|

Chow Tai Fook (1929)

Analysis¡G

Chow Tai Fook announced its fiscal year results for the period ended March 31, 2026, demonstrating significant success in its brand transformation and delivering high-quality profit growth. During the year, turnover increased 5.3% year-on-year to HK$94.398 billion, while profit attributable to shareholders rose 52.2% to a record HK$9.004 billion. Gross margin improved to 32.3%, supported by surging gold prices and higher sales contribution from uniquely designed, high-margin flagship product series. Coupled with effective cost control, operating profit grew 27.8% year-on-year to HK$18.85 billion, pushing the operating profit margin up 360 basis points to a five-year high of 20%. The group¡¦s return on equity rose to 28.4%, continuing to improve from the historical five-year average of 20.5%. The board recommended a final dividend of HK$0.45 per share, bringing the full-year dividend to HK$0.67 per share. The full-year payout ratio for fiscal 2026 was approximately 73.4%.The group is expanding its business around three core growth drivers: reshaping the global position of Chinese luxury brands, strengthening the product portfolio and operational efficiency, and exploring new business areas. In terms of reshaping the global position of Chinese luxury brands, the Signature Collection, Chow Tai Fook Heritage Collection, and Palace Museum series maintained strong sales momentum in fiscal 2026. This drove a 16.9% year-on-year increase in retail value of priced jewelry in mainland China, lifting the mainland¡¦s share of total retail value from 30.6% last year to 35.4%, which provided support for overall gross margin. Regarding strengthening the product portfolio and operational efficiency, the group¡¦s store optimization strategy focuses on securing premium locations and developing high-quality outlets while enhancing customer experience and maximizing productivity and operational effectiveness per retail space. As of the end of fiscal 2026, the group had opened 8 new-design high-end stores in prime locations in mainland China (these stores deliver significantly higher productivity, approximately 8 to 10 times the average same-store sales). The target is to increase this to 50 stores by fiscal 2030. In exploring new areas, Chow Tai Fook launched a brand-new business line called ¡§Chow Tai Fook Home,¡¨ becoming the first Chinese jeweler to enter the luxury home furnishings sector. This lifestyle product portfolio aims to tap into diversified market segments, expand the customer base, attract and engage new clientele, and generate strong synergies with the core jewelry business. On international market expansion, the group aims to double the retail value of its international business compared with fiscal 2026 and expand its international store network to over 100 outlets. (I do not hold the above stock.)

Strategy¡G

Buy-in Price: $12.20, Target Price: $13.20-13.70, Cut Loss Price: $11.60

|

JF SmartInvest(9636)

Analysis¡G

The Company is a leading online investment decision solution provider in China, focusing on educational services and financial information software services within the online investor content service market. It offers online investor content services, including premium online investment education, online financial literacy education, and financial information software services. In 2025, the Company¡¦s operating revenue reached RMB 3.43 billion (RMB, same below), representing a year-on-year increase of 48.75%, with a gross margin of 82.2%. From a revenue mix perspective, internet financial software contributed RMB 3.19 billion (93% of total revenue), while AI terminal products (stock learning devices) generated RMB 0.24 billion (7% of total revenue). The learning devices achieved annual net sales volume exceeding 75,000 units, establishing itself as the second growth curve. Net profit attributable to shareholders was RMB 922 million, up 238.5% YoY; basic earnings per share reached RMB 2.05; dividend per share declared was HKD 0.36. The Company¡¦s business essence can be deconstructed as a three-stage model of "public-domain traffic acquisition ¡X private-domain retention ¡X monetization closed loop". On the front end, it leverages short-video platforms to build an MCN content matrix, acquiring broad public-domain traffic through professional investment education content. On the middle end, it facilitates user migration and retention into private-domain pools via enterprise WeChat and its proprietary app. On the back end, it employs refined operational strategies to achieve paid conversion, forming a complete commercial closed loop. Over the long term, we are positive on the Company's traffic conversion elasticity and growth potential driven by rising penetration.

Strategy¡G

Buy-in Price: $29.00, Target Price: $32.16, Cut Loss Price: $26.50

|

|

Foryou Group (002906.CH) - Second Growth Curve Gradually Becoming Clear

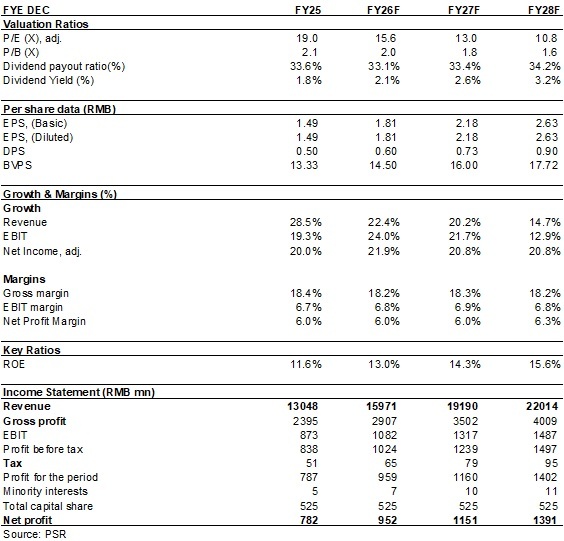

Company profileForyou Corporation was established in 1993 and is mainly engaged in the R&D, production and sales of automotive electronics and precision die-casting businesses. The Company's automotive electronics business mainly covers two core sectors, namely smart cockpit and advanced driver-assistance systems. Its precision die-casting business is centred on precision mould design and manufacturing technology, covering aluminium alloy, magnesium alloy and zinc alloy product lines. In addition, it actively explores and develops AI, robotics and other related businesses, including optical communication modules, AI high-speed connectors, robotics and other related component businesses. In 2025, the Company reported revenue of RMB13,048 million, up 28.46% yoy; net profit attributable to the parent company was RMB782 million, up 20.00% yoy. Investment SummaryQ1 Revenue Maintained High Growth

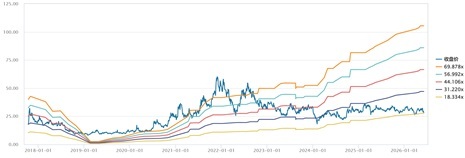

In Q1 2026, the Company reported revenue/net profit attributable to the parent company/net profit excluding non-recurring items of RMB3,096 million/RMB166 million/RMB159 million, respectively (RMB, the same below), up 24.37%/6.61%/5.89% yoy, respectively. Gross margin was 16.5%, down 1.7 ppts yoy. The slower profit growth compared with revenue growth was mainly due to factors such as price competition and rising raw material prices. The Company has established a raw material price linkage mechanism with most of its customers, and its operating results are expected to improve significantly from Q2. Automotive Electronics Business Continued to Grow, With Its Leading Position in Smart Cockpit Firmly EstablishedThe Company's automotive electronics business reported revenue of RMB9,675 million in 2025, up 27.25% yoy, accounting for 74.15% of total revenue. CAGR reached 35.66% from 2020 to 2025, maintaining high-quality growth. The Company has built a comprehensive product matrix and solution capabilities in the smart cockpit field. The market shares of HUD, in-vehicle wireless charging and other products continued to rank first in China, while the market shares of LCD instrument panels and central control screens rapidly rose to the forefront of the industry. The Company's customer structure continued to optimise, with a low dependence on any single customer, and the revenue contribution from some new energy vehicle makers and international automotive brands increased. Revenue from customers including Changan, BAIC, Xiaomi, Dongfeng, STELLANTIS, SAIC Volkswagen, BYD, Xpeng, NIO and Leapmotor increased significantly. Leveraging the ADAYO Automotive Open Platform (AAOP), the Company provides customers with "one-stop" overall smart cockpit solutions based on its implementation capabilities in cockpit domain controllers across multiple platforms including Qualcomm, SemiDrive and MediaTek, as well as mainstream large models, demonstrating significant platform-based competitive advantages. Precision Die-Casting Business Improved Its Process Technologies, Enhancing Overall CompetitivenessThe Company overcame a number of difficult technical challenges in mould design and manufacturing, expanded the application of highly flame-retardant magnesium alloy materials, and promoted the deep integration of 3D vision guidance with AI and robotics to improve the flexible changeover capability of automated manufacturing cells. Its capabilities in complex and difficult production processes, including high-vacuum combined extrusion, friction stir welding of aluminium-magnesium alloys, profiling spraying, multi-spindle machining and vacuum adsorption, continued to improve. The precision die-casting business delivered particularly impressive performance in 2025, reporting revenue of RMB2,859 million, up 38.47% yoy, with growth exceeding that of the automotive electronics business. CAGR reached 35.08% from 2020 to 2025. Second Growth Curve Gradually Becoming Clear, with Capacity Expansion Releasing Growth MomentumThe Company actively explores non-automotive businesses such as AI and robotics: 1) In the AI infrastructure field, optical communication modules, high-speed connectors and data centre cooling system components have secured project nominations; 2) In the robotics field, the Company has received orders for robotics display screens and joint module components, and jointly developed robotics main and auxiliary controllers, with brand momentum surging and sales increasing exponentially. Following a record-high scale of capacity construction in 2025, capital expenditure is expected to remain at a high level in 2026, focusing on the Thailand Production Base, the expansion of the Automotive Electronics Huizhou Base, the expansion of the zinc alloy die-casting business in the AI field, and Phase III of the Precision Die-Casting Changxing Project. Capacity expansion is being carried out based on orders on hand, providing solid support for sustained business growth going forward. Among them, the Thailand Production Base is expected to commence production in Q4 2026, providing strong support for overseas business expansion. Investment ThesisThe Company's traditional automotive business is growing steadily and rapidly, while its non-automotive business offers enormous growth potential. We are optimistic about the long-term development of the Company and expect EPS to be 1.81/2.18/2.63 yuan respectively for 2026/2027/2028, a yoy increase of 22%/21%/21%. We offer a target price of 36.3 yuan, respectively 20/16.6/13.8x P/E for 2026/2027/2028, and an "Buy" rating. (Closing price as at 5 June) Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research

RiskProgress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices Financials

(Closing price as at 5 June) Download PDF Version

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|