|

INNOCARE(9969)

Analysis¡G

In 2025, INNOCARE achieved transformative growth. Total operating revenue reached approximately RMB 2.374 billion, representing a substantial year-on-year increase of 135.3%. Among this, revenue from drug sales amounted to RMB 1.442 billion, up 43.4%, mainly driven by strong sales growth of orelabrutinib and the new launch of tanezumab (tanximab) starting from the fourth quarter of 2025. Revenue from business collaborations reached RMB 904 million, primarily from licensing income generated under exclusive licensing agreements signed with Zenas Biopharma and Prolium. The Group recorded its first-ever full-year profit of RMB 644 million in 2025 (compared with a loss of RMB 452 million in 2024), achieving a significant milestone. This was mainly attributable to strong commercial execution, improved market penetration of its launched products, and the realization of value from strategic global business development partnerships. Gross profit margin rose to 92%, an increase of 5.7 percentage points from 86.3% in 2024, largely due to the contribution from business collaboration revenue.With multiple products either already commercialized or about to submit regulatory applications, INNOCARE has entered a new stage of diversified growth. This has not only enhanced the predictability of its profitability but also expanded its global business footprint.

According to INNOCARE¡¦s 2.0 strategy, globalization was a core strategic focus in 2025. The Group completed two milestone business expansion transactions, significantly broadening the international layout of its pipeline and its value realization pathways:

• In January 2025, the Group entered into an exclusive licensing agreement with Prolium for the development and commercialization of ICP-B02. Under this agreement, Prolium obtained exclusive rights to ICP-B02 for all non-oncology indications globally and for oncology indications outside Asia.

• In October 2025, INNOCARE reached a strategic licensing collaboration with Zenas BioPharma, granting Zenas exclusive rights to develop, manufacture, and commercialize orelabrutinib for the treatment of multiple sclerosis globally, as well as for non-oncology indications in regions outside Greater China and Southeast Asia. INNOCARE retains full rights to orelabrutinib in the global oncology field and rights for non-oncology indications in Greater China and Southeast Asia. This collaboration also grants Zenas exclusive rights to develop, manufacture, and commercialize an oral IL-17AA/AF inhibitor in regions outside Greater China and Southeast Asia, as well as exclusive global rights to develop, manufacture, and commercialize an oral, brain-penetrant TYK2 inhibitor. These transactions demonstrate the global competitiveness of the Group¡¦s innovation engine and clinical assets, while enabling it to leverage its partners¡¦ international development and commercialization capabilities. Looking ahead, globalization will remain a core pillar of the Group¡¦s strategy in 2026 and beyond. The Group will continue to focus on selective out-licensing, co-development, and regional collaborations, while maintaining its strategic focus on innovative assets, to maximize global value.

The Group¡¦s self-owned 83,000 square meter small-molecule manufacturing facility in Guangzhou complies with GMP standards of the United States, Europe, Japan, and China, and has an annual production capacity of one billion tablets. It has already successfully obtained the production license. The facility has completed Phase II and Phase III construction, adding a total of 21,541 square meters of production area. The Phase III construction will support the rapid growth of orelabrutinib and the upcoming launch of new products. In addition, the Group has established a large-molecule CMC (Chemistry, Manufacturing, and Controls) pilot facility in Changping, Beijing, intended for the operational phase of early clinical supplies. It has also selected a 70,381 square meter plot of land adjacent to its headquarters in the Beijing Life Science Park to build a landmark R&D center and large-molecule production facility.(I do not hold the above stock)

Strategy¡G

Buy-in Price: $13.00, Target Price: $14.50, Cut Loss Price: $12.20

|

CHALCO(2600)

Analysis¡G

The company is a leading enterprise in China's nonferrous metals industry, with its comprehensive strength ranking among the top in the global aluminum industry. It is also the only large-scale production and operation enterprise in China's aluminum industry that integrates the exploration and mining of resources such as bauxite and coal; the production, sales, and technological research and development of alumina, primary aluminum, and aluminum alloy products; international trade; logistics; and thermal power and new energy power generation. In 2025, the company achieved operating revenue of RMB 241.125 billion, a year-on-year increase of 1.7%; gross profit was RMB 41.454 billion, up 16.7%. Net profit attributable to shareholders was RMB 12.674 billion, an increase of 2.3%, with earnings per share of RMB 0.74. A final dividend of RMB 0.147 per share was proposed. Together with the interim dividend, the total dividend for the year was RMB 0.27 per share. On March 29, Iran announced that it had used missiles and drones to strike two aluminum plants¡XEmirates Global Aluminium and Aluminium Bahrain. Both aluminum plants confirmed that the attacks resulted in personnel injuries and property damage, and they are assessing the specific losses. In the short term, the aluminum market is significantly affected by production reductions in the Middle East, and prices are expected to remain volatile at high levels. CHALCO is in a critical period of transitioning from a traditional aluminum enterprise to a green, low-carbon, global aluminum giant, with stable long-term development prospects.

Strategy¡G

Buy-in Price: $11.60, Target Price: $13.61, Cut Loss Price: $10.64

|

|

Desay SV (002920 CH) - Deepening Deployment in Automotive Intelligence

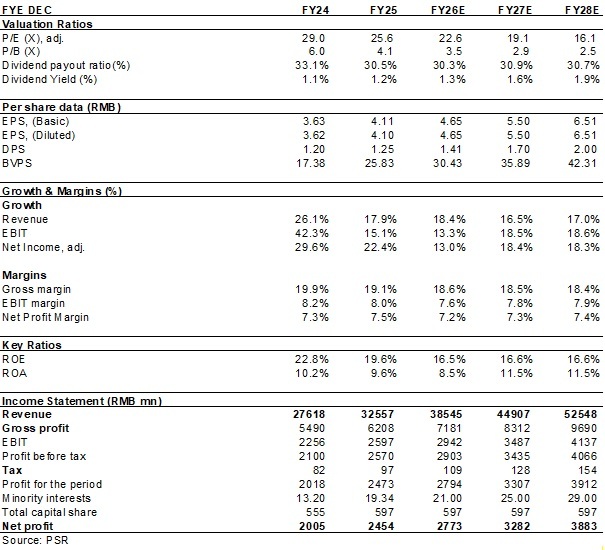

Company ProfileDesay SV, established in 1986, is a leading company in the automotive electronics field, with its main products including intelligent cockpits, intelligent driving, and connected services. Investment SummarySequential Improvement in Q4, Full-Year Results Up by Over 20%In 2025, the Company reported revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items of RMB32,557 million/RMB2,454 million/RMB2,414 million (RMB, the same below), respectively, up 17.88%/22.38%/24.05% yoy. Gross margin was 19.07%, down 0.81 ppts yoy. Net cash flow generated from operating activities reached RMB2.88 billion, up +93.1% yoy. In 2025 Q4, the Company reported quarterly revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items of RMB10,221 million/RMB666 million/RMB690 million, respectively, up 18.25%/11.34%/38.71% yoy and 32.87%/17.82%/20.72% qoq. The sequential recovery in Q4 results was mainly driven by qoq growth in sales volume from key customers such as Geely, Xiaomi and Li Auto. Deepening Deployment in Automotive IntelligenceBenefiting from the continued increase in penetration of automotive intelligent products and the significant rise in intelligent value per vehicle, the core business segments achieved strong growth in results. 1) Smart cockpit: Full-year revenue reached RMB20,585 million. Annualised sales of new project orders exceeded RMB20 billion. The Company continued to secure new project orders from major domestic and international OEMs, including Chery Automobile, Geely Auto, GAC Toyota, Li Auto, Great Wall Motor, Xiaomi Auto, XPeng Motors, Changan Automobile, VOLKSWAGEN, MERCEDES-BENZ and SKODA. 2) Intelligent driving: Full-year revenue reached RMB9.7 billion, up 32.63% yoy. Annualised sales of new project orders exceeded RMB13 billion. With the rapid adoption of intelligent driving technologies, the accelerated commercialisation of advanced functions such as urban NOA is expected to further drive high-speed growth in the Company's intelligent driving business. 3) Connected services: The Company's self-developed "Blue Whale" ecosystem achieved major breakthroughs during the reporting period. Based on AIOS, the Company comprehensively upgraded the cockpit intelligent software foundation, enabling full-stack decoupling of software and hardware and flexible adaptation across different hardware platforms and large models. It possesses full-stack AI capabilities ranging from large-model algorithms and AIOS middleware to Agent development, providing a robust full-stack software solution for the development of the AI cockpit software ecosystem. Focus on R&D, Expansion into Innovative BusinessesThe Company has consistently maintained a high level of R&D investment. In 2025, R&D expenditure reached RMB2,637 million, accounting for 8.10% of revenue. R&D personnel represented 42.40% of the Company's total workforce. The Company has established R&D centres in Singapore, Germany, Japan, and across China in Nanjing, Chengdu, Shanghai, Shenzhen, Guangzhou, Beijing, Taiwan and Changsha, ensuring sustained technological leadership and a leading position in the industry.

In terms of innovative businesses, the Company officially launched the "Chuanxing Zhiyuan" low-speed autonomous vehicle brand, expanding into a new track in last-mile logistics. Meanwhile, the Company continues to deepen industrial synergy in frontier intelligent fields, advancing in-depth cooperation and implementation with multiple embodied intelligence enterprises. It has also successfully secured designated orders for robot domain controller projects, with related products planned to achieve mass production and delivery in 2026. Steady Progress in Internationalisation StrategyIn 2025, the Company's overseas revenue increased by 41.12% to RMB2.41 billion, with its contribution rising to 7.40%, up 1.22 ppts yoy. The gross margin of overseas business was higher than that of the domestic market. In 2025, overseas gross margin reached 27.28%, up 1.34 ppts yoy and approximately 9 ppts higher than the domestic gross margin in the same period. As the internationalisation strategy continues to advance steadily, the Mexico and Indonesia plants commenced operations in 2025, while the Spain plant is expected to begin operations this year. The expansion of overseas production capacity will provide strong support for profit growth. Investment ThesisThe Company is a leader in the automotive electronics sector. Benefiting from ongoing industry development and sustained R&D investment, it maintains a technological leadership advantage while actively exploring new business opportunities. We remain firmly optimistic about the Company's long-term development prospects.

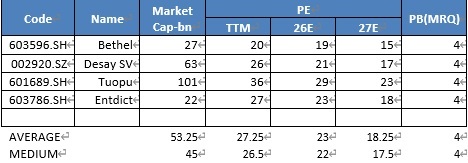

As for valuation, we expected diluted EPS of the Company to RMB 4.65/5.50/6.51 of 2026/2027/2028. And we accordingly gave the target price to RMB121, respectively 26/22/19x P/E for 2026/2027/2028. "Accumulate" rating. (Closing price as at 30 December 2026) Peer Comparison

Source: Wind, Phillip Securities Hong Kong Research

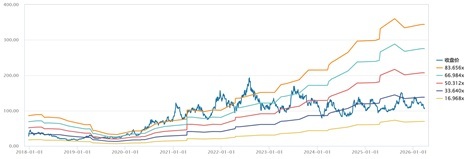

PE BAND

Source: Wind, Phillip Securities Hong Kong Research

RiskProgress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices Financials

(Closing price as at 30 March 2026)

Download PDF version...

| Recommendation on 31-3-2026 | | Recommendation | Accumulate (Downgrade) | | Price on Recommendation Date | $ 105.000 | | Suggested purchase price | N/A | | Target Price | $ 121.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|