|

|

|

*Advertisement* |

|

|

|

|

|

6 May, 2016 (Friday) |

UMP(722)

Analysis¡G

UMP Healthcare Holdings (722) announced that, UMP Healthcare China, its wholly owned subsidiary, has entered into the Master Management Agreement with Health Ventures, a wholly-owned subsidiary of Chow Tai Fook Enterprises, which exclusively appointed UMP Healthcare China as the manager to manage and operate all the Clinics to be established by Healthcare Ventures in the PRC. Those clinics will provide outpatient general practice services, specialist services, dental services and auxiliary healthcare services. This will enable UMP Healthcare Holdings to rapidly expand the geographical coverage of its clinic network in the PRC without incurring significant pre-opening and ramp up expenses and will diversify and increase its income streams and cash flow. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $1.30, Target Price: $1.55, Cut Loss Price: $1.20

|

|

ZTE(763)

Analysis¡G

ZTE Corporation realized the revenues of RMB100.1 billion in 2015, a year-on-year increase of 23%; net profit stood at RMB 3.21million, a year-on-year increase of 21.8%. The export restrictions imposed on ZTE by the U.S. Department of Commerce cut net profit by about RMB0.57 billion. Excluding the factor, the net profit stood at RMB3.78 billion, a year-on-year increase of 43%. Moreover, the Company invested RMB12.2 billion into research and development in 2015, a year-on-year increase of 35%. R&D cost rate was 12.2%. The investment was distributed mainly to products like 5G products, high-end routers, LTE, SDN, core chips, etc. and will serve as technical support for mid- and long-term development. We hold estimation that the growth will keep high within the next two years. Firstly, China Unicom and China Telecom have entered a period of rapid development in building the 4G network, which will sustain the steady development of domestic communications device market. Meanwhile, with rising 4G infrastructure in emerging markets, the Company, equipped with technological and branding advantages, will gain benefits in the mid and long term. Secondly, the requirements of cloud computing, big data, the Internet of Things and so on for data flow is increasing by geometric progression and the construction of broadband and transmission networks is fastening, which will trigger demands for optical network products in an all-round manner. There were worries that the U.S. export restrictions on ZTE may severely impact the supply chain of the Company and further affect product supply. However, the new management has promised to operate in accordance with laws and regulations. Besides, this event is related to Sino-U.S. trade relations, so an agreement is expected to be reached between ZTE and the U.S. administration, thus minimizing the negative influences.

Strategy¡G

Buy-in Price: $11.72, Target Price: $13.50, Cut Loss Price: $11.00

|

| |

|

MAPLELEAF EDU (1317.HK) - Stable Profit Growth and Bright Prospect

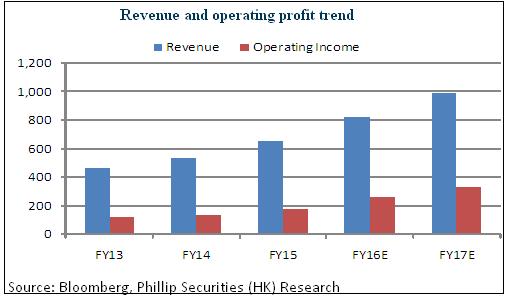

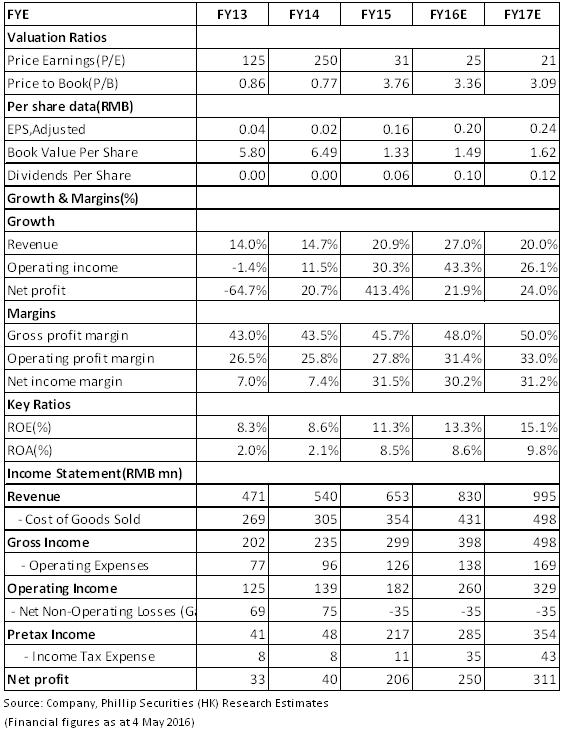

Significant Growth in Main Financial Indicators In the FY2015 the company's income totaled RMB653 million, growing by 20.9% over last year. This growth is mainly attributed to RMB87.8 million, the increase in revenue from tuition, as well as RMB10.3 million, the increase in revenue from summer and winter camps. The gross profit for the year stood at RMB298 million, with a gross profit margin of 45.7%. Also, the adjusted net profit for the year reached RMB185 million, up 45.8%. In the six months ended 29 February 2016, the company's revenue reached about RMB380 million, an increase of 26.7% over the same period last year. The adjusted net profit was RMB117 million, rising by 69.7%. The company announced an interim dividend of HK$0.042 per share.

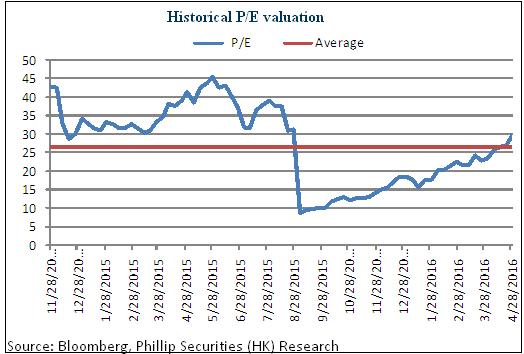

Increase in the Number of Students Enrolled and TuitionIn the FY2015, tuition remained the dominant source of revenue, and amounted to RMB555 million, a YoY increase of 18.8%, representing 84.9% of total revenue. The rise primarily resulted from the increase in student enrollment. On the other hand, the average tuition was RMB37,483 per person, witnessing no major changes. As of 31 March 2016, the total number of students enrolled in the company stood at 19,353, soaring by 20.4% from 16,078 students on 30 June 2015. Additionally, in the 2015/2016 school year, the company also increased the tuitions of some schools. Accordingly, in the six months ended on 29 February 2016, the average tuition per student in the company saw an increase of approx. 6.6% over the same period last year. It is expected that the company's results will be steadily enhanced as steady growth of the number of students enrolled and the increase in tuition income. Various Measures Boost Earnings GrowthFuture growth of the company depends on the continuous increase in students enrolled to receive K-12 education and services. In addition to the natural growth of existing school network, the company will keep cooperating with the government or local property developers. Besides, it will open more schools in an asset light model. Specifically, in the future, the company will build 18 new schools (from kindergarten to high school), and increase the number of students by 54% from 26,090 in FY2015 to 40,290 in FY2018. In addition asset light development, the company is also considering setting up or acquiring schools at home and abroad. At present, other education services revenue accounts for about 15% of the company's revenue. In the future, the company will also enhance incidental earnings by broadening services. Valuation and RatingWith the increase of China's household income, parents are more ready to send their children to study abroad, coupled with the favorable support of the universal two-child policy, the market of international schools will be further expanded. As China's largest international educational institution, Mapleleaf Edu will benefit from this growth of demand in education market. Additionally, the company also intends to achieve its growth target by means of multiple expansion strategies, such as the increases in the capacity of certain existing schools, ramp-ups of the utilization of new schools, and asset light expansions and acquisitions. On this basis, we expect the company's future profitability will be significantly improved. Therefore, we give the company the 12-month target price of HK$ 6.24, equivalent to 26X and22X the 2016/2017 expected P/E ratio and ¡§Accumulate¡¨ rating is given. (Closing price as at 4 May 2016)

Risk WarningsChanges in China's education policy; Changes in international educational needs; Financials

Click Here for PDF format...

| Recommendation on 6-5-2016 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 5.930 | | Suggested purchase price | N/A | | Target Price | $ 6.240 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | Guangdong Land Holdings | 124 | 18/04/2016 | Buy | 3.15 | 2.3 | | China Merchants Bank | 3968 | 16/03/2016 | Buy | 22 | 15.96 | | | GAC | 2238 | 05/05/2016 | BUY | 12 | 9.07 | | SIA | 600009 | 27/04/2016 | Buy | 34.8 | 28.31 | | | MAPLELEAF EDU | 1317 | 06/05/2016 | Accumulate | 6.24 | 0.000 | | HengTen Networks | 136 | 28/04/2016 | No Rating | | 0.35 | | | | LESSO | 2128 | 23/09/2015 | Buy | 7.9 | 6.02 | | FORTUNE REIT | 778 | 14/10/2014 | Accumulate | 7.32 | 6.92 | | | HSBC | 5 | 09/08/2013 | Accumulate | 100.4 | 84.25 | | HSBC Holdings PLC | 0005 | 09/05/2013 | Accumulate | 95 | 87.7 | | | KPC Pharmaceuticals | 600422 | 12/04/2016 | BUY | 39.6 | 30.01 | | Humanwell Healthcare | 600079 | 05/04/2016 | Buy | 24.66 | 18.2 | | | Poly Culture | 3636 | 18/03/2016 | Accumulate | 19.5 | 17.1 | | CUTC | 600358 | 08/03/2016 | N/A | | 10.41 | | | Grandblue ENV | 600323 | 20/04/2016 | Buy | 17.5 | 13.11 | | Grandblue ENV | 600323 | 19/04/2016 | Buy | 17.5 | 13.11 | | Food, Beverage and Retail | | | |

| | Kweichow Moutai | 600519 | 22/03/2016 | Buy | 280 | 226 | | Tianyi Summi | 756 | 07/03/2016 | Buy | 2 | 1.23 | | | China Railway Signal & Communication | 3969 | 04/05/2016 | Buy | 5.56 | 4.62 | | China Railway Signal & Communication | 3969 | 03/05/2016 | Buy | 5.56 | 4.62 | | | TSC GROUP | 206 | 28/07/2015 | Buy | 2.8 | 2.11 | | SPT Energy | 1251 | 24/02/2015 | Reduce | 1.5 | 1.74 | | | Goldpac Group | 3315 | 18/02/2015 | N/A | | 4.77 | | IGG | 8002 | 21/11/2014 | Accumulate | 3.95 | 3.44 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2016 Phillip Securities (HK) Ltd. All Rights Reserved.

|