Business of first three quarters in 2015 beat expectations

The Q3 report of Shanghai International Airport revealed that the total revenue in the first three quarters of 2015 amounted to RMB 4.72 billion, grew by 10.45% yoy; net profit attributable to shareholders increased by 21.9% yoy to RMB 1.924 billion, so that the corresponding earning per share recorded as RMB 1.00. Such result is better than our expectation. The net profits recorded in Q1, Q2 and Q3 are RMB 628 million (RMB 0.33 per share), RMB 664 million (RMB 0.34 per share), and RMB 633 million (RMB 0.33 per share) respectively, keeping fast growth rate with double digit in an overall sense.

Cost control in the first three quarters was satisfactory with the advantage of economies of scale. The Company's cost of sale, management fees and financial costs reduced more than 80 million compared to the same period last year; but income from investment dropped nearly 40 million yoy because of the profit downturn of fuel companies.

Fast growth of air traffic

In mid 2014, the Company's increase of maximum hourly capacity from 65 aircrafts to 74 aircrafts was approved, and the official opening of the fourth runway in Pudong airport enabled the release of more time resources of flights: the maximum hourly capacity increased from 74 aircrafts to 90 aircrafts. Moreover, the current international crude price is remaining at a low level and thus airline companies have stronger incentives to keep flying their routes. There are several factors inducing fast growth of air traffic of the Company.

In the first three quarters of 2015, the number of aircraft taking-off and landing exceeded 333,800, which grew by 12.45% yoy. The growth of domestic routes (16%) surpassed the growth of international routes (12%) (We considered such phenomenon was due to the capacity of Hongqiao Airport being fully utilized and parts of the domestic routes were transferred to Pudong Airport.) Regional routes slightly dropped by 3%. The Company recorded passenger throughput as 45.31 million, up 18% yoy. The growth of number of domestic passengers was still higher than that of international passengers, which amounted to 21% and 19% respectively. Cargo and shipment throughput reached 2.4 million tons, slightly increased by 3.6% yoy.

Investment Thesis

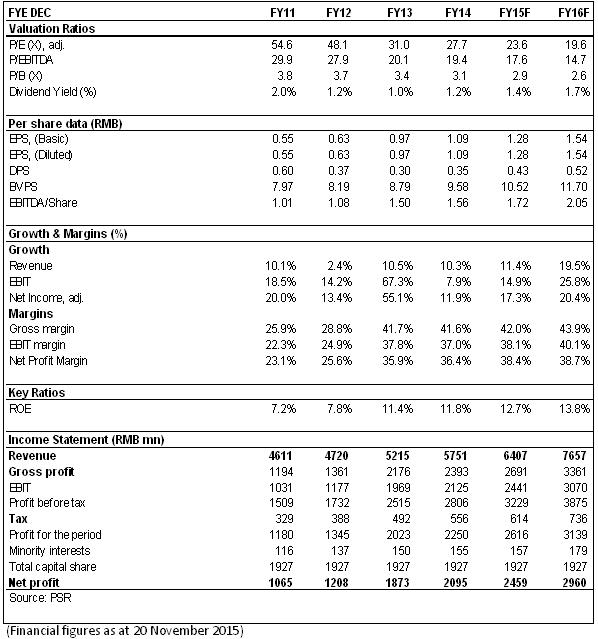

We expect the Company's EBITDA per share in 2015 and 2016 will be RMB1.72 and RMB 2.05 respectively, which is based on the valuation of 21.5x 2015e and 18x 2016e, with the corresponding target price set as RMB 36.87. We give a rating of ¡§Buy¡¨. (Closing price as at 20 Nov 2015)

Company Profile

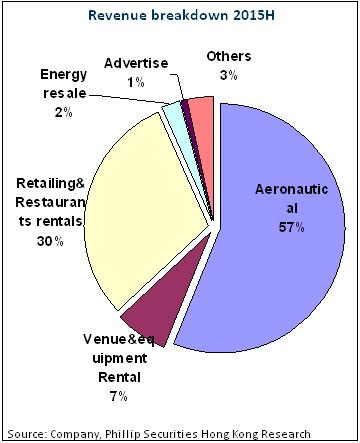

Shanghai International Airport Company Limited's major assets include Shanghai Pudong International Airport, and Shanghai Hongqiao International Airport which is operated and managed by a holding company owned by Shanghai Airport Authority. The Company's sources of income include aeronautical business (aircraft taking off and landing fees, passenger service charges, and airport fees) and non-aeronautical business (advertising, franchise loyalty from retail shops, and parking fee and rent from car parks etc.). Pudong Airport currently has four runways and two terminals, with passenger handling capacity of 60 million passengers. The total equity of the Company amounted to 1.927 billion shares, of which Shanghai Airport Authority (wholly owned by State-owned Assets Supervision and Administration Commission of Shanghai Municipal Government) holds 53%.

Fast growth of business expected to maintain

In regard to the most recently ranked top 10 Chinese airports, the throughput of Pudong Airport surpassed Baiyun Airport and ranked the second. The fifth runway of Pudong Airport is under construction and it will be the trial runway of locally produced large-sized aircrafts. The project of Southern Satellite terminal will be kicked off soon and will add 105 parking stations, which are all linked to the main terminal by mass railway transport system. It is expected that the bottleneck problem of inadequate parking positions due to a few number of terminals currently in operation would be solved upon commencement of operation of this new terminal. It is expected that the annual passenger throughput of Shanghai Pudong International Airport would exceed 80 million by 2020, while cargo and shipment throughput would exceed 3.4 million tons. It may rank among globally top 10 airports.

On the demand side, we expect the opening of Shanghai Disneyland and the establishment of free trade zone would bring new opportunities of growth. It not only brings higher growth of passenger flow to Pudong Airport, but also enhances the main business of the Company. In addition, it will open up more room for developing non-aeronautical business for the Company.

Financials

Click Here for PDF format...