|

JACOBIO-B(1167)

Analysis¡G

Jacobio Pharma is an innovation-driven clinical-stage biopharmaceutical company committed to developing breakthrough cancer therapies for global patients. Its R&D strategy focuses on key oncology signaling pathways such as KRAS, STING, p53, and MYC. The company¡¦s research pipeline centers on tumor-targeted therapies and tumor immunotherapy, with core projects aiming to be among the global top three in their respective categories.

The Group¡¦s laboratories are located in Beijing, Shanghai, and Boston. It possesses proprietary platforms including the Induced Allosteric Drug Discovery Platform (IADDP) and tADC/iADC platforms that use targeted drugs and immune recruiters (Recruitor) as payloads. Leveraging these self-established platforms, the Group has built a differentiated and globally competitive product pipeline, consisting of seven clinical-stage assets, three assets in the IND approval stage, and several other assets awaiting IND initiation. These candidate drugs target previously ¡§undruggable¡¨ targets, with particular emphasis on RAS signaling. They offer broad applicability across multiple tumor types and show strong potential for use in combination therapies.

Among all clinical-stage candidates, the Group¡¦s leading asset Iruikai (glesirasib, KRAS G12C inhibitor) has been approved by the National Medical Products Administration (NMPA) and was launched in May 2025. It was subsequently included in the National Reimbursement Drug List (NRDL) in December 2025. On August 30, 2024, the Group entered into an out-licensing agreement with Allist Pharmaceuticals, granting Allist rights to develop Iruikai and sitneprotafib in Greater China, while Jacobio retains development rights outside of China. The company is currently seeking advice on the registration pathway with the U.S. FDA. Allist has been actively advancing sales and market expansion for Iruikai and achieved solid sales performance in the second half of 2025.

The Group¡¦s non-wholly owned subsidiary, Beijing Jacobio, entered into a licensing and collaboration agreement with AstraZeneca to jointly develop and commercialize the pan-KRAS inhibitor JAB-23E73. Under this agreement, AstraZeneca is granted an exclusive license for the research, development, registration, manufacturing, and commercialization of JAB-23E73 worldwide, excluding mainland China, Hong Kong SAR, Macau SAR, and Taiwan. AstraZeneca will bear all subsequent development and commercialization costs and activities. In March this year, the Group received an upfront payment of US$100 million from AstraZeneca. The receipt of this payment has further strengthened the Group¡¦s cash reserves and will provide strong support for the continued advancement of its innovative oncology pipeline.(I do not hold the above stock)

Strategy¡G

Buy-in Price: $7.80, Target Price: $8.80, Cut Loss Price: $7.40

|

Laopu Gold(6181)

Analysis¡G

Laopu Gold recently posted job openings on recruitment platforms for in‑store customer service manager positions in Beijing, Shanghai, Hangzhou, and other cities. These roles require candidates to have at least six years of flight attendant experience with an airline, including more than three years as a purser. Laopu Gold has also set a high bar for the recruitment of store sales positions. For example, in July 2025, candidates for related roles had to go through multiple rounds of interviews, with personal image, temperament, and approachability being important considerations alongside educational background and past experience. Overall, Laopu Gold is continuously optimizing its store‑level service team and strengthening its ability to serve high‑net‑worth clients. For Q1 2026, the company expects to achieve sales (revenue including tax) of approximately RMB 19.0¡V20.0 billion, revenue of around RMB 16.5¡V17.5 billion, and net profit of about RMB 3.6¡V3.8 billion. The net profit for Q1 alone already exceeds 70% of the full‑year net profit for 2025, demonstrating strong operational resilience. By leveraging a differentiated product positioning (Eastern aesthetics + ancient‑method gold), the company has established a moat in the traditional gold retail market. Meanwhile, store upgrades and overseas expansion have opened up new growth space. We are optimistic about the company's medium‑to‑long‑term development prospects.

Strategy¡G

Buy-in Price: $673.00, Target Price: $738.50, Cut Loss Price: $630.00

|

|

LAOPU GOLD (6181.HK)

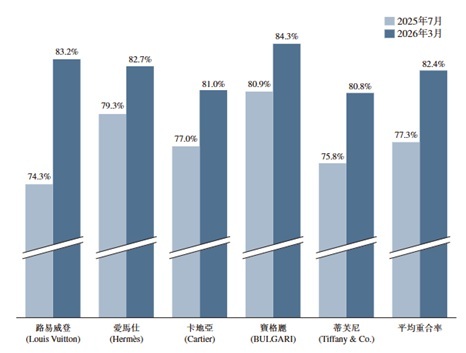

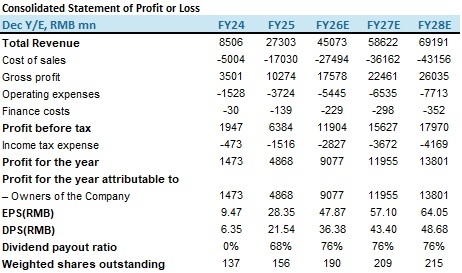

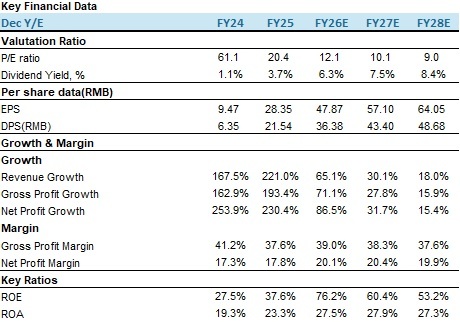

OverviewLaopu Gold (6181.HK) is the top heritage gold jewelry brand in China. Based on data of Frost & Sullivan, Laopu Gold was the first brand in the industry to introduce diamond-inlaid pure gold jewelry, leading trends for the industry. In 2025, the company's average annualized sales per shopping mall approached nearly RMB 1 billion. According to Frost & Sullivan data, among global luxury groups operating in mainland China in 2025, the company ranked first in both sales per shopping mall and sales per unit area. Strong performance growth was achieved in both the full year of 2025 and the first quarter of 2026In 2025, the company's revenue reached RMB 27.30 billion, + 221% YOY. Among this, revenue from mainland China was RMB 23.36 billion, + 205.4% YOY, accounting for 85.6% of total revenue; overseas revenue was RMB 3.94 billion, + 361% YOY, accounting for 14.4% of total revenue with an increase of 4.3 pct. Laopu Gold's first overseas store officially opened in June 2025 at Marina Bay Sands Shopping Mall in Singapore, located in a high-end luxury area. In addition, Laopu Gold has three stores in Hong Kong, including a flagship store at IFC. The company plans to further expand by opening 6--9 overseas stores in 2026 and 2027, entering markets such as Japan, North America, Australia, and the Middle East, in order to further expand its international footprint. We expect the overseas revenue share to continue climbing, contributing more significantly. Gross profit was RMB 10.27 billion, + 193.4% YOY; net profit attributable to the parent company was RMB 4.87 billion, + 230.45% YOY; EPS was RMB 28.35, + 299.4% YOY. In 2025, the company paid an interim dividend of RMB 9.59 per share and a final dividend of RMB 11.95 per share, resulting in a full-year dividend payout ratio of 76%. The above growth was mainly driven by brand advantages, product update, and store expansion (10 new stores added and 9 optimized in 2025). For the first quarter of 2026, the company expects to achieve sales (revenue including tax) of approximately RMB 19.0--20.0 billion, revenue of approximately RMB 16.5--17.5 billion, and net profit of approximately RMB 3.6--3.8 billion. As of the end of 2025, the company's total assets reached RMB 21.25 billion, + 235.4% YOY; total liabilities were RMB 10.16 billion; the asset-liability ratio stood at 47.8% with an increase of 9.5 pct YOY, mainly due to continuous store expansion and increased demand for gold raw material procurement, which drove up the scale of borrowings. Shareholders' equity was RMB 11.10 billion, + 183% YOY, reflecting a significant increase in owners' equity and further strengthening of the company's capital base. Cash and bank balances amounted to RMB 2.07 billion, + 252.3% YOY, indicating a substantial enhancement in cash reserves. Inventory was RMB 16.04 billion, covering raw materials, work in progress, and finished goods, + 292.5% YOY, primarily due to stockpiling in preparation for expected sales growth during the peak Spring Festival season. As a result, inventory turnover days extended from 195 days in the same period last year to 216 days. Accounts payable, other payables, and accrued expenses + 178.7% and 581.2% YOY respectively, reflecting the company's strong ability to occupy funds from upstream suppliers and downstream customers, highlighting its advantage in trade credit utilization, which helps free up its own funds for operating activities such as R&D investment and store expansion. Unfazed by gold price fluctuations, Laopu's luxury status has been further consolidatedSince the beginning of 2026, intensifying geopolitical conflicts and a tightening global security situation have led to sharp fluctuations in gold price, which once fell from USD 5,500 per ounce to USD 4,500 per ounce. Against this backdrop, the company's performance in Q1 2026 rose against the trend, with net profit for the quarter exceeding 70% of its full-year 2025 net profit, demonstrating strong operational resilience. The company has been listed on the Hurun Best of the Best for four consecutive years from 2023 to 2026, and in 2026 ranked among the top three jewelry brands most favored by China's high-net-worth individuals, being the only Chinese brand on the list. According to Frost & Sullivan, in 2025 the company ranked second among global luxury brands in mainland China by revenue and was the only Chinese brand among the top five. The overlap rate of its consumers with five major international luxury brands such as LV and Hermès increased from 77.3% (July 2025) to 82.4% (March 2026), continuously validating its high-end positioning. A Rothschild report noted that Laopu Gold, with its unique positioning of "integrating ancient craftsmanship with luxury fashion," has become an industry disruptor, achieving breakthroughs that other brands have not. The institution believes that the company surpassed the China jewelry business of Richemont Group in the second half of 2025. Richemont is one of the world's three largest luxury goods groups, with its jewelry business including Cartier, Van Cleef & Arpels, and Buccellati. Laopu Gold has approximately 610,000 loyal members, a net increase of 260,000 (or 74.3%) from the end of 2024, with its consumer base continuing to expand. While gold's high value-retention attribute certainly enhances the products, Laopu Gold's core competitiveness that distinguishes it from traditional gold jewelry retailers lies in its ancient method gold craftsmanship, brand influence, and strong luxury attributes. Figure 1: Gold price

Resources¡GWind¡APSHK Figure 2: High-end brand overlap rate

Resources¡GAnnual Report¡APSHK Investment ThesisWe believe that gold price in 2026 will show a "decline first, then rise" trend: in the first half, price will fluctuate within the range of USD 4,300--5,000 per ounce, digesting geopolitical premiums; in the second half, supported by a recovery in expectations of Fed rate cuts and continued central bank gold purchases, price will rebound to the target range of USD 5,200--5,500 per ounce. Core drivers include the evolution of the Middle East situation, the Fed's policy path, and the continued trend of central bank gold buying. Laopu Gold has carved out an independent path as an Eastern luxury brand, with low sensitivity to gold price fluctuations. In fact, higher gold price will be beneficial to its brand premium and earnings resilience. Laopu Gold's core advantage lies in its unique "cultural gold" positioning and high-growth model. Its prospects mainly depend on whether it can balance financial health and brand value amid rapid expansion. The company has built a moat in the traditional gold retail market through differentiated product positioning (Eastern aesthetics + ancient method gold) and has opened up new growth space through store upgrades and overseas expansion. We are optimistic about the company's medium-to-long-term development prospects and believe it can achieve sustainable growth while maintaining its premium brand positioning. We forecast the company's revenue for 2026--2028 to be RMB 45.07 billion, RMB 58.62 billion, and RMB 69.19 billion respectively. EPS is projected at RMB 47.87 / 57.1 / 64.05, corresponding to P/E ratios of 12.1x / 10.1x / 9.0x. Based on a target P/E of 15x for 2026, we set a target price of HKD 815.96 and upgrade the rating to "Buy". (Current price as of April 8) Risk factorsGold price fluctuations, intensified industry competition, macroeconomic recovery is weaker than expected, and store expansion is weaker than expected. Financial

Current Price as of: 08 Apr

Exchange rate: HKD/CNY = 0.88

Source: PSHK Est. Download PDF version...

| Recommendation on 16-4-2026 | | Recommendation | Buy (upgraded) | | Price on Recommendation Date | $ 657.500 | | Suggested purchase price | N/A | | Target Price | $ 815.960 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|