|

361 DEGREES(1361)

Analysis¡G

361 Degrees adheres to the brand positioning of ¡§professionalization, youthfulness, and internationalization,¡¨ and is committed to providing high-value, multi-category professional sports products. The 361 Degrees brand focuses on the professional functionality of its products, with a deep emphasis on core categories such as running, basketball, and sports lifestyle. It comprehensively covers the increasingly diversified demands of the mass sports consumer group.The 361 Degrees children¡¦s brand continues the professional sports gene, positioning itself as the ¡§Youth Sports Expert.¡¨ Leveraging professional functionality, healthy technology, and child-friendly fashionable design, it creates differentiated competitive advantages and meets the comprehensive sports equipment needs of children and adolescents.

For the year ended December 31, 2025, the Group achieved revenue of RMB 11.146 billion, representing a 10.6% increase compared to 2024. Profit attributable to shareholders was RMB 1.309 billion, up 14%. Basic earnings per share were RMB 0.633. The Board recommends a final dividend of HK$0.113 per share. Together with the interim dividend of HK$0.204 per share, the total dividend for the year is HK$0.317 per share. The payout ratio remains at 45%, and the current dividend yield exceeds 5%.

As of December 31, 2025, the 361 Degrees brand had 5,394 core stores in mainland China, with an average store size of 165 square meters, an increase of 16 square meters compared to 2024. The proportion of stores in shopping malls and department stores continued to rise. By region, approximately 76.1% of the stores are located in China¡¦s third-tier and below cities, while 5.2% and 18.7% of the stores are located in first-tier and second-tier cities respectively. The physical layout of the Finnish outdoor sports brand ONEWAY in the Greater China market has begun to show results, with successful expansion to 6 stores. In the international market, the Group has accelerated its global layout, owning a total of 1,253 offline sales outlets in the Americas, Europe, and the ¡§Belt and Road¡¨ regions. At the same time, it is actively building ¡§integrated¡¨ and ¡§full-category¡¨ immersive experience 361 Degrees super stores. As of December 31, 2025, a total of 127 361 Degrees super stores have been established, of which 21 are children¡¦s super stores.

Facing increasingly diversified consumer demands, the Group is actively deepening its presence in high-potential niche segments, expanding its diverse consumer base, and extending the boundaries of its brand services. The Group places high importance on the growth vitality of the women¡¦s sports market and has launched the upgraded ¡§New Skin¡¨ series of yoga wear and the ¡§New Move¡¨ series of training equipment, while also introducing its first tennis series products. At the same time, by opening the first 361 Degrees women¡¦s sports concept store and creating offline experience scenes such as the ¡§Soft is Strength¡¨ themed yoga energy field, the Group continues to deepen the emotional connection with female consumers and builds growth momentum for future multi-category synergistic development.(I do not personally hold the above stock.)

Strategy¡G

Buy-in Price: $5.70, Target Price: $6.30, Cut Loss Price: $5.40

|

ASIA-POTASH(000893.CH)

Analysis¡G

Asia-potash is a leading domestic producer of potash fertilizer, owning a 263.3-square-kilometer potash salt mine in Khammouane Province, Laos, with estimated pure potassium chloride resources exceeding 1 billion tons, making it the enterprise with the largest potash reserves in Asia. In the first three quarters of 2025, the company achieved total operating revenue of 3.867 billion yuan, up 55.76% yoy, and net profit attributable to the parent company after non-recurring items of 1.362 billion yuan, up 164.56% yoy. The strong performance was primarily driven by the industry's upward trend. The Company's capacity expansion plan of "adding one million tons annually" is steadily progressing. The second and third 1-million-ton-per-year potash fertilizer projects have already entered the late stage of mining and construction, with an expected total capacity of 5 million tons per year. Further expansion to 7-10 million tons per year is anticipated. Looking ahead, the arrival of the potash fertilizer peak season is expected to support prices at relatively high levels. In the medium to long term, global population growth and declining per capita arable land will impose higher demands for increased crop yields and quality, leading to further emphasis on potash fertilizers. This will drive long-term demand, while supply-demand mismatches and the slowdown in new potash production capacity will likely sustain potash prices.

Strategy¡G

Buy-in Price: RMB58.90, Target Price: RMB68.00, Cut Loss Price: RMB54.00

|

|

MINISO (9896.HK) - Better-than-expected Jan-Feb same-store growth may drive a full-year Davis double play

Company OverviewMINISO is a global self-owned brand integrated retailer featuring IP design, mainly engaged in lifestyle home products and trendy toy cultural creations. Its core businesses include MINISO (value-for-money lifestyle products) and TOP TOY (trendy toys). Adopting an ¡§IP collaboration + high cost-performance¡¨ model, the Company sells through a global store network covering toys, beauty, and lifestyle products. Since opening its first store in 2013, the Company has built a retail network spanning 112 countries and regions worldwide, with more than 7,700 stores globally and over 100 million cumulative registered members. Leveraging the dual-brand matrix of MINISO and TOP TOY, the Company has achieved multi-format synergies and built significant global channel advantages and user-base barriers. Figure 1: MINISO Store

Resources: Company Website, Phillip Securities Figure 2: TOP TOY Store

Resources: Company Website, Phillip Securities Highly concentrated ownership with sound governanceMINISO¡¦s largest shareholder, Mini Investment Limited, holds 26.24%, while YYY MC Limited and YGF MC Limited hold 20.61% and 16.25%, respectively. The actual controllers are founder Ye Guofu and his wife Yang Yun, forming a stable concerted action relationship. The top ten shareholders together hold more than 80%. Overall, this forms a stable structure centered on Ye Guofu, with concerted parties controlling more than 60% of voting rights, providing strong support for the continuity of the Company¡¦s long-term strategy and governance stability. Figure 3: Shareholding Structure

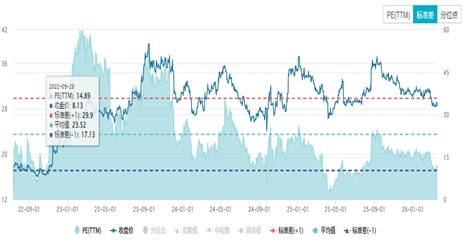

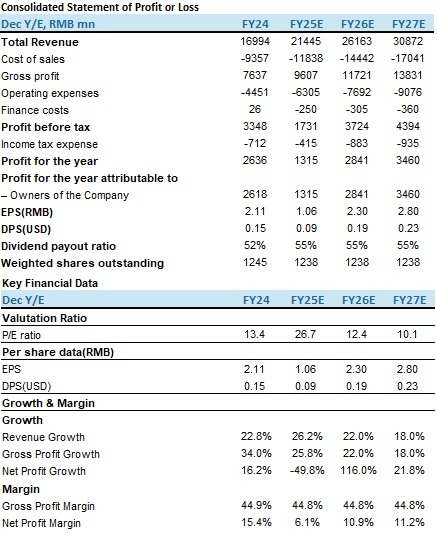

Resources: WIND, Phillip Securities Industry AnalysisLifestyle home products broadly refer to various consumer-facing household and daily-use products, covering personal care, bags and accessories, small consumer electronics, digital accessories, stationery and cultural products, leisure snacks, daily necessities, home textiles, toys, and other subcategories. According to data from Huajing Industry Research Institute, the global household goods market grew from US$655.079 billion in 2017 to US$779.094 billion in 2023, representing a CAGR of about 2.9%. As the global economy recovers, incomes rise, and consumption frequency increases, demand for household goods is expected to maintain steady growth. Guangdong Toy Association estimates that China¡¦s traditional toy market reached about RMB80.13 billion in 2025, up about 3.5% year-on-year, while China¡¦s trendy toy market reached about RMB87.97 billion, up 21% year-on-year, far outpacing traditional toys. TOP TOY is accelerating overseas expansion and in March 2025 announced a globalization strategy targeting entry into core business districts in 100 countries and more than 1,000 stores over the next five years, potentially forming the Company¡¦s second growth curve. Revenue up over 26%, Jan-Feb same-store GMV beat expectationsThe Company expects FY2025 revenue of about RMB21.44 billion, up 26% year-on-year; operating profit of about RMB3.30-3.305 billion; and adjusted operating profit of about RMB3.665-3.675 billion, mainly benefiting from product mix optimization, stronger branding, and channel expansion. Net profit is expected at about RMB1.32-1.33 billion, with the decline mainly due to: 1) about RMB740 million share of loss from Yonghui investment; 2) about RMB400 million combined impact from TOP TOY share-based compensation and fair value changes in preferred shares; and 3) about RMB190 million interest expense on stock-linked securities, of which RMB170 million is non-cash. Excluding these non-operating items, adjusted net profit is about RMB2.89-2.90 billion, up 6.2%-6.6% year-on-year. Operational momentum remained strong. In Jan-Feb 2026, domestic MINISO GMV rose over 25% year-on-year, with same-store GMV recording high-single-digit growth; U.S. market GMV rose over 50% year-on-year, with same-store GMV up over 20%; and overseas market management efficiency improved significantly. We believe these data show that the Company¡¦s IP strategy, channel optimization, and globalization capabilities are accelerating into tangible operating results, laying a solid foundation for long-term value growth. TOP TOY spin-off approaching, RMB10bn valuation anchors value realizationThe TOP TOY spin-off is approaching. In the first three quarters of 2025, TOP TOY store count reached 307, up 31% year-on-year, and revenue reached RMB1.317 billion, up 88% year-on-year. After completing Temasek strategic financing last year, its valuation has been anchored at RMB10 billion. We believe that if TOP TOY is successfully spun off while remaining a non-wholly-owned subsidiary of MINISO, it may bring multi-dimensional re-rating to the parent company through valuation premium, strategic focus, and capital-market catalysts, marking the formal value realization stage of MINISO¡¦s ¡§second growth curve.¡¨ Valuation and investment recommendationIn January-February 2026, total retail sales of consumer goods reached RMB8,607.9 billion, up 2.8% year-on-year, 1.9 percentage points faster than in December last year. On a month-on-month basis, February total retail sales of consumer goods rose 0.81%. We believe MINISO is poised to become a global leading IP-driven retail platform. As its IP matrix continues to improve and globalization deepens, brand value and market share are expected to rise further. We forecast revenue of RMB21.445 billion, RMB26.163 billion, and RMB30.872 billion in 2025-2027, with EPS of RMB1.06/2.3/2.8 and corresponding P/E of 26.7x/12.4x/10.1x. We assign a target price of HK$39.2, corresponding to 15x 2026E P/E, and maintain a Buy rating. (Current price as of 25 Mar) Figure 4: PE Curve

Resources: WIND, Phillip Securities RisksConsumption recovery falls short of expectations; intensifying industry competition and severe IP homogenization; overseas expansion risk and trade policy volatility; IP life-cycle management risk. Financial Data

(As of 25 Mar 2026)

Exchange Rate: HKD/RMB = 0.88

Source: PSHK Est. Download PDF version...

| Recommendation on 27-3-2026 | | Recommendation | Buy | | Price on Recommendation Date | $ 32.240 | | Suggested purchase price | N/A | | Target Price | $ 39.200 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|