|

MICROTECH MED-B(2235)

Analysis¡G

MicroTech Medical recently issued a positive profit alert. The Group expects revenue for the year ending December 31, 2025 to be no less than RMB 650 million, representing an approximate 88.1% increase compared to RMB 345 million for the year ended December 31, 2024. Net profit attributable to owners of the parent company is expected to be no less than RMB 38 million, compared to a loss of RMB 63.1 million in 2024 ¡X representing an improvement of RMB 101 million. The Group achieved substantial revenue growth in 2025 and successfully turned from loss to profit. This was mainly driven by the continued strong revenue growth from one of its core products ¡X the continuous glucose monitoring (CGM) system ¡X as well as highly effective overseas market expansion. The LinX CGM system successfully entered multiple countries, delivering significant year-on-year growth in international revenue. In addition, the continued deepening of lean management and marked improvement in operational efficiency resulted in a substantial decline in the proportion of selling and administrative expenses to revenue.

The Group¡¦s products now cover 118 countries and regions worldwide. The LinX Continuous Glucose Monitoring System has successfully entered the medical insurance systems of several European countries and has also completed market access in multiple countries across emerging markets such as the Middle East, Asia-Pacific, and South America, providing solid support for international business growth. Recently, the LinX CGM system received marketing approval in Brazil for continuous glucose monitoring in both adults and children. As a core market in Latin America, Brazil offers enormous potential. According to the International Diabetes Federation (IDF) 2025 Global Diabetes Atlas, Brazil has approximately 16.62 million diabetes patients aged 20¡V79, with a prevalence rate of 10.7%, ranking sixth globally in patient numbers. In 2024, Brazil¡¦s diabetes-related expenditure reached approximately USD 45.1 billion, ranking third worldwide after the United States and China. The approval of the Group¡¦s LinX CGM system in Brazil will significantly strengthen its market positioning in Latin America.

The Group¡¦s other core products ¡X the AiDEX X Continuous Glucose Monitoring System and the Equil Patch Insulin Pump System ¡X continue to deepen market penetration. Domestic hospital coverage has exceeded 2,500 facilities, and the products have been sold to 118 countries globally. The Equil Patch Insulin Pump System continues to maintain its leading position among domestically manufactured insulin pumps. In terms of the product R&D pipeline, the Group adheres to independent innovation and self-reliant development. The clinical trial of the AiDEX X CGM system for pregnant women has completed all subject enrollments, providing solid clinical evidence to further expand the applicable patient population. The post-marketing clinical trial for the Equil insulin pump system in Europe has completed patient enrollment, supporting potential medical insurance access. Enrollment for the hybrid closed-loop insulin infusion system¡¦s indication in children aged over 2 has exceeded 50%. Several other innovative products are also advancing rapidly. Furthermore, in view of the development trend of AI large models in the CGM field, the Group has begun strategic positioning by establishing an internal AI team and collaborating with leading domestic research institutions through multiple channels.(I do not hold the above stock)

Strategy¡G

Buy-in Price: $7.50, Target Price: $8.40, Cut Loss Price: $7.10

|

Laopu Gold(6181)

Analysis¡G

Recent news that Laopu Gold will raise product prices has drawn strong market attention. Within less than ten minutes of launching promotional activities on its online platform, multiple high-priced items quickly sold out, and offline stores also saw queues of customers rushing to make purchases. This scenario is quite similar to the consumption frenzy before luxury brands raise prices, earning Laopu Gold the nickname "Hermès of the gold world." On its Tmall flagship store, various items priced at hundreds of thousands of yuan are already showing as out of stock, including a gold bowl priced at 627,500 yuan and a gold gourd priced at 560,900 yuan. For offline stores, counters in cities such as Shanghai and Beijing have experienced a surge in foot traffic, with some consumers specifically trying to complete their purchases before the price hike. We believe that geopolitical risks are on the rise, and gold prices are expected to continue increasing. Laopu Gold's price increase is therefore reasonable. The company is gradually building its own luxury brand in China, and its brand influence and customer loyalty are likely to further improve. The company's financial results are scheduled to be released soon, and we anticipate strong performance. We believe the company exhibits definite growth potential.

Strategy¡G

Buy-in Price: $723.00, Target Price: $822.00, Cut Loss Price: $685.00

|

|

JOYSON Electronics (600699 CH) ¡V Expanding into Robotics to Build a Second Growth Curve

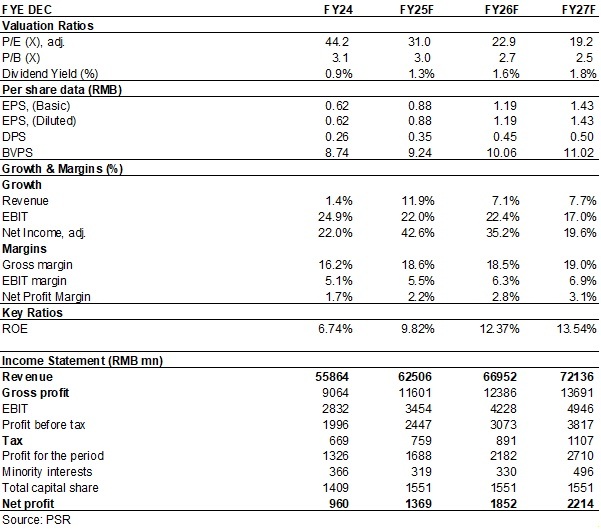

Company ProfileAs a leading global supplier in automotive electronics and automotive safety, Joyson Electronics provides one-stop solutions in key technology areas of intelligent electric vehicles to global OEMs. The Company's business is divided into two major segments: automotive electronics and automotive safety. The automotive electronics segment mainly includes intelligent cockpit, intelligent connectivity, intelligent driving and new energy management, while the automotive safety segment mainly includes products related to seatbelts, airbags, intelligent steering wheels and integrated safety solutions. In 2025, the Company strategically extended into the upstream and downstream of the robotics industry chain, newly positioning itself as "Automotive + Robotics Tier1" and actively building a second growth curve. Investment SummaryThe Company Released Its 2025 Earnings Forecast: Core Profit up 17%It is expected that in 2025 the Company will realise net profit attributable to owners of the parent company of approximately RMB1.35 billion (RMB, the same below), up 40.56% yoy; net profit attributable to the parent company excluding non-recurring items is expected to be approximately RMB1.5 billion, up approximately 17.02% yoy. The difference between the two is mainly due to non-recurring losses of approximately RMB160 million arising from the transfer of the weighing apparatus business by the Company's listed subsidiary Guangdong Xiangshan Weighing Apparatus Group Co., Ltd. (002870.CH), as well as the optimisation and disposal of certain overseas factories. The Company attributes the growth in results to the gradual effectiveness of various profitability improvement and business integration measures implemented across global business regions in 2025, as well as the continued recovery in profitability of overseas operations. Profitability of Core Businesses Continued to ImproveThrough optimising and integrating its global operations, particularly achieving notable results in reducing global raw material costs and improving operational efficiency, the Company has significantly enhanced its operating performance and profitability. The Company's overall gross margin increased from 11.1% in 2022 to 14.5% in 2023, further rising to 16.2% in 2024, and continued to increase to 18.31% as of the third quarter of 2025. From a regional perspective, overseas markets have focused on continuously reducing raw material costs by introducing Chinese suppliers and optimising procurement prices from existing suppliers. Meanwhile, the Company's global operational improvement team has continued to optimise and enhance OEE (Overall Equipment Effectiveness) at overseas factories, while adjusting and relocating production capacity from high-cost countries/regions to low-cost countries/regions, thereby steadily driving gross margin improvement. In particular, cost improvement measures in the European region were implemented earlier and achieved significant gross margin enhancement during the reporting period. Cost improvement measures in the Americas were implemented relatively later, and gross margin is expected to improve correspondingly in the future, with profitability continuing to strengthen. Sufficient Orders on Hand with Sustainable Growth Potential in Core BusinessesIn the third quarter of 2025, the Company secured new orders with a total full lifecycle amount of approximately RMB40.2 billion. In the first three quarters, the Company's cumulative global newly secured orders reached approximately RMB71.4 billion in total full lifecycle amount, of which approximately RMB39.6 billion was from the automotive safety segment and approximately RMB31.8 billion was from the automotive electronics segment. According to Frost & Sullivan, in 2024 the Company's market share in automotive safety products ranked second globally, with global and China market shares of 22.9% and 26.1%, respectively. It is estimated that by 2029, the global and domestic market sizes of the automotive passive safety industry will grow to RMB213.6 billion and RMB49.7 billion, respectively, representing CAGR of 5.4% and 7.8%, respectively, from 2025. It is further expected that by 2029, the global and China automotive electronics market sizes will reach RMB3,330.3 billion and RMB1,892.6 billion, respectively, representing CAGR of 5.8% and 9.4%, respectively, from 2025. In H1 2025, the automotive safety and automotive electronics segments accounted for 62.53% and 27.53% of revenue, respectively. As the Company firmly drives development through technological innovation in automotive electronics, maintaining intensive R&D investment in intelligent cockpit, intelligent driving, intelligent connectivity, vehicle-road-cloud coordination and high-voltage fast charging for new energy vehicles, it ensures sustained leadership in key technology areas and possesses long-term growth potential. Expanding into Robotics to Build a Second Growth CurveAccording to Frost & Sullivan, the humanoid robot market size is expected to surge from USD2.3 billion in 2025 to USD12.9 billion in 2029, representing a CAGR of 54.4%. The Company has established strategic partnerships with several leading domestic and international robotics companies and has successfully launched a series of products, including AI-empowered robot head assemblies, integrated robot domain controllers and next-generation robot energy management solutions. Investment ThesisAs a leading enterprise in automotive safety and automotive intelligence, the Company possesses strong R&D capabilities. Its automotive-related businesses are expected to continue benefiting from the global trends of vehicle electrification and intelligence, while its expansion into the humanoid robotics field is poised to open up a second growth curve.

We expect Joyson's EPS for 2025-2027 to be 0.88/1.19/1.43 yuan. We revised the target price of RMB 33.4 equivalent to 37.8/28.0/23.4x E P/E 2025-2027 and assign Buy ratings. (Closing price as at 2 March)

RiskOperating collision in Joyson's M&A

Worse-than-expected downstream demand Financials

(Closing price as at 2 March)

Source: PSR Download PDF version...

| Recommendation on 3-3-2026 | | Recommendation | BUY (Maintain) | | Price on Recommendation Date | $ 27.370 | | Suggested purchase price | N/A | | Target Price | $ 33.400 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|