The largest risk of the banking industry comes from the decrease of the asset quality

According to 3Q results of China's banking sector, there were three main factors of the listed banks` operating performance: 1) the decrease of the profit growth, 2) the slight increase of assets, and 3) the accelerated deterioration of the asset quality. The largest risk was coming from the sharp growth of the banks` NPLs and the ratios.

The major reason of the decrease of the banks` performance is the deterioration of China's macroeconomic environment. As at the end of Sep 2015, China's GDP was 6.9%, and 7.0% in the previous two quarters. According to Goldman Sachs's latest report this week, it estimate China's GDP growth should maintain at 7.0% in 2016, but we think this is quite hard to achieve, and it's more reasonable to be around 6.8% due to the trend of the decrease of China's economic growth in the medium and long term.

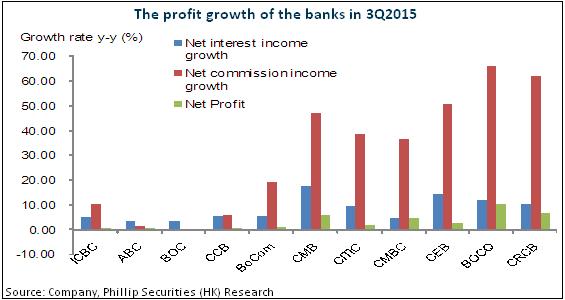

The banks` interest income growth slowed down obviously because of the decrease of the loan growth due to the decrease of the economic growth. By the end of 3Q, CMB's net interest income gained the largest growth as 17.7% among the peers, and BOC had the lowest growth as 3.14%. Meanwhile, the listed banks` intermediate business increased strongly due to the bull market in 1H, although there was a large volatility in 3Q. Due to the low base, the growth of the small and medium-sized banks was much higher than the large-sized banks. BOCQ gained the largest growth of net fee and commission incomes, with the y-o-y growth of 65.90%, compared to BOC's -0.82%, the only bank which had the negative growth during the same period. In the largest five state-owned banks, only BoCom's net profit growth was higher than 1%. The change of the profit growth meets our previous expectation.

In the whole year of 2015, the profit growth would increase slightly in 4Q benefited from the improvement of the market environment. However, we expect the banks` growth rate will continue to decrease due to the slow-down of the economy and the decrease of interest rates, and some banks` profits would experience the negative growth in 4Q this year or 1Q next year.

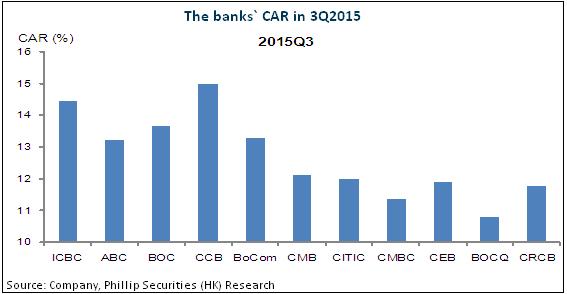

The banks` assets continued to increase although the profit growth slowed down. Meanwhile, the large-sized banks still have more advantages in asset scale than the other banks. According to the CAR, the capital of the large-sized banks was richer than the small and medium-sized banks, of which CCB had the highest CAR as 14.97%, compared with the lowest one of BOCQ as 10.78%.

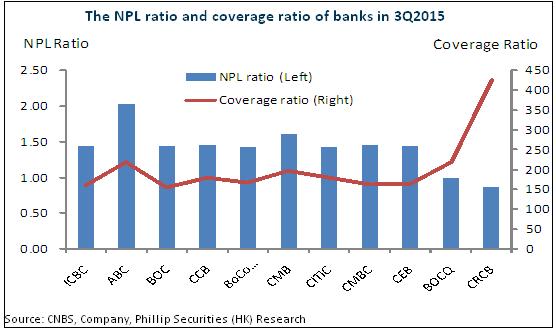

As at the end of 3Q2015, the asset quality of the banks continued to decrease, the average NPL ratio of the industry was 1.38% compared with 1.13% in 2014. Excluding HRB and HSB (No data in 3Q), ABC's NPL ratio was the highest as 2.02%, compared with CRCB's 0.86%, the lowest one.

We expect the banks` asset quality will continue to go down, representing the consistent growth of the NPL ratio in future, and it will cause impairment losses to go up and increase operating expenses sharply, which will offset the positive impact of other income growths. It would be the largest operating risk of the listed banks.

Risk

Lower-than-expected growth of main business incomes;

The deterioration of the asset quality due to the sharp growth of the NPLs;

Share prices of the listed banks decrease largely affected by the market environment in the short run.

Click Here for PDF format...