Company introduction

China Construction Bank's predecessor was founded in 1954, and was restructured as commercial bank in 2004, which now is one of the leading large-sized commercial banks in China. By the end of 2013, according to total assets, CCB was the second largest bank in China, and was listed in H and A Shares in 2005 and 2007 respectively.

Summary

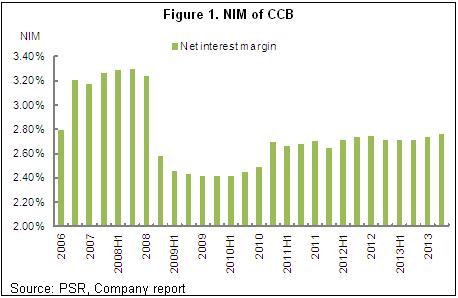

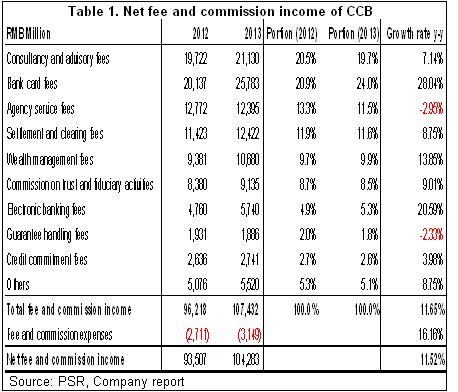

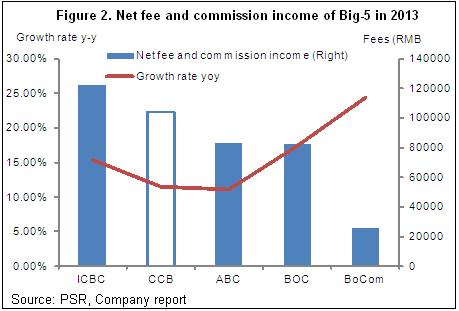

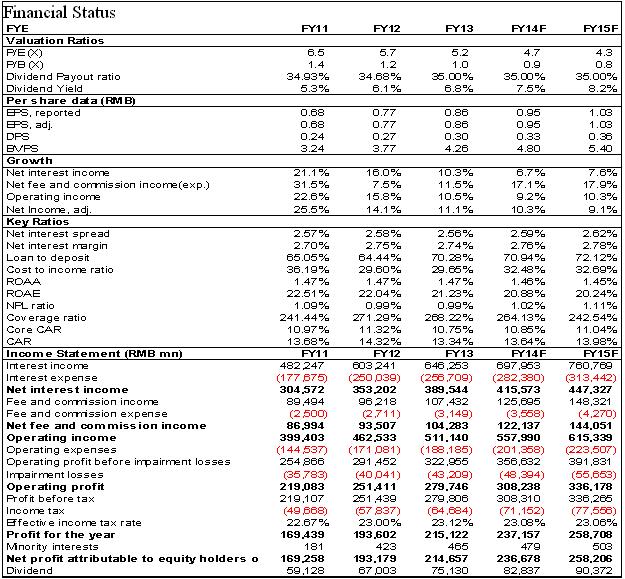

-According to China Construction Bank's (CCB or the Group) 2013 results, its accumulated net interest incomes amounted to RM389.544 billion, up 10.3% y-y approximately and the growth rate slowed down compared with that of 2012. Intermediate business increased largely due to the development of the market of which accumulated net fees and commission incomes increased by 11.5% y-y to RMB104.283 billion, especially new products recorded better performance such as credit card and newly financial consultant business, but the growth rate of intermediate business was lower than the peers;

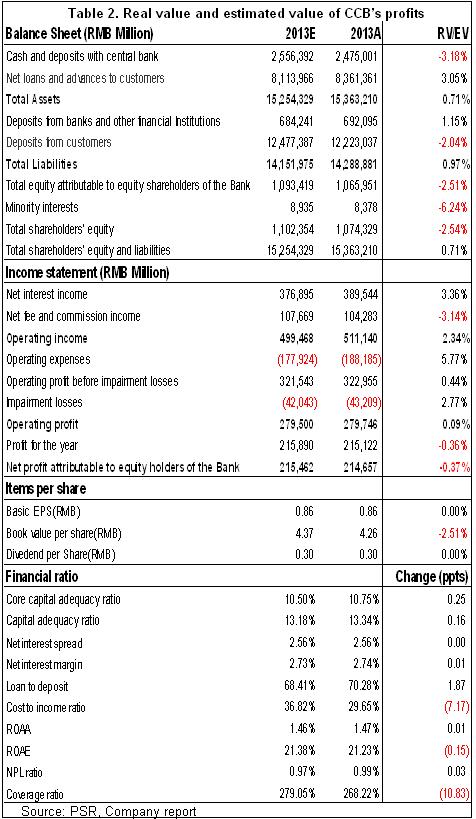

-The Group's operating incomes recorded RMB511.14 billion, up 10.5%, and net profits increased by 11.12% y-y to RMB214.657 billion, the profit growth met our previous expectation;

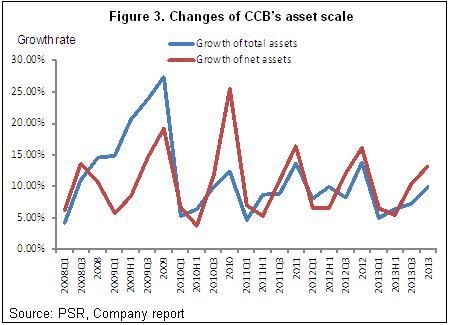

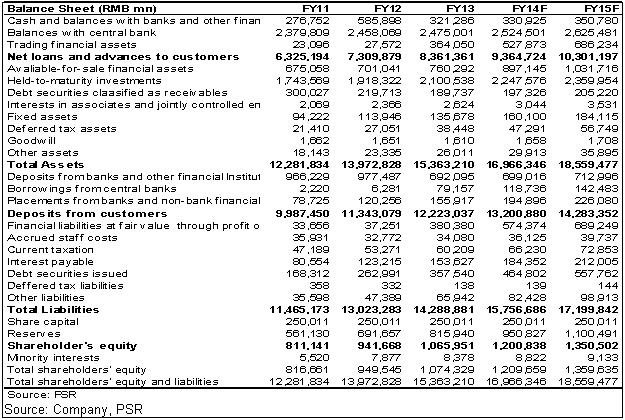

-The Group's total assets increased by 9.95% to RMB15.36 trillion compared with the end of 2012. Net assets rose 13.20% to RMB1.07 trillion, equivalent to the BVPS of RMB4.30. Although there was the decrease of investment revaluation reserve, surplus reserve and retained profits increased obviously compared with the same period of 2012, therefore CCB's net assets still achieved quite strong growth;

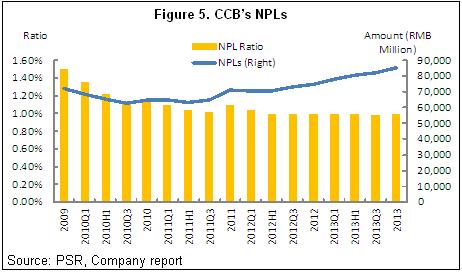

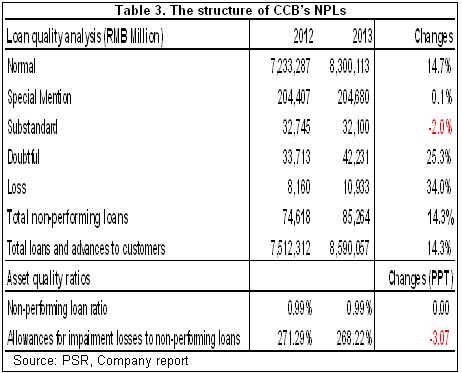

-The ability of CCB's risk control was quite good and the loan quality kept stable in 2013. NPL ratio recorded 0.99% as same as 2012, but the coverage ratio decreased by 3.07ppts to 268.22% mainly caused by the large increase of the NPLs, especially for doubtful and loss loans. Considering the trend of the changes of the NPLs, we expect CCB's NPL ratio will go up continually with the risk of the deterioration of the loan quality in the next few quarters;

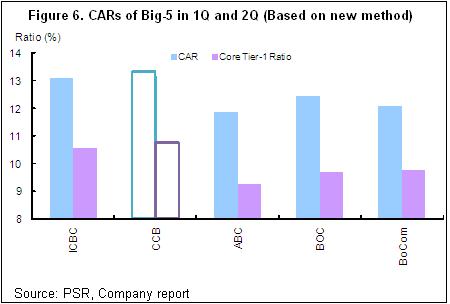

-The CAR of CCB decreased due to the implementation of new calculation method of capital in 2013, and the Group's CAR and Core Tier-1 CAR recorded to 13.34% and 10.75% respectively by the end of 2013, down 0.29ppts and 0.17ppts respectively compared with that of 1Q, however the CAR was still on the top of the peers, representing smaller capital pressure for the bank relatively;

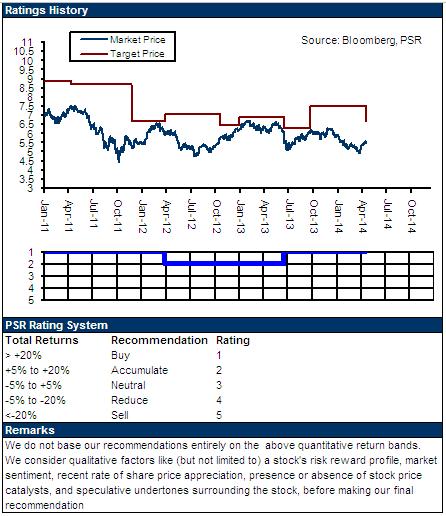

-In all, considering stable profit growth of CCB, in line with our expectation, we still hold optimistic view on the bank's future performance, but estimate the profit growth would go down continually and net profits should increase by 10% y-y approximately in the next two years. Moreover, considering the slow-down of profits in future and the risks of the deterioration of assets, we cut CCB's 12-month target price to HK$6.70, around 22% higher than the current price, equivalent to P/E5.2x and P/B1.0x in 2015 respectively, the valuation is quite attractive. Maintain Buy rating.

Click Here for PDF format...