The three major operators announce that they will fund 10 billion yuan to establish China Communication Facilities Service Limited Company (IE "Tower Company"). Tower Company clearly states that it will favor China's Communication Service Co., Ltd. (CCS) under equal conditions when it publicly outsources its design, construction, supervision and maintenance of the tower and its related supporting facilities on prerequisite that it does not lead to the breach of the Non-competition Treaty between China Telecom and CCS. If stock assets registration happens, the agent maintenance agreement signed by initiators of Tower Company and CCS will still be effective. When the contract expires, it will carry out outsourcing, and still favor CCS under equal conditions.

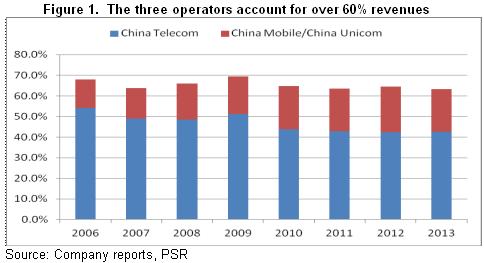

On the whole, the operation of Tower Company this time is only limited to tower rather than basic station, the investment of which only accounts for 5% of the operator's CAPEX. Therefore, the adverse effect of it on communication industry in terms of capital spending is smaller than market expected previously. Besides, the company has no non-governmental capital, and CCS further gains priority. Therefore, the cooperation framework between CCS and the three major operators is not affected. The turnover of the company of general contribution of 3 major operators is over 63%. It is worth mentioning that currently the continuous development of mainland mobile virtual network operation will benefit from the reform process from a mid-term and long-term perspective. It will benefit the non-operator business of CCS. In 2013, in this field the company grows 16.1%, above the 9% growth rate of operators.

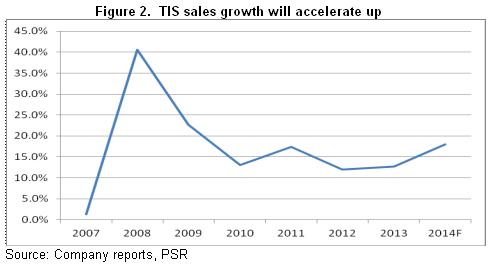

The market effect of 4G has already appeared. We believe that it will promote the investment of China Telecom and China Unicom in 4G. By the end of June, the two companies have gained FDD-LTE. Currently, China Telecom has opened 4G business in 16 cities. It is reported that in 2013 China Telecom has invested about 13.2 billion yuan in the construction of 4G on accumulative basis. In 2014, the investment is expected to exceed 40 billion yuan. In next 2 to 3 years, the investment will continue to increase with larger scale, exceeding hundred billion yuan. It is worth mentioning that the market share of CCS reaches 80%. Therefore, we believe the 4G business contribution in the last half year is expected to accelerate. The company's TIS department will be the major beneficiary of LTE investment upswing period.

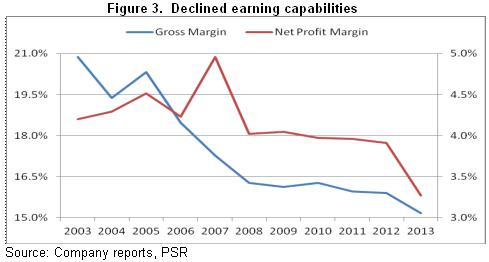

The profitability of the company is continuously weak. Gross margin decreased from 20.9% of 2003 to 15.2% of 2013. Net profit margin decreased from 5% of 2007 to 3.3%. We expect that the profitability difficulty the company face will continue. Except for price pressure of operators and the cost upswing of human resources after the end of demographic dividend, the set-up of Tower Company will also weaken the price negotiating right and further bring pressure to profit margin.

Investment Action

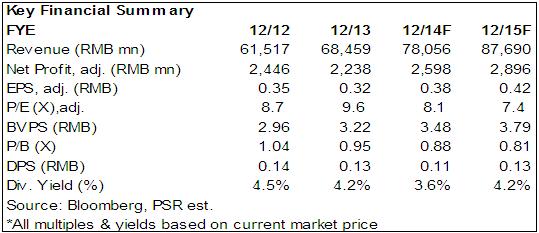

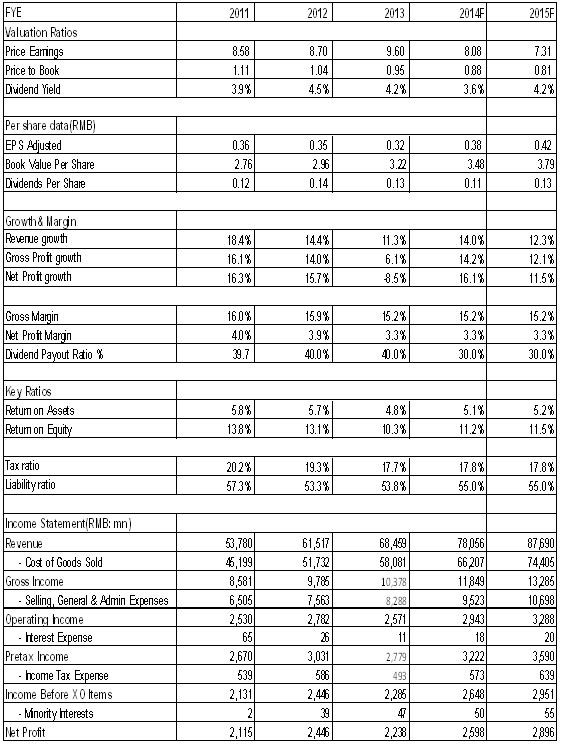

4G investment upswing cycle will promote the acceleration of company's domestic business. Meanwhile the impact of Tower Company's upcoming establishment is lower than market expectation. We expect that turnovers of 2014 and 2015 will be 78.1 billion yuan and 87.7 billion yuan respectively. Net profit will be 2.598 billion yuan and 2.896 billion yuan, a year-on-year growth of 16.1% and 11.5%, and the EPS will be 0.38 yuan and 0.42 yuan.

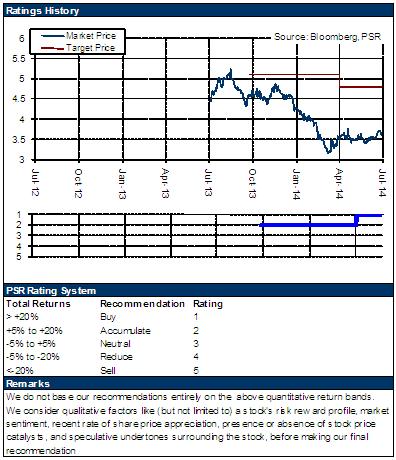

The company has maintained steady growth after listing and we make valuation by referring to price-to-earnings ratio. By looking back the history of the company, as the profitability falls off, the central price-to-earnings ratio also falls from 10.6X of 2010-2011 to 9.4X since 2012. However, considering the 4G motive power may accelerate, we grant it 10 times of the EPS valuation of 2014, and the 12-m target price is HK$4.7. We maintain it ¡§Buy¡¨ rating.

Click Here for PDF format...