|

U-PRESID CHINA(220)

Analysis¡G

Uni-President China has announced its annual results for the year ended December 31 last year, delivering a solid performance with both revenue and net profit reaching record highs, accompanied by strong cash flow and an extremely generous dividend policy. The Group¡¦s 2025 revenue amounted to RMB 31.714 billion, representing a year-on-year increase of 4.6%. Of this, food business revenue reached RMB 10.493 billion, up 5% and accounting for 33.1% of the Group¡¦s total revenue. Guided by its value marketing strategy, the Group combines rigorous quality control with continuous deep innovation. Through a diversified product matrix and convenient consumer experiences, it delivers a genuine ¡§value-for-money¡¨ experience to consumers.

Beverage business revenue stood at RMB 19.471 billion, an increase of 1.2%, contributing 61.4% of the Group¡¦s total revenue. The Group has actively expanded and refined its market channels to effectively cover multiple consumption scenarios, including on-the-go, catering, household, sports and gifting occasions. At the same time, it has continued to raise the proportion of high-performance terminal outlets, strengthened chilled distribution, accelerated digital empowerment, and persistently enhanced its R&D and innovation capabilities while expanding its product pipeline to adapt to evolving consumer trends, thereby supporting the long-term sustainable growth of its brands and businesses.

Gross profit rose from RMB 9.869 billion in 2024 to RMB 10.529 billion, an increase of 6.7%. The gross margin improved by 0.7 percentage points from 32.5% to 33.2%, mainly benefiting from higher production efficiency and lower prices for certain bulk raw materials. Profit attributable to shareholders reached RMB 2.05 billion, up 10.9%. Earnings per share were RMB 0.4747, with a final dividend of RMB 0.4747 (compared with RMB 0.4281 the previous year), resulting in a payout ratio of 100% and a current dividend yield of nearly 7%.

Facing structural changes in which consumption has become more rational and diversified, the Group continues to uphold its long-term philosophy and the ¡§Three Goods and One Fair¡¨ principle ¡X good quality, good credibility, good service and fair pricing. Through value marketing and digital empowerment, while maintaining price stability and healthy channel conditions, it is deepening market penetration and building stronger brand barriers.(I do not hold the above stock.)

Strategy¡G

Buy-in Price: $8.10, Target Price: $8.90, Cut Loss Price: $7.70

|

Chicmax(2145)

Analysis¡G

In 2025, China's cosmetics retail sales reached 822.53 billion yuan, representing a year-on-year increase of 6.2%. Among this, online channels accounted for 56.9% of the market share, up by 1.6 percentage points compared to 2024. In the same year, domestic-brand cosmetics recorded retail sales of 468.84 billion yuan, a year-on-year growth of 8.64%, capturing a market share of 57%. Meanwhile, foreign-brand cosmetics achieved retail sales of 353.69 billion yuan, growing by 3.09% year-on-year, holding a 43% market share. In January, 33 brands surpassed 100 million yuan in GMV, marking a 10% increase in the number of such brands compared to December. Among them, Kans led the rankings for the second consecutive month with a GMV exceeding 300 million yuan. As a leading player in the domestic cosmetics industry, Shanghai Chicmax is currently reaping the benefits of its multi-brand strategy. The company's competitive edge lies in its strong presence on the Douyin platform, the synergistic effects of its diverse brand portfolio, and its robust product innovation capabilities. Looking ahead, in the short term, the company is poised to benefit from channel optimization and the rapid growth of its sub-brands. In the medium to long term, it is expected to achieve sustained growth through global expansion and the establishment of technological barriers.

Strategy¡G

Buy-in Price: $60.40, Target Price: $68.60, Cut Loss Price: $56.50

|

|

JOYSON Electronics (600699 CH) ¡V Expanding into Robotics to Build a Second Growth Curve

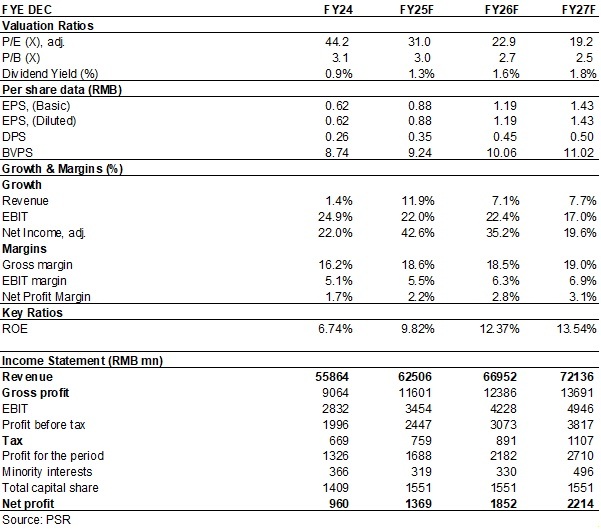

Company ProfileAs a leading global supplier in automotive electronics and automotive safety, Joyson Electronics provides one-stop solutions in key technology areas of intelligent electric vehicles to global OEMs. The Company's business is divided into two major segments: automotive electronics and automotive safety. The automotive electronics segment mainly includes intelligent cockpit, intelligent connectivity, intelligent driving and new energy management, while the automotive safety segment mainly includes products related to seatbelts, airbags, intelligent steering wheels and integrated safety solutions. In 2025, the Company strategically extended into the upstream and downstream of the robotics industry chain, newly positioning itself as "Automotive + Robotics Tier1" and actively building a second growth curve. Investment SummaryThe Company Released Its 2025 Earnings Forecast: Core Profit up 17%It is expected that in 2025 the Company will realise net profit attributable to owners of the parent company of approximately RMB1.35 billion (RMB, the same below), up 40.56% yoy; net profit attributable to the parent company excluding non-recurring items is expected to be approximately RMB1.5 billion, up approximately 17.02% yoy. The difference between the two is mainly due to non-recurring losses of approximately RMB160 million arising from the transfer of the weighing apparatus business by the Company's listed subsidiary Guangdong Xiangshan Weighing Apparatus Group Co., Ltd. (002870.CH), as well as the optimisation and disposal of certain overseas factories. The Company attributes the growth in results to the gradual effectiveness of various profitability improvement and business integration measures implemented across global business regions in 2025, as well as the continued recovery in profitability of overseas operations. Profitability of Core Businesses Continued to ImproveThrough optimising and integrating its global operations, particularly achieving notable results in reducing global raw material costs and improving operational efficiency, the Company has significantly enhanced its operating performance and profitability. The Company's overall gross margin increased from 11.1% in 2022 to 14.5% in 2023, further rising to 16.2% in 2024, and continued to increase to 18.31% as of the third quarter of 2025. From a regional perspective, overseas markets have focused on continuously reducing raw material costs by introducing Chinese suppliers and optimising procurement prices from existing suppliers. Meanwhile, the Company's global operational improvement team has continued to optimise and enhance OEE (Overall Equipment Effectiveness) at overseas factories, while adjusting and relocating production capacity from high-cost countries/regions to low-cost countries/regions, thereby steadily driving gross margin improvement. In particular, cost improvement measures in the European region were implemented earlier and achieved significant gross margin enhancement during the reporting period. Cost improvement measures in the Americas were implemented relatively later, and gross margin is expected to improve correspondingly in the future, with profitability continuing to strengthen. Sufficient Orders on Hand with Sustainable Growth Potential in Core BusinessesIn the third quarter of 2025, the Company secured new orders with a total full lifecycle amount of approximately RMB40.2 billion. In the first three quarters, the Company's cumulative global newly secured orders reached approximately RMB71.4 billion in total full lifecycle amount, of which approximately RMB39.6 billion was from the automotive safety segment and approximately RMB31.8 billion was from the automotive electronics segment. According to Frost & Sullivan, in 2024 the Company's market share in automotive safety products ranked second globally, with global and China market shares of 22.9% and 26.1%, respectively. It is estimated that by 2029, the global and domestic market sizes of the automotive passive safety industry will grow to RMB213.6 billion and RMB49.7 billion, respectively, representing CAGR of 5.4% and 7.8%, respectively, from 2025. It is further expected that by 2029, the global and China automotive electronics market sizes will reach RMB3,330.3 billion and RMB1,892.6 billion, respectively, representing CAGR of 5.8% and 9.4%, respectively, from 2025. In H1 2025, the automotive safety and automotive electronics segments accounted for 62.53% and 27.53% of revenue, respectively. As the Company firmly drives development through technological innovation in automotive electronics, maintaining intensive R&D investment in intelligent cockpit, intelligent driving, intelligent connectivity, vehicle-road-cloud coordination and high-voltage fast charging for new energy vehicles, it ensures sustained leadership in key technology areas and possesses long-term growth potential. Expanding into Robotics to Build a Second Growth CurveAccording to Frost & Sullivan, the humanoid robot market size is expected to surge from USD2.3 billion in 2025 to USD12.9 billion in 2029, representing a CAGR of 54.4%. The Company has established strategic partnerships with several leading domestic and international robotics companies and has successfully launched a series of products, including AI-empowered robot head assemblies, integrated robot domain controllers and next-generation robot energy management solutions. Investment ThesisAs a leading enterprise in automotive safety and automotive intelligence, the Company possesses strong R&D capabilities. Its automotive-related businesses are expected to continue benefiting from the global trends of vehicle electrification and intelligence, while its expansion into the humanoid robotics field is poised to open up a second growth curve.

We expect Joyson's EPS for 2025-2027 to be 0.88/1.19/1.43 yuan. We revised the target price of RMB 33.4 equivalent to 37.8/28.0/23.4x E P/E 2025-2027 and assign Buy ratings. (Closing price as at 2 March)

RiskOperating collision in Joyson's M&A

Worse-than-expected downstream demand Financials

(Closing price as at 2 March)

Source: PSR Download PDF version...

| Recommendation on 9-3-2026 | | Recommendation | BUY (Maintain) | | Price on Recommendation Date | $ 27.370 | | Suggested purchase price | N/A | | Target Price | $ 33.400 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|