|

TS LINES(2510)

Analysis¡G

T.S. Lines primarily provides container shipping services. Its fleet consists of owned and chartered vessels, with a focus on the Asia-Pacific regional market, including Greater China, Greater China¡VNorth Asia, Greater China¡VSoutheast Asia, Northeast Asia¡VSoutheast Asia, Asia¡VOceania, and Asia¡VIndian Subcontinent routes. In addition to Asia-Pacific routes, the Group also operates Asia-to-Mexico services as well as Middle East and Red Sea routes. Through joint venture and slot exchange cooperation models, it further expands its market coverage. The Group continues to optimize its route portfolio. In 2025, it exited the Trans-Pacific West Coast route and refined its Asian regional route structure to improve vessel utilization efficiency. In response to changes in market demand and supply chain restructuring trends, the Group has strengthened its service presence in the Asia¡VMexico, Middle East, and Red Sea markets, while flexibly deploying extra sailings during peak seasons to optimize overall capacity allocation.

As of the end of 2025, the Group operated 46 routes (excluding any chartered-out vessels), comprising 11 self-operated routes, 23 joint venture routes, 10 slot exchange routes, and 2 slot purchase routes, calling at 58 ports across approximately 22 countries and regions worldwide. The Group¡¦s operating fleet totals 41 vessels, including 37 owned ships and 4 chartered vessels, with a total capacity of 109,342 TEU. Additionally, the Group has chartered out 4 owned vessels to improve asset utilization efficiency. During 2025, no newbuildings were delivered, keeping the fleet size relatively stable. The Group enhanced operational flexibility through route adjustments and capacity optimization.

In 2025, the Group¡¦s total capital expenditure amounted to approximately US$200 million, primarily for the purchase of 13 new vessels with a combined capacity of about 93,600 TEU. These include 2 vessels of 7,000 TEU, 3 of 14,000 TEU, 6 of 5,300 TEU, and 2 of 2,900 TEU. The new ships are scheduled for delivery between 2026 and 2028. This investment will further optimize the Group¡¦s vessel type structure, enhance operational flexibility and economies of scale, while ensuring compliance with the latest environmental and regulatory requirements, thereby supporting the Group¡¦s long-term sustainable development strategy.

Strategy¡G

Buy-in Price: $8.70, Target Price: $9.60, Cut Loss Price: $8.30

|

CATL(3750)

Analysis¡G

CATL is the global leader in power batteries and energy storage systems, with high-energy-density battery cells, CTP/CTC system integration technology, green extreme manufacturing systems, and zero-carbon business models as its core strengths. In 2025, the company's Hungary plant began production, a Spanish joint venture was established, and the Indonesian industrial chain advanced, marking the transition from "Made in China" to "Global Manufacturing." Overseas joint ventures (such as Northvolt and CATL Europe) entered a profit growth phase, with overseas capacity utilization exceeding 85% and overseas revenue accounting for 40%, gradually forming a globalized profit structure. In Q1 2026, the company achieved revenue of 129.131 billion yuan, a yoy increase of 52.45%, and net profit attributable to the parent company of 20.738 billion yuan, up 48.52% yoy. Domestic power battery market share reached 47.7%, up 3.4 percentage points yoy. Recently, CATL and its affiliated capital entities announced plans to acquire Zhongheng Electric (002364.CH) and VNET (CenturyLink) for 4.1 billion and 6.4 billion yuan respectively, completing the closed-loop ecosystem of "energy storage battery cells (CATL) + HVDC power supply systems (Zhongheng Electric) + data center application scenarios (VNET)" to accelerate the cultivation of new growth curves.

Strategy¡G

Buy-in Price: $767.00, Target Price: $867.00, Cut Loss Price: $715.00

|

|

Sanhua (002050.CH) - Dual-Engine Momentum Conversion

Company ProfileSanhua is the world's largest manufacturer of HVACR controls and components, focusing on heat management business with heat pump technology as the core. It operates the domestic and commercial air conditioning business as well as automotive heat management fields, establishing a leading position in the industry. The products of the Company such as electronic expansion valves of air conditioning, four-way reversing valves, solenoid valves, micro-channel heat exchangers, automotive electronic expansion valves, new energy vehicle heat management integrated components and omega pumps have the highest market share across the world. The market proportion of service valves, thermostatic expansion valves for vehicles and receivers rank top among the world. Investment SummaryCore Business Maintained High Growth, Profitability Improved

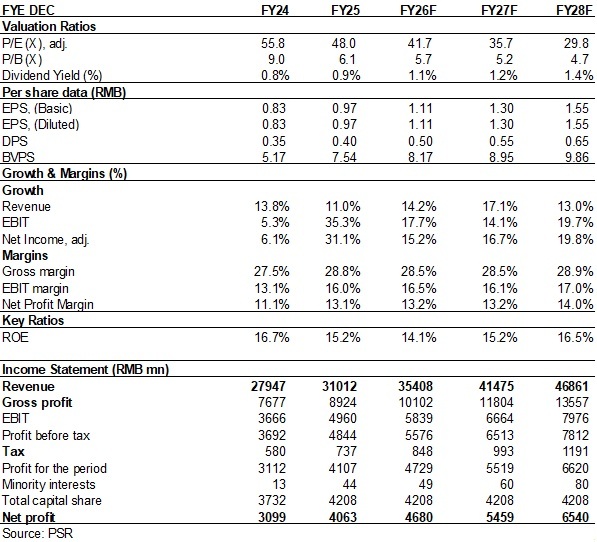

FY2025 full-year results: The Company reported revenue of RMB31,012 million (RMB, the same below), up 10.97% yoy; net profit attributable to the parent company of RMB4,063 million, up 31.10% yoy; and gross margin of 28.8%, up 1.4 ppts yoy. The Company adopted a raw material price linkage mechanism and hedging measures to reduce costs and enhance efficiency, while continuously optimising its product mix and benefiting from economies of scale, driving an improvement in profitability. In terms of business structure, revenue from refrigeration and air-conditioning electrical appliance components amounted to RMB18,585 million (accounting for 59.93%), up 12.22% yoy; revenue from automotive components amounted to RMB12,427 million (accounting for 40.07%), up 9.14% yoy. FY2026 Q1 results: Revenue amounted to RMB7,774 million, up slightly by 1.36% yoy; net profit attributable to the parent company was RMB928 million, up 2.68% yoy; and net profit excluding non-recurring items was RMB986 million, up 15.52% yoy. Gross margin was 27.8%, up 1.0 ppt yoy. Although growth was moderate, after adding back foreign exchange losses of RMB140-150 million and securities investment losses of RMB100 million, adjusted net profit grew by more than 30% yoy, with net profit margin rising to 14.6%. This reflects that despite the challenge of rising raw material costs caused by the situation in the Middle East in Q1, the Company still achieved solid results growth. Refrigeration Business Foundation Remained Solid, Liquid Cooling and Energy Storage Demand Was StrongIn 2025, revenue from the refrigeration components business grew against the trend, despite a 1.2% decline in total domestic air-conditioner industry sales volume. This was mainly attributable to the steady increase in market share and product mix optimisation. The segment's gross margin was 28.8%, up 1.42 ppts yoy. Notably, the Company's annual sales from liquid cooling and energy storage businesses reached RMB2 billion, among which revenue from data centre liquid cooling doubled. In 2026 Q1, despite a 3% yoy decline in domestic air-conditioner sales volume, the Company achieved steady revenue growth by expanding its data centre liquid cooling business and new application scenarios for energy storage thermal management. Based on strong demand, the Company maintained its full-year guidance of high growth of 50%-100% for data centre and energy storage-related businesses. Refined Operations in Automotive Components BusinessIn 2025, the gross margin of the automotive components business segment increased by 1.15 ppts to 28.8%, reflecting the strategic results of the Company's shift from scale expansion to refined operations. In 2026 Q1, although NEV sales volume declined by 3.7% yoy, the Company's core customer Tesla recorded a 13% yoy increase in global production in Q1, the proportion of domestic emerging automaker customers increased, and exports of domestic brands grew rapidly, jointly driving the Company's automotive components business growth to outperform the industry average. Moreover, the Company's automotive thermal management business is transforming and upgrading from component supply to system integration, which helps increase the value of products per vehicle, product value-added and overall competitiveness. Cost Reduction and Efficiency Enhancement Delivered Significant ResultsIn 2025 H2, the Company adjusted its strategy and refocused on operational improvements. Through measures such as digital transformation and upgrades, the introduction of AI and digital employee tools, and the optimisation of operational efficiency at overseas bases, the Company improved its operational efficiency. In 2025 and 2026 Q1, the period expense ratios (sales + administration expense ratios) decreased by 0.65 ppts and 0.88 ppts yoy to 13.01% and 11.69%, respectively, with economies of scale continuing to emerge. Liquid Cooling Contributes Short-Term Certain Incremental Growth, While Robotics Opens Up a Hundred-Billion-Level Growth SpaceThe Company has entered the liquid cooling and energy storage sectors as a thermal management component supplier, with core products covering valves, pumps, heat exchangers and sensors. The common architecture of thermal management technology across the three major scenarios of automobiles, robotics and AI servers gives the Company the ability to reuse its technology for "one core and three applications". Its R&D investment efficiency is significantly higher than that of single-track companies, with a high self-production rate, more mature products and a clear platform-based expansion path. It has currently reached cooperation with several leading thermal management integrators. Among them, Tesla's HW4.0 valve island product has secured a nomination and entered the batch delivery stage, while AI server liquid cooling has reached cooperation with leading domestic cloud vendors, entered the prototype testing stage, and is expected to achieve small-scale mass production within the year. Short-term growth certainty in the liquid cooling segment is promising. In the robotics field, the Company has entered the biomimetic robot market as an electromechanical actuator supplier, actively cooperating with customers in product R&D, trial production and iteration, while stepping up joint development efforts. At the same time, it is strengthening its technology reserves and capacity layout in parallel, and has launched the construction of a RMB3.8 billion robotics production base, laying the foundation for future profit growth. Investment ThesisSanhua Intelligent Controls is a leader in refrigeration components. As global NEV penetration remains on an upward trend, the Company's technical barriers and customer advantages remain solid, and its market share is expected to continue increasing. Its automotive components business is expected to maintain a double-digit CAGR over the next three years, while the liquid cooling and energy storage businesses have relatively high certainty of sustaining high growth. In the long term, the potential space in the robotics track is expected to reshape the Company's valuation logic. As for valuation, we expected the Company's 2026/2027/2028 earnings per share to 1.11/1.30/1.55 yuan, a yoy increase of 15.2%/16.7%/19.8%. And we accordingly gave the target price to RMB53.4, respectively 48/41.2/34.4x P/E for 2026/2027/2028. "Accumulate" rating. (Closing price as at 29 May) RiskProgress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices Financials

(Closing price as at 29 May 2026) Download PDF Version

| Recommendation on 3-6-2026 | | Recommendation | Accumulate (Maintain) | | Price on Recommendation Date | $ 46.340 | | Suggested purchase price | N/A | | Target Price | $ 53.400 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|