|

JD INDUSTRIALS(7618)

Analysis¡G

JD Industrial announced its first-quarter 2026 results. Revenue for the period reached RMB 5.658 billion, representing a 25.3% year-on-year increase. Profit amounted to RMB 185 million, up 45% year-on-year. Non-IFRS net profit was RMB 229 million, growing 54.4%. The Group also announced that the Board has authorized and approved a share repurchase program, allowing the company to buy back up to US$200 million worth of shares in the open market over a 24-month period starting from the approval date.As a leading industrial supply chain technology and service provider, JD Industrial enhances efficiency through ¡§Digital Intelligence¡¨ (digital and intelligent technologies) and ensures reliable delivery through its ¡§Physical¡¨ network (goods and fulfillment infrastructure). By integrating digital and physical elements, the Group promotes coordinated and seamless operations across all links in the industrial supply chain.

In terms of industry services, the Group focuses on four major sectors ¡X manufacturing, transportation, energy, and comprehensive industries ¡X leveraging its strengths in supply chain infrastructure and digital intelligence technologies to continuously develop scenario-based solutions. In customer collaboration and service enhancement, the Group extends its end-to-end digital intelligence infrastructure into clients¡¦ internal operations, working closely with them on top-level procurement strategy planning and full-chain system development to drive the implementation of digital intelligence capabilities across various business scenarios. In its service model, the Group remains customer-centric and continues to build a comprehensive end-to-end industrial supply chain service system. Through sustained investment and optimization in key areas such as product governance, procurement cost reduction, fulfillment optimization, and operational efficiency improvement, it is gradually becoming a co-builder of partners¡¦ digital intelligence transformation and an enabler of supply chain capabilities.

In the first quarter of 2026, JD Industrial continued to strengthen its industrial supply chain product capabilities and deepened strategic cooperation with leading suppliers such as SATA Tools, 3M China, and Linde (China) Forklift Truck. By further integrating industry chain resources and expanding product categories to create sales synergies, the Group drove accelerated year-on-year revenue growth from key enterprise clients. At the same time, it leveraged its advantages to promote standardization of industrial products and simultaneously launched an industrial goods price index. This price index, based on the JoyIndustrial large language model, provides enterprises with authentic, credible, and publicly verifiable price reference benchmarks for industrial procurement, helping companies ensure compliance and improve operational efficiency. Furthermore, to address major pain points in industrial products such as non-standardized parameters, long-tail items, and information asymmetry on both supply and demand sides, the Group has continued to strengthen its full-chain AI technology capabilities. It has launched nearly 40 AI agents, serving over 3,000 key enterprise clients. AI technology is now widely applied in areas such as product recognition, intelligent matching, batch ordering, and precise customer demand forecasting. Through driving Mercator product capability development, AI also helps clients build standardized product libraries and further improves product standardization levels. In addition, AI has significantly enhanced manpower efficiency in core positions such as procurement, sales, and product management. AI technology has been comprehensively applied across multiple business scenarios, achieving operational efficiency optimization and commercial value realization.(I do not hold the above stock.)

Strategy¡G

Buy-in Price: $15.50, Target Price: $17.00-18.60, Cut Loss Price: $14.70

|

Jinxun Resource(3636)

Analysis¡G

Jinxun Resource is a mining trading company specializing in non-ferrous metal ore trading. The company is primarily engaged in both domestic and international trade of non-ferrous metal ores, having developed a trading system centered on copper concentrate, while also trading zinc concentrate, lead concentrate, and other varieties. Over the past three years, the company has achieved explosive growth, with revenue increasing by 236% and net profit surging more than tenfold, reflecting a significant improvement in profitability. Its net profit margin rose from 4.31% to 14.48%, indicating a substantial enhancement in operating efficiency. Peru¡¦s energy crisis law took effect on May 11, prioritizing residential electricity use while placing industrial and mining power at the lowest priority. Although this has not yet impacted mining operations, Peru is the world¡¦s second-largest copper-producing country, and concerns over supply-side disruptions remain elevated. The three-month copper futures contract on the London Metal Exchange (LME) briefly hit a high of $14,106.50 per tonne. The market is facing an imminent supply crisis, with growing concerns that disruptions to sulfuric acid supplies in the Persian Gulf could affect copper supply. We believe that Jinxun Resource, as a leader in the niche field of low-grade copper smelting, leverages its technological advantages and geographic positioning to demonstrate strong growth potential amid the copper industry¡¦s cyclical upturn. Its current valuation is below the industry average, leaving room for further upside.

Strategy¡G

Buy-in Price: $24.50, Target Price: $27.30, Cut Loss Price: $22.84

|

|

POP MART (9992.HK) - Concentration and operating cost concerns emerge

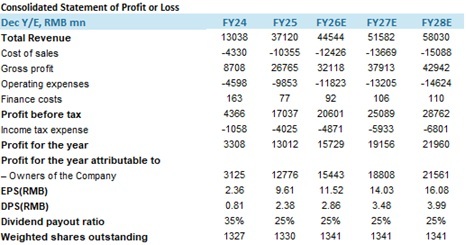

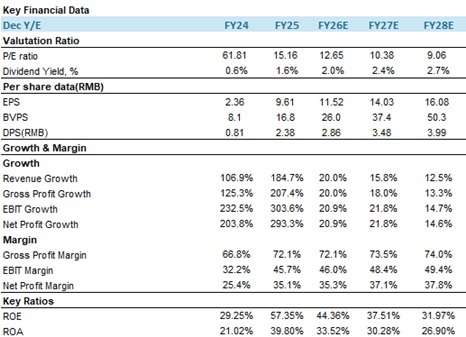

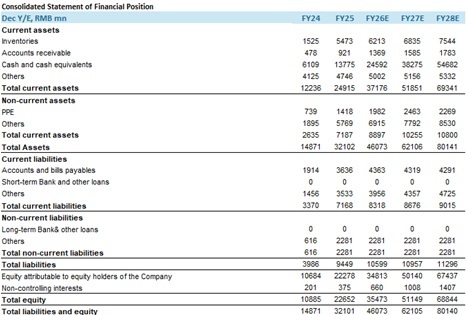

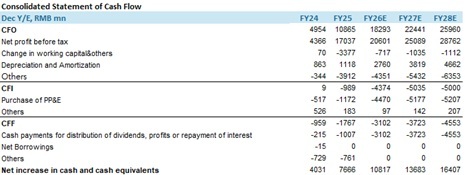

OverviewPOP MART is primarily engaged in the design and development of trendy toys. It operates a comprehensive platform covering the entire industry chain of intellectual property (IP) for trendy toys, with businesses including IP incubation and operation, trendy toys and retail, theme park and experiences, and digital entertainment. The company's products include blind boxes, figurines, ball-jointed dolls (BJD), MEGA, plush toys, and derivatives, among others. Its self-developed products primarily feature artist-owned IPs such as THE MONSTERS, MOLLY, SKULLPANDA, and CRYBABY, as well as licensed IPs, which are sold in both domestic and international markets. High Margin Rivals Luxury Goods, but IP Concentration and Heavy-Asset Expansion Pose RisksIn 2025, the company achieved operating revenue of RMB 37.12 billion with a substantial year-on-year increase of 185%. Overseas sales accounted for 44% of total revenue, indicating that international markets have become a core growth engine. By product category, plush toys contributed 50.4% of revenue, surging 560.6% year-on-year. Centralized procurement effectively compressed costs, supporting profit release. Gross profit for the year reached RMB 26.76 billion, up 207% year-on-year, outpacing revenue growth. The gross margin stood at 72.1% with an increase of 5.3 percentage points. This margin rivals that of luxury goods (typically 60%-80%) and significantly exceeds conventional product pricing logic, reflecting strong pricing power driven by popular IPs and emotional value. In terms of IP structure, artist IPs generated 90% of revenue, with The Monsters contributing over RMB 14 billion, or 38% of total revenue. This highlights heavy dependence on hit IPs such as Labubu, SkullPanda, Molly, DIMOO, and Twinkle Twinkle. Should the company fail to continuously create new blockbuster IPs, a decline in the popularity of core IPs would put downward pressure on revenue. On the expense side, distribution and selling expenses for 2025 totaled RMB 8.08 billion, up 121% year-on-year. Within that, commissions and e-commerce platform service fees were RMB 1.44 billion (+134%), advertising and marketing expenses were RMB 1.19 billion (+110%). While promotion and customer acquisition costs were gradually diluted as revenue grew, short-term lease and variable lease-related expenses reached RMB 1.34 billion (+192%), and transportation and logistics expenses reached RMB 2.043 billion (+276%). These increases indicate simultaneous expansion of stores, headcounts, and logistics systems, raising fixed operating costs -- necessary for revenue growth, but also a double-edged sword: if IP sales weaken, the heavy-asset nature makes it difficult to scale back costs quickly, thereby hurting profits. General and administrative expenses were RMB 1.77 billion (+87%), significantly below revenue growth, demonstrating that the company had achieved economies of scale and built certain industry barriers. City Theme Park Upgrade Exceeds Expectations, IP Omni-Scene Ecosystem AcceleratesPop Mart's City Theme Park, a core offline IP ecosystem venue, recently saw major progress: part of the upgraded area has been completed, with 70% of new content opened early to the public on April 30 (ahead of the May Day holiday). The remaining landscape construction is expected to be fully completed by late July to early August. The park's first full operating year (2024) was already profitable, as the company prioritizes long-term refinement over short-term returns. Notably, even when only about one-third of the area was open, visitor traffic increased significantly, with non-family and non-local visitors each accounting for more than half. The concurrent expansion of "popop" accessory stores (in Beijing and Shanghai) and the independent dessert brand "POP BAKERY" (over 10 pop-up events in multiple cities) further enriches the IP consumption scene matrix, collectively building an immersive themed experience. Venturing into Small Home Appliances: High Premium, Weak StabilityLeveraging its IPs, Pop Mart has entered the small home appliance sector with an initial product line covering five categories, including the LABUBU refrigerator. Adopting an OEM asset-light model, the company plans to first establish a foothold in mainland China before expanding overseas. The LABUBU refrigerator, limited to 999 units globally and priced at RMB 5,999, garnered over 47,000 pre-orders before launch. Its secondary market price once surged to RMB 20,000 but later retreated; after a second batch sold out quickly, some units were resold below the original price. This reflects high emotional premium elasticity but weak stability. The home appliance industry's gross margin is significantly lower than the company's 72.1% overall margin, so near-term earnings contribution is expected to be limited. The long-term strategic rationale is to extend IPs into high-frequency scenarios. Home appliances are functional goods, with quality control and after-sales requirements far exceeding those of blind boxes; failure to meet practical standards could undermine IP trust. While a limited-quantity strategy remains effective in the short term, whether consumers can transition from impulse buying to pragmatic repeat purchases remains to be seen. Valuation and Investment RecommendationsAs China's leading pop toy company, Pop Mart has the capability to cover the entire IP value chain, precisely capturing market demand for emotional consumption while continuously building a diversified IP matrix. The company's 2025 revenue surged, gross margin rivaled luxury goods, overseas and plush product segments drove strong growth, and scale effects are evident. However, IP concentration, heavy-asset expansion, and the quality control and repurchase risks of cross-sector home appliances coexist. We believe the company's share price will depend on the stability of new IP incubation and new scenario profitability. We project revenue for 2026¡V2028 at RMB 44.54 billion, RMB 51.58 billion, and RMB 58.03 billion respectively, with EPS of RMB 11.52 / 14.03 / 16.08. We downgrade the rating to Neutral, with a target price of HKD 158.9, corresponding to 12x forecast 2026 P/E. Risk factors1) Macroeconomic downturn impacting end-consumer spending;

2) The company's overseas expansion falling short of expectations;

3) Weakening appeal of IPs/products;

4) Intensifying industry competition. FinancialCurrent Price as of: 11 May

Exchange rate: HKD/RMB = 0.87

Source: PSHK Est. Download PDF Version

| Recommendation on 14-5-2026 | | Recommendation | Neutral | | Price on Recommendation Date | $ 167.400 | | Suggested purchase price | N/A | | Target Price | $ 158.900 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|