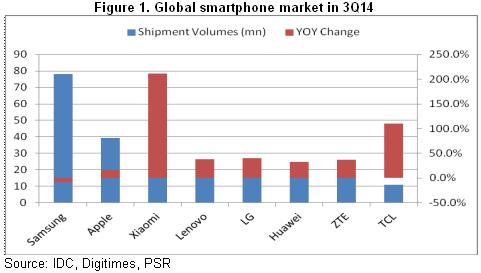

-In the third quarter, Xiaomi became the third smart cellphone manufacturer on the global list with its 17, 300 thousand shipments and 5.3% market share; Huawei took the sixth place with 16, 800 thousand and 5.1% share. The two companies¡¦ smart phone shipments increased 211.3% and 32.3% respectively. Tongda Group expects that its cellphone casings will account for 30-40% and 20-25% of Huawei and Xiaomi's shipments respectively, and it will become the major beneficiary of the mainland's cellphone manufacturers` business expansion.

-The company owns the only complete LDS antenna production line in the mainland. This kind of technology is manly applied in 4G cellphones. It is expected that over 30% of domestic 4G products will apply the LDS technology. Therefore, the company will benefit from the rapidly expanding 4G market. Considering LDS and cellphone shell's bonding sell, and that higher selling price can be accomplished, the profitability is to be higher than that of the current business.

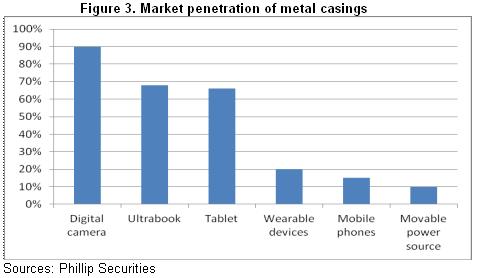

-Metal casings` application in the smart phone market will continue to improve. The company's amount of CNC machine tools will rise from 200 in 2013 to 500 at the end of this year. And it will also manufacture more metal cellphone casings in the future. Overall speaking, metal casings have more attractive prices and profitability. Therefore, in the future, the company's cellphone shells business will improve in both production capacity and structures.

-The company's businesses have extended to the production of parts as automotive upholstery. There is not only an increase of 90 million cars but also bigger decoration demands of stock market in the automobile industry. Besides, automobile parts possess great profitability, whose gross margin is as high as 30%. Therefore, we expect that automotive parts will become the company's new growth power in the middle period.

Investment Action

Smart phones` growth is slowing down, and the major its main technical application fails to reach the expectation, which both negatively impact on its recent performance. However, with the 4G market swiftly expanding and metal casing production capacity increasing, it is expected that the company's revenue and profitability will continue to improve.

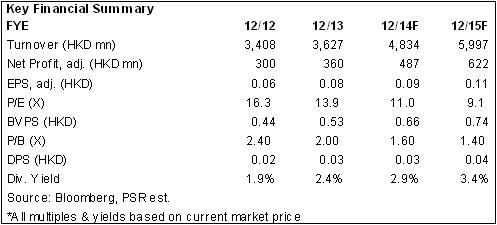

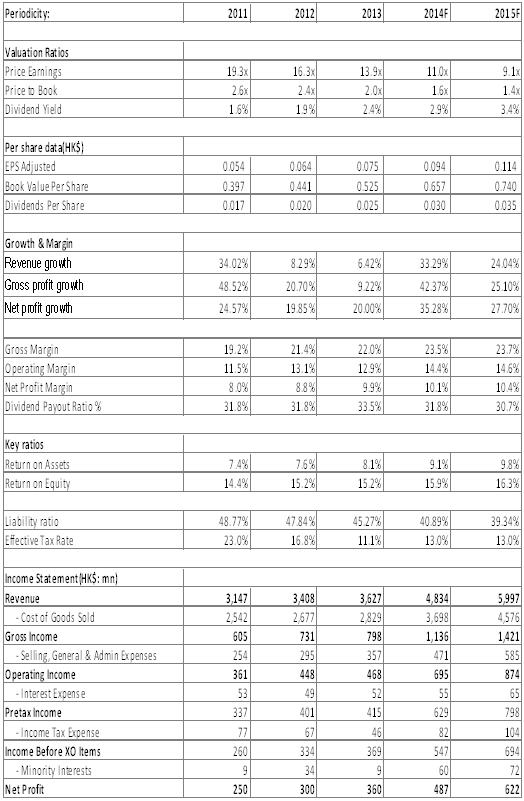

Although the company¡¦s scale is relatively small, its ability of sustainable growth is rare in the sector. Even conservatively granting it 12X times of EPS in 2015, the target price can reach 1.37 HKD, 35% premium than the latest closing price. We maintain it "Buy" rating.

To benefit from major clients` rapid growth

About half of Tongda Group's revenue comes from cellphone shells, and its major clients cover renowned manufacturers as Xiaomi, Huawei, Coolpad, ZTE and OPPO. As the biggest client, Huawei¡¦s revenue contribution is as high as 30%. Xiaomi and Coolpad only started to largely increase their amounts in the first half year of this year, but their contributions are only standing at single-figure.

According to the IDC statistics, in the third quarter, Xiaomi became the third smart cellphone manufacturer on the global list with 17, 300 thousand shipments and 5.3% market share; Huawei took the sixth place with 16, 800 thousand and 5.1% share. It is worth mentioning that the two smart phones` shipments in the third quarter were 211.3% and 32.3% respectively. In response to the rapid increase of clients` demands, the company's subsidiary Xiamen factory's new production capacity was part of the production in September. It is expected that by the end of 2014, its cellphone shells` annual production may rise by 50% to 60 million, and the company also predicts that cellphone shells will account for 30-40% of Huawei's shipments and 20-25% of Xiaomi 's shipments respectively. Therefore, the company is expected to be the major beneficiary of the mainland's cellphone manufacturers` business expansion.

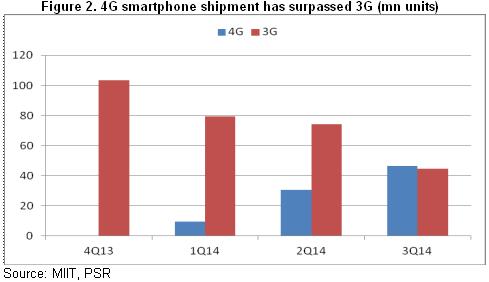

It is worth mentioning that the mainland's 4G market is rapidly expanding. There are about ten millions of new users every month, and the extension speed is greatly faster than that in the 3G age. Huawei and others are introducing relevant products. We believe that in the future, with the issuing of FDD national license, the 4G market will expand even faster. The company owns the only complete LDS antenna production line in the mainland, which is manly applied in 4G cellphones. It is expected that over 30% of domestic 4G products will apply the LDS technology. Therefore, the company will benefit from the rapidly expanding 4G market. Considering LDS and cellphone shell's bonding sell, and that higher selling price can be accomplished, the profitability is to be higher than that of the current business.

Metal casings` contribution may increase

At the moment, the company is oriented on plastic cellphone shells, which account for about 90%, whereas metal shells only take up 5-6%. What is worth to be brought about is that, after Apple, which is a leading enterprise that applies metal parts, more cellphone manufacturers are employing metal shells, including HTC, Nokia, Huawei, Xiaomi and so forth. As the one with the biggest share of smart phones, Samsung has also continuously released metal shell products recently. In 2013, the permeability of cellphones with metal shells already reached 15%. According to the application trend of digital cameras, tablet computers and ultrabooks using metal parts, we believe that metal shells` application in the smart cellphone market will continue to increase.

Adapting to this trend, the company has actively put investment in CNC machine tool to increase production capacity. The amount of CNC will rise to 500 by the end of the year from 200 in 2013, and the company will manufacture more metal cellphone shells in the future. Metal shells generally have more attractive prices and profitability, and some types` gross margin is as high as 30%, which is far higher than the company's profitability of 20%. Therefore, in the future, the company's cellphone shells business will improve in both production capacity and structures.

Diverse business expansion supports the continuous growth

In the past ten years, the diverse business structure of cellphones, laptops and electronic products guarantees the company's steady growth. This year, the company's business starts to extend to the production of parts as automotive upholstery. To our knowledge, this act is to relieve laptops and other businesses` depression. Although there is still an extensive market available for smart phones that have been supporting the development, the growth power is slowing down. There is not only an increase of 90 million cars but also bigger decoration demand of stock market in the automobile industry. Besides, automobile parts possess great profitability, whose gross margin is as high as 30%. Therefore, we expect that automotive parts will become the company's new growth power in the middle period.

Catalysts

LDS market's substantial extension;

Development of new clients.

Risks

Price pressure by intensified competition of smartphone vendors;

New plants are not put into operation as expected.

Click Here for PDF format...