„h Sinosoft¡¦s 1H14 revenue up 27.7% yoy while gross profit grew 39.4% yoy. GPM sharply increased 6.14 ppt. to 73.25% and net profit rose 52.7% yoy. EPS amounted to RMB 4.47 cents, no interim dividend.

„h Benefited by the national policy on carbon emission trading, and cooperation with environmental protection companies, the carbon management solution is expected the future growth momentum.

„h The PRC government supports to local IT service providers enabled the company to grab market share from foreign leading companies.

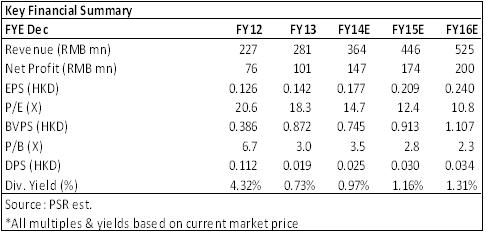

„h We maintain the rating of Sinosoft as ¡§Accumulate¡¨ and increase the target price to HK$ 2.94, equivalent to 15x/12.7x of 2014 and 2015 forecasted EPS, plus cash per share of HK$ 0.29.

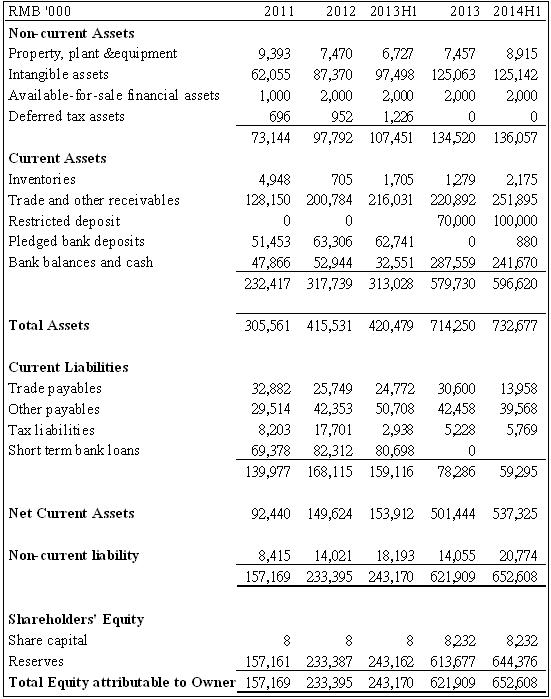

Financial Highlights

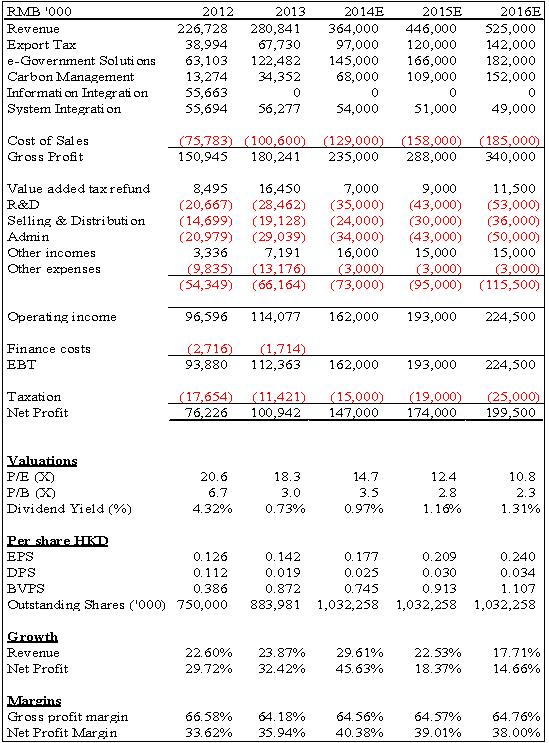

The growth on Sinosoft speeded up in the 1H14. Revenue reached RMB 133 mn, up 27.7% yoy while gross profit grew 39.4% yoy to RMB 97 mn. Both of them were accelerated when compared to 2013 full year results. Gross profit margin sharply increased 6.14 ppt. to 73.25% and net profit rose 52.7% yoy to RMB 46 mn both showed better cost control in the first half. Earnings per share amounted to RMB 4.47 cents, no interim dividend.

How we view this

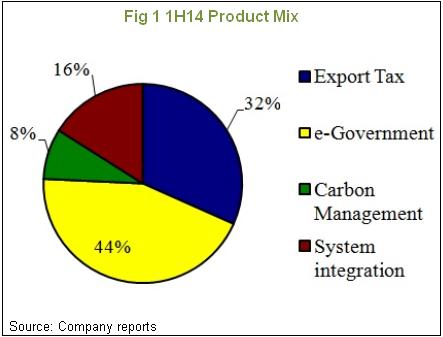

The accelerated revenue growth was mainly contributed by the growth on export tax software and carbon management solutions, which yearly grew 42.9% and 39.4% respectively. Margins also sharply improved in 1H14, but we expect the GPM to go down since the company used to put in heavy selling effort and promotions in the second half. Meanwhile, we are optimistic about the future growth on the carbon management solution due to the national policy on carbon emission trading. Sinosoft had collaborated with the subsidiary of China Energy Conservation and Environmental Protection Group (CECEP Group) to develop system and platform on the carbon related solutions.

Investment Action

Previously, the foreign IT solution companies, such as Oracle, IBM and Microsoft dominated the IT service market in mainland. But the PRC government had recently increased its concerns on the Internet information security, and tried to employ more local software, which allowed the local IT service providers to grab more market share. Thus, we maintain the rating of Sinosoft as ¡§Accumulate¡¨ and increase the target price to HK$ 2.94, equivalent to 15x/12.7x of 2014 and 2015 forecasted EPS, plus cash per share of HK$ 0.29.

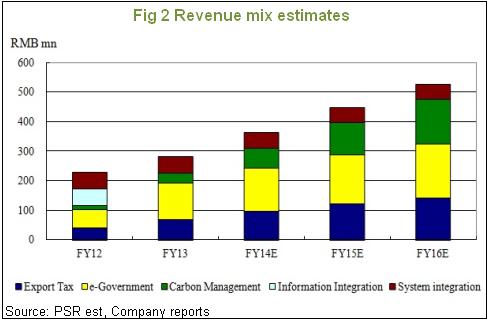

Export tax software and carbon management business remained high growth

Sinosoft had obtained good results, revenue growth rate accelerated, which mainly contributed by the export tax software and carbon management solution business. The export tax business was once the largest revenue contributor before the merger of e-Government and information integration. The consulting and training services of export tax became significant sources of income.

The carbon management solution started at 2011 and achieved rapid growth in these years. According to company¡¦s listing prospectus, there were only three companies which provided carbon related monitoring software in 2012, and it was the only one provider in Jiangsu Province. It is expected the revenue from carbon management business will surpass the declining system integration business at the end of this year and gradually becomes the second largest revenue contributor to Sinosoft.

According to the China International Software & Information Service Fair (CISIS), it is predicted that the investment in information security by private companies will increase by 30% this year, while government and enterprises is projected to spend 7.8% more on software purchase.

Potential Risks

High competition on the integration solution business;

The growth on carbon management solution slowdown.

Financial Status

Financial Status

Click Here for PDF format...