 43%. Moreover, the Company invested RMB12.2 billion into research and development in 2015, a year-on-year increase of 35%. R&D cost rate was 12.2%. The investment was distributed mainly to products like 5G products, high-end routers, LTE, SDN, core chips, etc. and will serve as technical support for mid- and long-term development. We hold estimation that the growth will keep high within the next two years. Firstly, China Unicom and China Telecom have entered a period of rapid development in building the 4G network, which will sustain the steady development of domestic communications device market. Meanwhile, with rising 4G infrastructure in emerging markets, the Company, equipped with technological and branding advantages, will gain benefits in the mid and long term. Secondly, the requirements of cloud computing, big data, the Internet of Things and so on for data flow is increasing by geometric progression and the construction of broadband and transmission networks is fastening, which will trigger demands for optical network products in an all-round manner. There were worries that the U.S. export restrictions on ZTE may severely impact the supply chain of the Company and further affect product supply. However, the new management has promised to operate in accordance with laws and regulations. Besides, this event is related to Sino-U.S. trade relations, so an agreement is expected to be reached between ZTE and the U.S. administration, thus minimizing the negative influences.

Strategy¡G

Buy-in Price: $9.76, Target Price: $12.50, Cut Loss Price: $9.00

|

| |

|

Air China (753.HK) - Buy Opportunity Arose in Slack Season

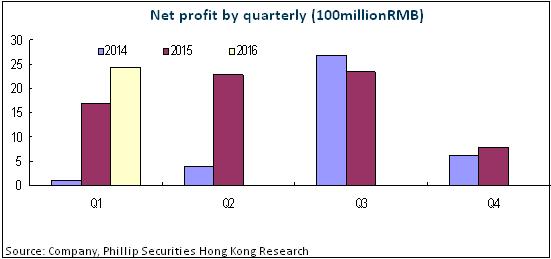

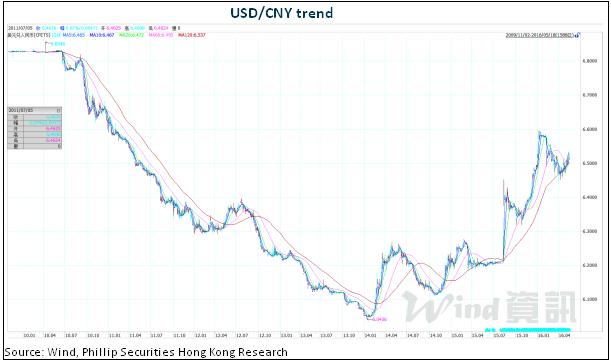

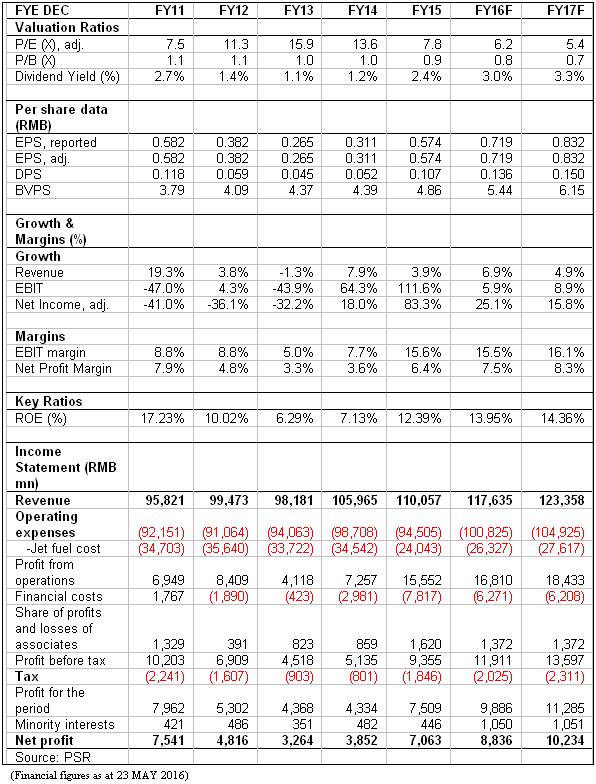

Net income in 2016Q1 Surged by near to 50%According to Air China's First Quarterly Report 2016 (China Accounting Standards), it recorded a revenue of RMB26.39 billion in 1Q16, up 4.38% Y-o-Y. Its net profit attributed to the parent company rose by 44.8% to RMB2.33 billion, and EPS was RMB0.20. More rapid growth in revenue than that in oil cost, with less input in marketing and financial expenses mainly contributed to such substantial increase. FY2015 Results Soared by 83.7%A plunge in the crude oil cost led to an annual growth of 83.7% in attributable net income in 2015, though the total revenue increased only by 4%. Meanwhile, over RMB5 billion exchange loss caused by renminbi's depreciation offset part of the profit. Excluding that offset, the company could have registered a 182% year-on-year increase in final results. Aviation data Maintained Steady GrowthIn 2016, Air China continued to accelerate the deployment of transport capacity for international routes. International ASK in the first four months of 2016 had grown by 26% year-on-year, leading to a 25.7% Y-o-Y increase in international passenger turnover, far higher than 4.6% and 4% Y-o-Y increase respectively in its domestic routes. Remaining stable on the whole, Passenger Load Factor dropped by 0.3ppts to 79.9%. Direct selling continued to enjoy a bigger share. Throughout the first quarter, sales on the official website have reached 26.6% proportion of its total ticket booking, representing a Y-o-Y increase of 12.8 percentage points. Additional four jets were bought to join a fleet of 594 airplanes in total during 2016Q1. The management of Air China made it clear that they will carry forward the strategy of hub network and innovation of business pattern to strengthen service competitiveness with respect to digital and Internet-based service. In the meantime, they will optimize the debt structure and increase direct selling for more tangible gains. Valuation & Investment thesisCurrently, the company is burdened with US dollar-denominated debt of 67.3%, down by 6.2 percentage points, year-on-year. The debt burden is expected to drop to 60% by the end of 2016. We hold that the two-way volatility RMB rate is becoming a notable trend, which is likely to become stable in mid-term. Since the second quarter, international oil price has climbed up by 30% compared with the first quarter, yet there was no remarkable growth compared with last year's average. We will continue to track the fuel cost since it takes a huge proportion in total cost of airlines. After the slack season of June, then will comes the traditional peak season. It is advisable to invest in the aviation sector before the slack season ends. The target price is maintained at HKD7.09, and P/E estimates 8.3x/7.2x in 2016/2017. ¡§Buy¡¨ rating is given. (Closing price as at 23 May 2016)

Financials

Click Here for PDF format...

| Recommendation on 26-5-2016 | | Recommendation | BUY | | Price on Recommendation Date | $ 5.360 | | Suggested purchase price | N/A | | Target Price | $ 7.090 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | Guangdong Land Holdings | 124 | 18/04/2016 | Buy | 3.15 | 2.3 | | China Merchants Bank | 3968 | 16/03/2016 | Buy | 22 | 15.96 | | | Air China | 753 | 26/05/2016 | BUY | 7.09 | 0.000 | | BOC Aviation | 2588 | 20/05/2016 | Subscribe | | 42 | | | KERRY LOG NET | 636 | 18/05/2016 | No Rating | | 10.78 | | MAPLELEAF EDU | 1317 | 06/05/2016 | Accumulate | 6.24 | 5.93 | | | | LESSO | 2128 | 23/09/2015 | Buy | 7.9 | 6.02 | | FORTUNE REIT | 778 | 14/10/2014 | Accumulate | 7.32 | 6.92 | | | HSBC | 5 | 09/08/2013 | Accumulate | 100.4 | 84.25 | | HSBC Holdings PLC | 0005 | 09/05/2013 | Accumulate | 95 | 87.7 | | | Fosun Pharma | 2196 | 16/05/2016 | Accumulate | 22.86 | 19.4 | | Hengrui Medicine | 600276 | 10/05/2016 | BUY | 56.5 | 46.92 | | | Poly Culture | 3636 | 18/03/2016 | Accumulate | 19.5 | 17.1 | | CUTC | 600358 | 08/03/2016 | N/A | | 10.41 | | | Yunnan Water | 6839 | 23/05/2016 | Buy | 5.7 | 3.94 | | Grandblue ENV | 600323 | 20/04/2016 | Buy | 17.5 | 13.11 | | Food, Beverage and Retail | | | |

| | Peak Sport | 1968 | 13/05/2016 | Buy | 2.25 | 1.83 | | Kweichow Moutai | 600519 | 22/03/2016 | Buy | 280 | 226 | | | ZTT | 600522 | 24/05/2016 | Accumulate | 24.16 | 20.73 | | Cowell e Holdings | 1415 | 09/05/2016 | Buy | 3.7 | 2.78 | | | TSC GROUP | 206 | 28/07/2015 | Buy | 2.8 | 2.11 | | SPT Energy | 1251 | 24/02/2015 | Reduce | 1.5 | 1.74 | | | Goldpac Group | 3315 | 18/02/2015 | N/A | | 4.77 | | IGG | 8002 | 21/11/2014 | Accumulate | 3.95 | 3.44 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2016 Phillip Securities (HK) Ltd. All Rights Reserved.

|