Summary

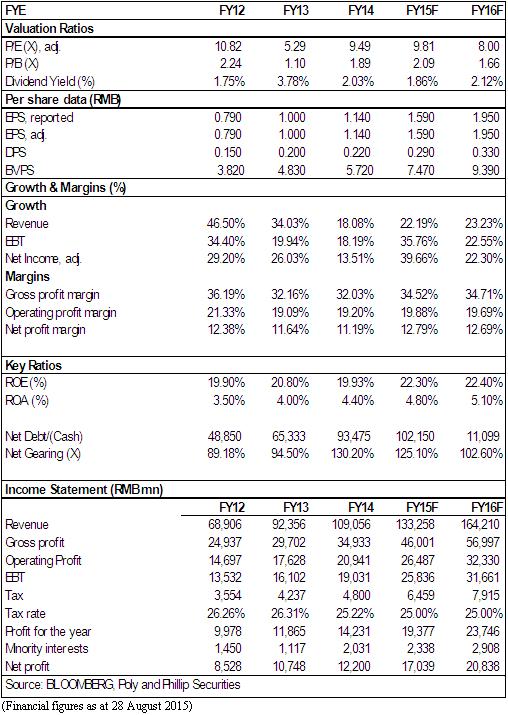

2015H1, the company reported a 24.55% yoy growth in revenue to RMB42.345 billion. Net profit attributable to shareholders grew by 29.5% yoy to RMB4.95 billion while core net profit increased by 32.6% yoy to RMB4.885 billion. Basic EPS was up by 27.78% yoy to RMB0.46.

During the reporting period, gross profit margin and net profit margin expanded by 2.52%-point and 1.61%-point to 36.3% and 13.94% respectively, which were higher than those achieved by industry leaders and industry average. The improvement in the company's profitability was mainly due to profit recognition of high-margin projects such as those in Guangzhou and Shanghai. The average contracted selling price grew by 1.56% from 2014 to RMB13,000 psm in H1.

In H1, Poly Real Estate reported contracted sales of RMB76 billion. Contracted GFA sold increased by 16.7% yoy to 5.85 million sq.m. Of which, the amount of contracted sales and subscription reached historical highs of RMB25.7 billion and RMB22.8 billion respectively. During the period, the market share of the company increased by 0.41%-point from 1.8% at end-2014 to 2.2%, which was just lower than that of Vanke, Evergrande and Greentown.

On the one hand, the pick-up in the sales growth of the company was due to a broad-based recovery of the property market. On the other hand, it also benefited from the strategy of clustering around ¡§3+2+X¡¨ cities. In H1, the reported cumulative revenue from three core regions, namely the Pearl River Delta, Yangtze River Delta and Bohai Rim areas, was over RMB53 billion, accounting for over 70% of contracted sales. In terms of product mix, the company mainly focused in ordinary housing, which accounted for 84% of total GFA. Of which, 91% was from ordinary housing with unit size of 144 sq.m. or below. The company focuses its expansion in Tier 1 regions. By positioning itself in serving the market mainstream, the company hs greatly enhanced its resistance to risks during business development.

As of June 2015, Poly Real Estate had RMB38.7 billion cash on hand, which was equivalent to 1.3x of its short-term debts. In addition to an estimated operating cash flow of RMB40 billion in the coming 12 months, Poly Real Estate will have sufficient liquidity to meet cash out flows from the maturity of its RMB29.2 billion short-term debts and committed land lease.

As of June 2015, the total debts of Poly Real Estate decreased from RMB126.2 billion at end-2014 to RMB122.6 billion. Continued strong contracted sales, faster cash collection from contracted sales and lower expenditure on land acquisitions attributed to the fall in the company's leverage ratio in H1. Benefiting from rate cuts in China and the issuance of onshore medium-term notes, the company's funding cost dropped from 6.5% at end 2014 to 5.68% at end-June.

The strong cash flows of Poly Real Estate provided strong liquidity support to its transformation in business model. While real estates continues to be Poly Real Estate's core business, it is actively seeking changes in profit mix. The 5P Strategy (namely old-age care real estate, whole-life-circle green buildings, community O2O, Poly Real Estate APP, and overseas real estate) is the main direction for its business transformation. We are optimistic that Poly Real Estate will achieve solid breakthroughs in its 5P Strategy, which will also become its new sources for profit growth, in the coming three years.

The interim result of Poly Real Estate was in line with expectations and its sales outperformed its peers. Besides, diversified funding channels, lower funding costs and strong cash flows are the key advantages of its business transformation. Against the background of a loosening government control in the property market in order to stimulate the macro economy, the valuation of Poly Real Estate becomes attractive. We maintain our ¡§BUY¡¨ rating in Poly Real Estate, with a 12-month target price of RMB15.6, which is equivalent to prospective 2015/2016 P/E of 10x and 8x. (Closing price as at 28 Aug 2015)

Financials

Click Here for PDF format...