Annual Target to be Overfulfilled

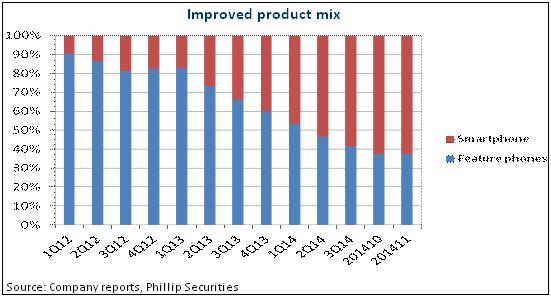

TCL Communication Tech sold 8.286 million cell phones and other products totally in November, rising by 14% year on year. The total sales volume of the last 11 months rose by 32% year on year to 64.917 million. Among them, smart phone accounted for 62% with the increasing share. The Company is expected to overfulfill its guiding target of 40 million. Thanks to the improvement of product structure, the Company¡¦s product ASP rises significantly. Additionally, with the release of scale effect, the profitability will also continue to improve.

Benefiting from the Overseas Emerging Markets Continuously

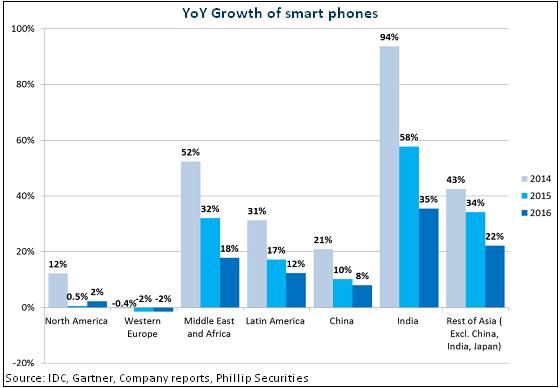

The emerging markets, except those of China, still have a huge alternative space. TCL Communication is also one of the limited brands which will benefit from the tide of replacing functional phones with smart ones. Since the Company mainly worked on these markets in the past, over 90% of smart phone shipment is from overseas markets.

4G Embraces Considerable Opportunities

4G market still has vast development space. Given that operators provide low subsidies, the low-cost 4G cell phones are expected to be more popular. TCL will benefit from this progress, for it enjoys solid channels. Besides, the close cooperation with MTK will help it develop more cost-effective cell phone products. MTK¡¦s more competitive SoC processors to be available in the first half of 2015 can accelerate the products to be put into market. In addition, the gross margin of 4G cell phones is 1 to 2 percentage points higher than that of 3G ones.

Major Shareholders Buy in More Shares Positively

Although the Chinese mainland market may be confronted with ceiling effect, TCL Communication works on overseas markets. Its smart phone business is expected to maintain rapid growth. And benefiting from the scale advantage offered by the Chinese mainland industrial chain, the improvement of product structure and scale effect, the profitability will be also improved. It is worth mentioning that major shareholders bought in as many as 7.87% of shares positively in the past three months, showing their optimistic confidence. The Company¡¦s average historical P/E is about 10 times. Even if we cautiously grant it 9X 2015EPS, the target price can be HK$ 10.13. We upgrade it to ¡§Buy¡¨ rating.

Annual Target to be Overfulfilled

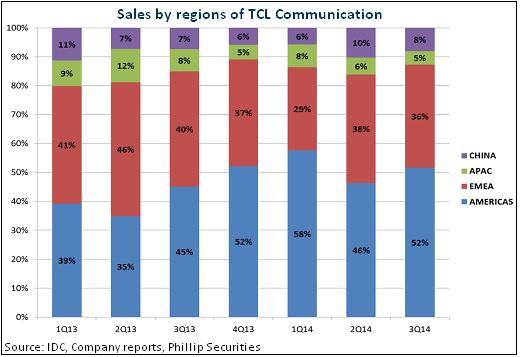

TCL Communication sold a total of 8.286 million cell phones and other products in November, rising by 14% year on year. 7.511 million ones were sold overseas, increasing by 9% year on year. The sales volume in Chinese market rose substantially by 100% year on year to 775,000. The sales volume of cell phones and other products in the last 11 months rose by 32% year on year to 64.917 million, of which a total of 58.705 million were sold overseas, rising by 32% year on year. A total of 6.212 million were sold in China, rising by 42% year on year.

Among them, the sale volume of smart phones rose substantially by 70% year on year to 5.115 million in November, which accounted for 62% of the total sales volume with the larger share. The total sales volume in the last 11 months rose by 140% year on year to 36.06 million.

It is simply estimated that the Company will achieve an annual shipment of 41.18 million which is slightly higher than the guiding target of 40 million if the smart phone shipment of December maintains at the same level as that of November. Thanks to the improvement of product structure, the Company¡¦s product ASP rises significantly. Additionally, with the release of scale effect, the profitability will also continue to improve.

Benefiting from the Overseas Emerging Markets Continuously

After years of development, the permeability of smart phones in Chinese mainland has reached 66%, which is close to or even higher than that of some developed countries. ¡§The ceiling effect¡¨ has appeared. However, the emerging markets, except those of China, still have huge alternative space. TCL Communication is also one of the limited brands which will benefit from the tide of replacing functional phones with smart ones. Since the Company mainly worked on these markets in the past, over 90% of smart phone shipment is from overseas markets. Meanwhile, the Company also enjoys the following competitive advantages. First, it works closely with the global operators and distributors (70%+contribution). Second, it boasts of higher cost performance. Third, its brand TCL-Alcatel enjoys fine recognition.

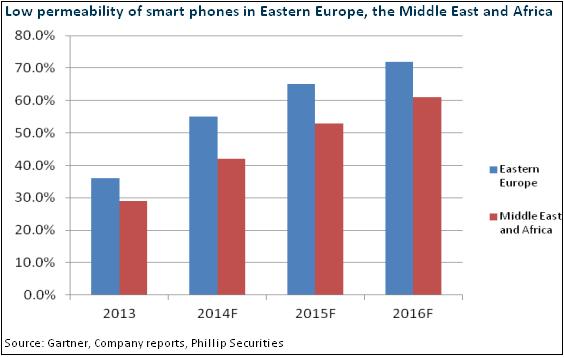

It is worth mentioning that the American markets, whose revenue contribution is over half of the Company¡¦s revenue, facing an opportunity of replacing the functional phones with smart phones in Latin America. Moreover, the Company will have a new cooperator, Sprint, in the North American market and Verizon will be a new potential cooperation partner. Channel development is also expected to improve the Company¡¦s local market share. In addition, markets of Eastern Europe, the Middle East and Africa whose total revenue contribution is about 40% of the Company¡¦s revenue, have low permeability of smart phones. In those regions, the cell phones with a price of less than $ 200 also gradually occupy the market share of the high-end cell phones. The entry-level smart phones of TCL Communication are only sold at a price of $ 60 to $ 80, which is expected to boost it to win the market.

4G Embraces Considerable Opportunities

Despite the fact that the permeability of 4G in markets of Western Europe and Japan is relatively higher (nearly 80%), that of North America is about 50% and China and Russia and other emerging countries is only about 20% to 30%. 4G market still has vast development space. Given that operators provide low subsidies, the low-cost 4G cell phones are expected to be more popular.

We believe TCL Communication will benefit from this progress, for it not only enjoys solid channels. Besides, the close cooperation with MTK will help it develop more cost-effective cell phone products. MTK¡¦s more competitive SoC processors to be available in the first half of 2015 can accelerate the products to be put into market. In addition, the gross margin of 4G cell phones is1 to 2 percentage points higher than that of 3G ones.

Catalyst

Major shareholders buy in more shares positively;

Overseas market expansion better than expected.

Risks

Smart phones didn¡¦t replace functional ones in emerging markets as scheduled;

The competition between smart phone manufacturers in emerging markets is more intense.

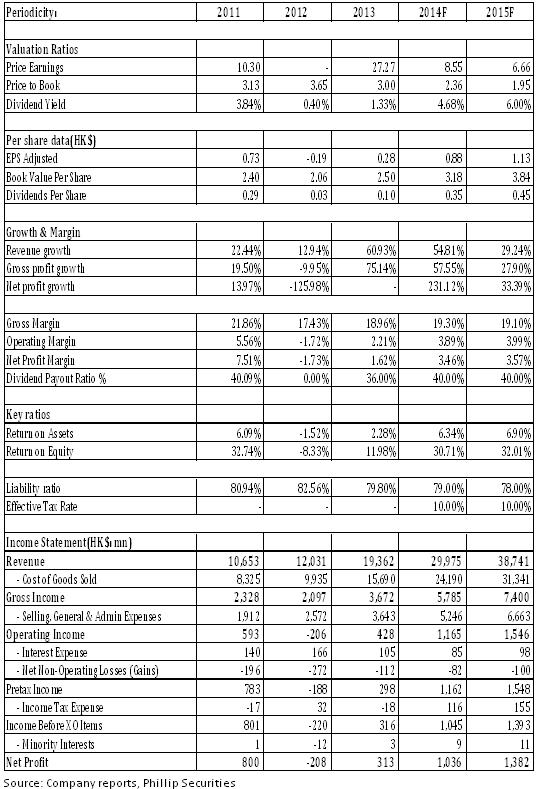

Financials

Click Here for PDF format...