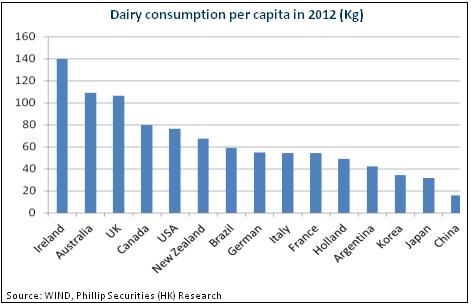

The demand space of dairy products in China remains large. In 2014, our country's urban per capita dairy products consumption was 28.3 kg, which was far lower than 220.3 kg, the level of developed countries, and even did not reach the level of developing countries. Currently the dairy market structure shows the characteristics of oligopoly, and Yili's revenue, total market value and market share take the first place. Plus with the grown demand, we think Yili's market share will increase.

Yili enjoys the moat advantages. Firstly, the trust degree of Yili brand is better than those of the competitors. Secondly, the marketing channels are wide and deep. Thirdly, the company controls the milk source. It has already built milk source bases in the three major golden milk source regions of our country-the Xilingol Grassland of Inner Mongolia, the HulunBuir Grassland and the Tianshan Grassland.

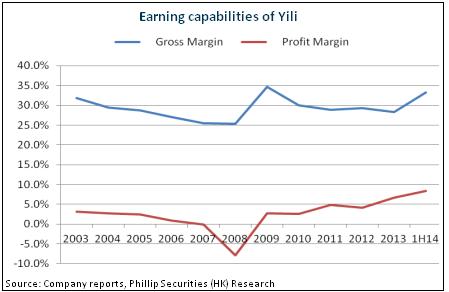

The profitability will improve. First, raw materials` price lowers. Due to annual settlement contracts, scale ranches` price did not lower until the fourth quarter. Next, Yili's product mix improves. In 2013, the company released normal temperature yoghurt "£D£O£E£T£RS£L£DL", started to increase volume in 2014, and may earn billions of Yuan in sales in 2015. In addition, the company also promoted walnut milk, and the products` gross margins are all above 40%. What's more, expense management is also good for profitability improvement.

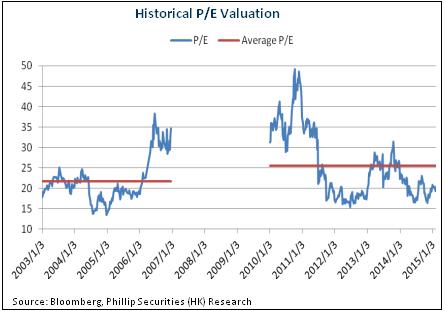

"Buy" rating for low valuation

YILI underperformed the HS300 index significantly in 2014. But, as the leading enterprise that enjoys sound reputation and has strong marketing ability, the company's advantages are obvious. Besides, dairy products market itself has a broad space, the structure of oligopoly is also favorable for the company to take more market shares, and we expect the company will maintain a steadily fast growth. The valuation of the company is only 15X corresponding to the performance in 2015, which is obviously lower than its peer. We temporarily grant it the valuation of 20X, with the target price of CNY34.98 and "Buy" rating initially.

Still great expansion space as the industry leader

With economic development and the increase of per capita disposable income, China's dairy products market has achieved remarkable development. However, the demand space of dairy products in China remains large. In 2014, our country's urban per capita dairy products consumption was 28.3 kg, which was far lower than 220.3 kg, the level of developed countries, and even did not reach the level of developing countries. Even compared with the neighboring countries of Japan and South Korea which have the similar diet with China, our country's per capita dairy products consumption is also only about a half of their level.

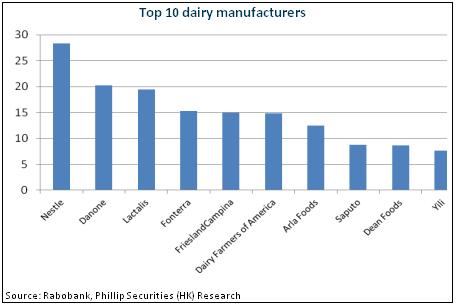

At present, among domestic dairy companies, Yili, Mengniu and Brightdairy are the top three, CR3 reaches 47%, and the market structure shows the characteristics of oligopoly. Among them, Yili's revenue, total market value and market share take the first place. In 2014, Yili was just promoted to the tenth place in the global dairy products industry. Up to the end of 2014, the company's market shares in liquid milk, kids` milk and milk beverage were respectively 35%, 33% and 21%, and the increase speed already exceeded the main competitors. We believe that, there is still a great expansion space for the capacity of domestic dairy products market, and that the leading companies which have brand, scale, channel, milk source and other advantages, such as Yili, will benefit from this, and their market shares are also expected to increase.

The moat advantage

Firstly, the trust degree of Yili brand is better than those of the competitors. After experiencing the melamine incident in 2008 and the Mengniu incident in 2011, the brand of Yili shows stronger strength. The company is also the only dairy products enterprise in the world that meets double standards of the Olympic Games and the Expo and provides products and service for the 2008 Beijing Olympics and the 2010 World Expo.

Secondly, the marketing channels are wide and deep. Yili is the enterprise that firstly conducts the channel sinking and innovation in the industry. Early in 2006, the company carried out the "Weaving Net Project" all over the country, and became the first dairy products enterprise that covers the national market. Meanwhile, the company pays attention to the deep ploughing of channels, and the channels continue to sink to the markets of the third and fourth tier cities as well as villages and towns, and have entered point-of-sale terminals of villages and towns such as "Countryside Stores" in virtue of the "Ten Thousand Villages and Thousand Townships " activity of the Ministry of Commerce since 2007. In 2013, the company put forward the "Global Weaving Net Project", which is essentially the integration of global distribution and industrial chains. The overseas expansion will also be a positive watching focus.

Thirdly, YILI controls the milk source. The milk source of China concentrates in the northern areas, so the milk source and cost advantage of grassland-type dairy products enterprises such as Yili can`t be surpassed by city-type dairy products enterprises. The company has already built milk source bases in the three major golden milk source regions of our country-the Xilingol Grassland of Inner Mongolia, the HulunBuir Grassland and the Tianshan Grassland.

The profitability will improve

Ever since listed, the company's profitability maintains a relatively steady state, for instance, the gross margin is generally around 30%. In 2014, benefited from factors like dropping costs of raw milk, the company's profitability improved. We believe that this trend will continue in 2015.

First, raw materials` price lowers. Currently, the domestic fresh and raw milk is in a descending stage; compared with the high spot at the beginning of 2014, it has dropped around one fifth, and the New Zealand-imported dried milk's price even lowers half. Besides, in the cost structure of Yili raw milk, large-scale ranches take up 30% and family ranches account for 60%. Although the latter's settlement price apparently dropped in 2014, due to annual settlement contracts, scale ranches` price did not lower until the fourth quarter.

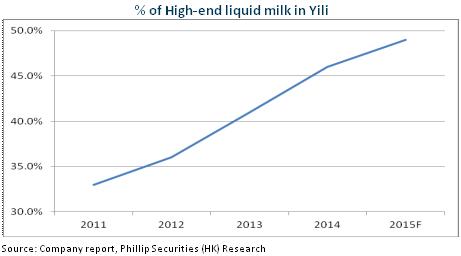

Secondly, its product mix improves. Around 60% of Yili's revenue comes from normal temperature milk, and its gross margin is only 20%-25%, whereas yoghurt's gross margin is 35%-40%, ice cream 30%-35%, high-class white milk such as YiliSatine over 40%. In 2013, the company released normal temperature yoghurt "£D£O£E£T£RS£L£DL", started to increase volume in 2014, and may earn billions of Yuan in sales in 2015. In addition, the company also promoted walnut milk, and the products` gross margins are all above 40%.

Thirdly, expense management is also good for profitability improvement. Sales scale expansion will lower the average sales costs. As far as advertisement expenses are concerned, the Yili brand has taken firm root among the crowds, so the future advertisement investment's growth can slow down. In addition, benefiting from the layout of factories in the neighborhood and the full-load transportation of single goods, the efficiency of logistics supply chain will increase, and the expenses for loading, unloading and transportation will decline.

Catalyst

Products` high-end orientation exceeds the expectation;

Strategy of internationalization is advanced.

Risk

Price of raw milk increases significantly;

The sales of Yili's new milk products do not reach to the expectation;

Food safety risk.

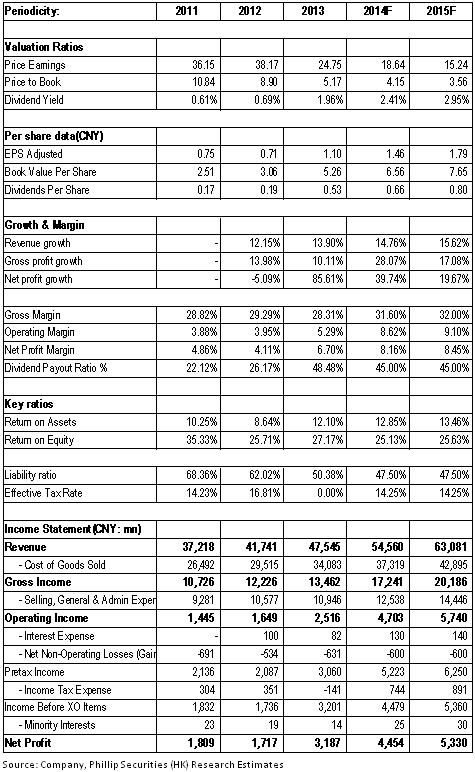

Financials

Click Here for PDF format...