|

ZAI LAB(9688)

Analysis¡G

Zai Lab is an innovative global biopharmaceutical company in the commercialization stage, committed to addressing significant unmet medical needs in the fields of oncology, immunology, neuroscience, and infectious diseases through the discovery, development, and commercialization of products. The Group has substantial operations in Greater China and the United States. It currently has seven commercialized products (ZEJULA, VYVGART / VYVGART Hytrulo, NUZYRA, OPTUNE, QINLOCK,XACDURO, and AUGTYRO) that have received marketing approval in at least one region in Greater China. In addition, it has multiple projects in late-stage product development, with several key clinical studies underway in its product pipeline.

In 2025, the Group delivered strong financial performance, with total revenue increasing 15% year-over-year to US$460 million, while net loss narrowed by 32% to US$175.5 million. The revenue growth was primarily driven by increased sales of XACDURO, supported by strong patient demand and continued expansion of hospital coverage, as well as higher sales of NUZYRA, benefiting from improved market coverage and penetration. Despite the evolving competitive landscape for PARPi products in mainland China, Zejula maintained its leading position in hospital sales of PARP inhibitors for ovarian cancer in mainland China. VYVGART¡¦s revenue included a US$5.6 million rebate related to its renewal in the National Reimbursement Drug List (NRDL), while VYVGART Hytrulo¡¦s revenue included a US$2.4million rebate following a voluntary price adjustment prior to NRDL negotiations. In the fourth quarter of 2025, the National Medical Products Administration (NMPA) approved AUGTYRO for the treatment of adult patients with NTRK-positive solid tumors and KarXT for the treatment of adult patients with schizophrenia.

The Group also continued to make progress across its product pipelines. For global assets, encouraging results were obtained from the global Phase I study of zoci, a DLL3-targeted ADC with first-in-class and best-in-class potential for the treatment of extensive-stage small cell lung cancer. The internally developed bispecific antibody ZL-1503 for the treatment of atopic dermatitis also yielded promising preclinical data. For the late-stage regional rights pipeline, the Group obtained positive data in 2025, including data for povetacicept in the treatment of IgA nephropathy and primary membranous nephropathy. In addition, the Group expanded and strengthened its pipeline through synergistic business development activities, including the acquisition of global exclusive rights for the development and commercialization of ZL-1311, a next-generation TCE targeting MUC17 for the treatment of gastric cancer and gastroesophageal junction cancer. In 2026, the Group expects revenue to continue growing, primarily driven by existing commercialized products as well as recently approved products or new indications expected to be launched within the year. While preparing to launch more products or new indications for existing products, the Group will strive to achieve strong financial performance and move toward profitability by improving the accessibility of its existing commercialized products and further enhancing efficiency and productivity.(I do not hold the above stock)

Strategy¡G

Buy-in Price: $16.00, Target Price: $18.00, Cut Loss Price: $15.00

|

JOHNSON ELEC H(179)

Analysis¡G

As a global leader in the micro motor industry, Johnsonelectric is extending its business from traditional automotive motor operations to two high-growth sectors¡XAI data center liquid cooling and humanoid robotics¡Xmarking the beginning of its second growth curve. The company's automotive product revenue accounts for over 80% of its total, with deep partnerships established with top-tier global clients such as Bosch, Continental, and Volkswagen. Its micro motor products maintain a long-term second-place position in the global market share, while its traditional core business remains stable. In the first half of FY26, the gross margin reached 24.0%, benefiting from cost reductions and currency hedging, leading to continuous profitability improvements. The company's new business initiatives boast significant first-mover advantages: its AI data center liquid cooling pumps have already supplied top-tier global hyperscale enterprises, being applied in NVIDIA Blackwell servers with power ranges from 18W to 1800W to meet high computational density cooling demands. In the humanoid robotics sector, Teconn Motor has formed a joint venture, "Motion Intelligence Control," with Shanghai Electromechanical, focusing on core components such as joint modules and dexterous hand actuators. As AI computing power demand surges and humanoid robotics commercialization accelerates, the company's technological expertise and customer resources will translate into substantial growth.

Strategy¡G

Buy-in Price: $24.80, Target Price: $28.60, Cut Loss Price: $22.50

|

|

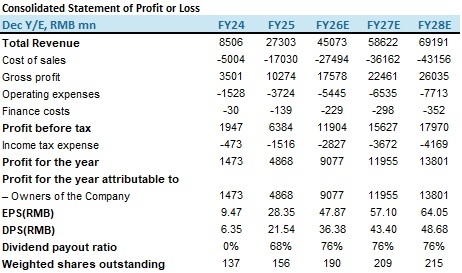

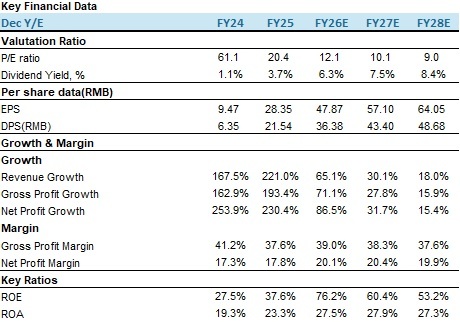

LAOPU GOLD(6181.HK) - Unfazed by gold price fluctuations, both performance and luxury status are doubly validated

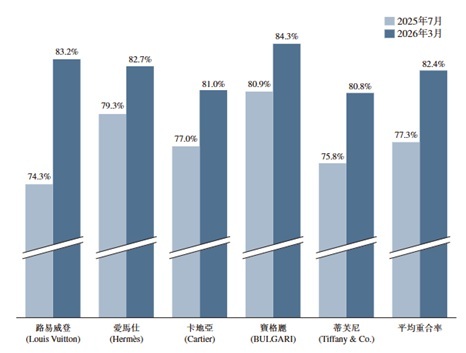

OverviewLaopu Gold (6181.HK) is the top heritage gold jewelry brand in China. Based on data of Frost & Sullivan, Laopu Gold was the first brand in the industry to introduce diamond-inlaid pure gold jewelry, leading trends for the industry. In 2025, the company's average annualized sales per shopping mall approached nearly RMB 1 billion. According to Frost & Sullivan data, among global luxury groups operating in mainland China in 2025, the company ranked first in both sales per shopping mall and sales per unit area. Strong performance growth was achieved in both the full year of 2025 and the first quarter of 2026In 2025, the company's revenue reached RMB 27.30 billion, + 221% YOY. Among this, revenue from mainland China was RMB 23.36 billion, + 205.4% YOY, accounting for 85.6% of total revenue; overseas revenue was RMB 3.94 billion, + 361% YOY, accounting for 14.4% of total revenue with an increase of 4.3 pct. Laopu Gold's first overseas store officially opened in June 2025 at Marina Bay Sands Shopping Mall in Singapore, located in a high-end luxury area. In addition, Laopu Gold has three stores in Hong Kong, including a flagship store at IFC. The company plans to further expand by opening 6--9 overseas stores in 2026 and 2027, entering markets such as Japan, North America, Australia, and the Middle East, in order to further expand its international footprint. We expect the overseas revenue share to continue climbing, contributing more significantly. Gross profit was RMB 10.27 billion, + 193.4% YOY; net profit attributable to the parent company was RMB 4.87 billion, + 230.45% YOY; EPS was RMB 28.35, + 299.4% YOY. In 2025, the company paid an interim dividend of RMB 9.59 per share and a final dividend of RMB 11.95 per share, resulting in a full-year dividend payout ratio of 76%. The above growth was mainly driven by brand advantages, product update, and store expansion (10 new stores added and 9 optimized in 2025). For the first quarter of 2026, the company expects to achieve sales (revenue including tax) of approximately RMB 19.0--20.0 billion, revenue of approximately RMB 16.5--17.5 billion, and net profit of approximately RMB 3.6--3.8 billion. As of the end of 2025, the company's total assets reached RMB 21.25 billion, + 235.4% YOY; total liabilities were RMB 10.16 billion; the asset-liability ratio stood at 47.8% with an increase of 9.5 pct YOY, mainly due to continuous store expansion and increased demand for gold raw material procurement, which drove up the scale of borrowings. Shareholders' equity was RMB 11.10 billion, + 183% YOY, reflecting a significant increase in owners' equity and further strengthening of the company's capital base. Cash and bank balances amounted to RMB 2.07 billion, + 252.3% YOY, indicating a substantial enhancement in cash reserves. Inventory was RMB 16.04 billion, covering raw materials, work in progress, and finished goods, + 292.5% YOY, primarily due to stockpiling in preparation for expected sales growth during the peak Spring Festival season. As a result, inventory turnover days extended from 195 days in the same period last year to 216 days. Accounts payable, other payables, and accrued expenses + 178.7% and 581.2% YOY respectively, reflecting the company's strong ability to occupy funds from upstream suppliers and downstream customers, highlighting its advantage in trade credit utilization, which helps free up its own funds for operating activities such as R&D investment and store expansion. Unfazed by gold price fluctuations, Laopu's luxury status has been further consolidatedSince the beginning of 2026, intensifying geopolitical conflicts and a tightening global security situation have led to sharp fluctuations in gold price, which once fell from USD 5,500 per ounce to USD 4,500 per ounce. Against this backdrop, the company's performance in Q1 2026 rose against the trend, with net profit for the quarter exceeding 70% of its full-year 2025 net profit, demonstrating strong operational resilience. The company has been listed on the Hurun Best of the Best for four consecutive years from 2023 to 2026, and in 2026 ranked among the top three jewelry brands most favored by China's high-net-worth individuals, being the only Chinese brand on the list. According to Frost & Sullivan, in 2025 the company ranked second among global luxury brands in mainland China by revenue and was the only Chinese brand among the top five. The overlap rate of its consumers with five major international luxury brands such as LV and Hermès increased from 77.3% (July 2025) to 82.4% (March 2026), continuously validating its high-end positioning. A Rothschild report noted that Laopu Gold, with its unique positioning of "integrating ancient craftsmanship with luxury fashion," has become an industry disruptor, achieving breakthroughs that other brands have not. The institution believes that the company surpassed the China jewelry business of Richemont Group in the second half of 2025. Richemont is one of the world's three largest luxury goods groups, with its jewelry business including Cartier, Van Cleef & Arpels, and Buccellati. Laopu Gold has approximately 610,000 loyal members, a net increase of 260,000 (or 74.3%) from the end of 2024, with its consumer base continuing to expand. While gold's high value-retention attribute certainly enhances the products, Laopu Gold's core competitiveness that distinguishes it from traditional gold jewelry retailers lies in its ancient method gold craftsmanship, brand influence, and strong luxury attributes. Figure 1: Gold price

Resources¡GWind¡APSHK Figure 2: High-end brand overlap rate

Resources¡GAnnual Report¡APSHK Investment ThesisWe believe that gold price in 2026 will show a "decline first, then rise" trend: in the first half, price will fluctuate within the range of USD 4,300--5,000 per ounce, digesting geopolitical premiums; in the second half, supported by a recovery in expectations of Fed rate cuts and continued central bank gold purchases, price will rebound to the target range of USD 5,200--5,500 per ounce. Core drivers include the evolution of the Middle East situation, the Fed's policy path, and the continued trend of central bank gold buying. Laopu Gold has carved out an independent path as an Eastern luxury brand, with low sensitivity to gold price fluctuations. In fact, higher gold price will be beneficial to its brand premium and earnings resilience. Laopu Gold's core advantage lies in its unique "cultural gold" positioning and high-growth model. Its prospects mainly depend on whether it can balance financial health and brand value amid rapid expansion. The company has built a moat in the traditional gold retail market through differentiated product positioning (Eastern aesthetics + ancient method gold) and has opened up new growth space through store upgrades and overseas expansion. We are optimistic about the company's medium-to-long-term development prospects and believe it can achieve sustainable growth while maintaining its premium brand positioning. We forecast the company's revenue for 2026--2028 to be RMB 45.07 billion, RMB 58.62 billion, and RMB 69.19 billion respectively. EPS is projected at RMB 47.87 / 57.1 / 64.05, corresponding to P/E ratios of 12.1x / 10.1x / 9.0x. Based on a target P/E of 15x for 2026, we set a target price of HKD 815.96 and upgrade the rating to "Buy". (Current price as of April 8) Risk factorsGold price fluctuations, intensified industry competition, macroeconomic recovery is weaker than expected, and store expansion is weaker than expected. Financial

Current Price as of: 08 Apr

Exchange rate: HKD/CNY = 0.88

Source: PSHK Est. Download PDF version...

| Recommendation on 9-4-2026 | | Recommendation | Buy (upgraded) | | Price on Recommendation Date | $ 657.500 | | Suggested purchase price | N/A | | Target Price | $ 815.960 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|