|

GREEN TEA GROUP(6831)

Analysis¡G

Green Tea Group has issued a positive profit alert. It expects profit for the year ending 31 December 2025 to range between approximately RMB 460 million and RMB 508 million, representing an increase of about 31.4% to 45.1% compared with RMB 350 million for the year ended 31 December 2024.The increase is mainly attributable to the continued expansion of the restaurant network, which drove revenue growth of approximately RMB 696 million to RMB 1.174 billion from about RMB 3.838 billion in 2024, as well as ongoing improvements in operating efficiency that enhanced store-level profitability. These benefits were partially offset by listing expenses incurred in 2025 (approximately RMB 18 million). Based on a market capitalisation of approximately HKD 5 billion, the implied 2025 price-to-earnings ratio is below 10 times.

The Group is a well-known operator of casual Chinese-style restaurants in mainland China, committed to offering customers a fusion of various regional Chinese cuisines at affordable prices. Benefiting from the flexible and versatile nature of Chinese fusion cuisine, the Group is able to continuously launch new popular dishes to keep pace with the latest dining trends, encouraging frequent customer visits. Menus are developed according to the principles of food safety, stable ingredient supply and standardisation feasibility. In the first half of last year, the Group launched a total of 305 new dishes. As at 30 June 2025, the Group¡¦s restaurant network comprised 502 restaurants, primarily focused on the three major regions of East China, Guangdong Province and North China. It covers 21 provinces, four municipalities directly under the central government and two autonomous regions in mainland China, as well as the Hong Kong Special Administrative Region, including all first-tier cities, 15 new first-tier cities, 31 second-tier cities and 91 third-tier and lower-tier cities. Strategically, the Group places even greater emphasis on the delivery business. In the first half of last year, delivery revenue accounted for 22.9% of total revenue, indicating substantial room for further growth in this segment.

Looking ahead, the Group will continue to refine its menu, enhance service quality and maintain strict food safety controls to build a differentiated reputation moat. To drive sustainable growth, it will steadily advance its network expansion strategy, deepen penetration in existing markets and explore emerging potential markets. At the same time, it will continue to strengthen supply chain optimisation and invest in technology and digital marketing to support standardised and scalable expansion.(I do not hold the above-mentioned shares.)

Strategy¡G

Buy-in Price: $7.20, Target Price: $8.00, Cut Loss Price: $6.80

|

KARRIE INT'L(1050)

Analysis¡G

As a leading global supplier in the server chassis sector, Kali International is deeply benefiting from the explosive growth in AI computing power demand, with AI server chassis emerging as a key growth driver. The company has successfully been included in NVIDIA's qualified supplier list for server chassis and cabinet components and has delivered prototype products for next-generation AI servers such as the MGX and DGX series. Meanwhile, its application-specific integrated circuit (ASIC)-related server products have begun shipments, marking a significant milestone in entering the core AI server supply chain and laying the foundation for future order growth. As AI servers demand improved cooling and reliability, the unit prices and gross margins of related products have also improved accordingly. The company is actively expanding its "China + Thailand" dual production bases, planning to increase the production capacity of its Thailand facility to match that of mainland China to address overseas order growth and mitigate trade risks. For the six months ended September 30, 2025, the company reported revenue of HK$1.609 billion, a yoy increase of 5.4%; net profit of HK$102 million, a yoy decrease of 0.1%; and basic earnings per share of HK$0.05, with an interim dividend of HK$0.015 per share. The Company anticipates that production capacity at its facilities in China and Thailand will continue to face strong demand in 2026. Recently completed private placements have raised funds to expand production capacity in order to meet orders from global data centers and leading AI infrastructure companies.

Strategy¡G

Buy-in Price: $2.68, Target Price: $3.10, Cut Loss Price: $2.45

|

|

Sinotruk (3808 HK) ¡V Parallel Growth in Domestic and Overseas Markets

Company ProfileAs one of the leading heavy truck manufacturers in China, Sinotruk specializes in the heavy trucks, light trucks, buses and related major powertrains and parts. With heavy trucks as the main products, the Company serves a wide range of customers in the infrastructure, construction, container service, logistics, mining, steel and chemical industries. Investment ThesisLeading Position Further ConsolidatedAs a leading enterprise in China's heavy truck industry, SINOTRUK has continued to consolidate its competitive advantages across three key dimensions: sales growth, exports, and new energy transformation. According to publicly disclosed information, in 2025, total heavy truck sales in China reached 1,137 thousand units, up 26% yoy. In 2025, the HOWO and SITRAK dual-brand strategy delivered coordinated growth, supporting the Company's sustained improvement in sales growth. The total vehicle sales volume for the year exceeded 440 thousand units, up 25% yoy, of which heavy truck sales surpassed 300 thousand units. The Company's market share has ranked first in the domestic market for four consecutive years and, for the first time, topped the global heavy truck sales ranking.

In terms of core business structure, heavy truck remains the absolute pillar of the Company's revenue. According to the 2025 interim statements, the heavy truck business contributed 86.9% of revenue, while light truck and other businesses accounted for 14.3%. The financial and engine businesses together accounted for 16.1%, (internal sales 17.2%), reflecting a stable business structure. Remarkable Progress in New Energy Transformation with Further Advancement in IntelligenceIn 2025, the Company's cumulative sales volume of new energy heavy truck reached 27 thousand units, up 249% yoy, ranking first in the industry, with a growth rate significantly exceeding the industry average of 189%. The highest monthly sales volume exceeded 6 thousand units, ranking first in monthly sales of new energy heavy truck. Sales volume of new energy light truck reached 10,300 units, up 196% yoy, ranking third in the industry, achieving rapid penetration in the light commercial vehicle market.

The Company has comprehensively deployed three major technology routes, namely EV, HEV and hydrogen fuel cell, with products covering all application scenarios including tractor units, dump trucks and mixer trucks. Meanwhile, the Company has simultaneously advanced fast-charging and battery swap models, building differentiated competitive advantages.

In the field of intelligent driving, the Company has launched an L2+ level advanced driver assistance system, equipped with intelligent response capabilities for complex road conditions. The system enables a range of functions including intelligent ramp merging and automatic obstacle avoidance in tunnels, and supports the "dual-driver to single-driver" mode. At the end of 2025, the Company globally launched the "Xiaozhong 1.0" intelligent service system, capable of processing complex customer demands in driving operations, maintenance enquiries, fault warnings and behavioural analysis at millisecond level, achieving deep integration of vehicle connectivity and AI large models. This marks a new stage in the Company's intelligent service system. Continuous Breakthroughs in Overseas MarketsIn respect of export business, the Company leverages SINOTRUK International, with products covering more than 150 countries and regions across Africa, Southeast Asia, Central Asia and the Middle East. In 2025, the Company's annual export sales volume of heavy truck exceeded 150 thousand units, up 14% yoy, ranking first in China's heavy truck exports for 21 consecutive years. The Company has continued to expand into high-end markets, achieving breakthrough growth in strategic regions such as Saudi Arabia and Morocco, demonstrating strong demand for the Company's highly cost-effective products. The Company has advanced its localisation strategy by establishing 37 KD assembly plants in 27 countries worldwide, significantly enhancing market penetration and service response efficiency. In addition, the Company has actively broadened its export product portfolio. Revenue from export of after-market parts increased by 53% yoy for the year, forming a dual-engine overseas expansion model of "complete vehicles + parts". Stable Financial PerformanceIn H1 2025, the Company reported revenue of RMB50.88 billion (RMB, the same below), up 4.2% yoy, and net profit attributable to the parent company of RMB3.43 billion, up 4.0% yoy, delivering a solid result. Gross margin reached 15.1%, up 0.4 ppts yoy, mainly attributable to improved profitability of heavy truck products. Net profit margin stood at 7.3%, with profitability remaining stable. In terms of expenses, distribution costs accounted for 3.5% of product revenue, up 0.3 ppts yoy, while administrative expenses accounted for 4.7% of revenue, down 0.2 ppts yoy. Overall changes in costs and expenses were primarily driven by sales volume growth, optimisation of product mix and a decline in financing costs.

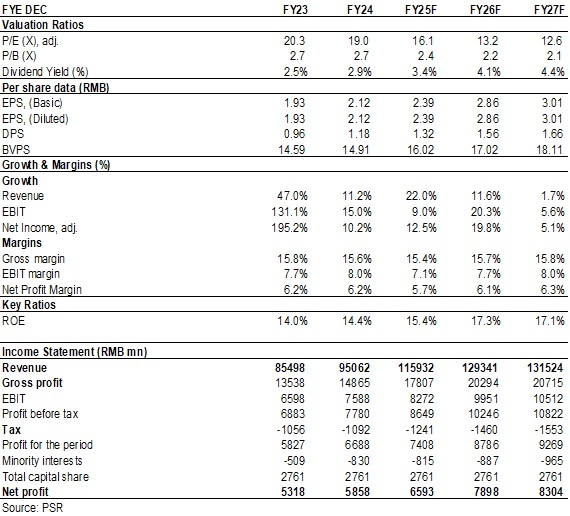

The Company's dividend payout ratio has continued to increase over the past five years. In the interim period of 2025, a cash dividend payout ratio of 55% has been implemented. Going forward, the Company will dynamically enhance the cash dividend payout ratio based on operating performance and funding requirements. Valuation & Investment SuggestionIn January 2026, the Company's heavy truck export volume exceeded 16 thousand units for the first time, setting another monthly record. Currently, order reserves remain abundant. In January alone, Jinan Truck Manufacturing Company secured orders exceeding 28.6 thousand units. Management has set a target to achieve total vehicle sales of over 800 thousand units by 2030, equivalent to a CAGR of 12.5% over the next five years, effectively rebuilding another "SINOTRUK". With the continuation of the heavy truck replacement subsidy policy, we expect the Company to continue benefiting from the recovery of China's heavy truck industry and the growth trend in export markets. In the medium to long term, there are opportunities for value enhancement in some segmentations of heavy trucks brought by innovation. We expected the Company's EPS in 2025/2026/2027 to be 2.39/2.86/3.01 yuan, respectively, and adjust the target price to HKD 49.3, corresponding to 18.5/15.2/14.4x P/E and 2.8/2.5/2.4x P/B in 2025/2026/2027, with 'Accumulate' rating. (Closing price as at 23 February)

Source: Wind, Phillip Securities Hong Kong Research RiskThe economic recovery was less than expected, resulting in lower than expected sales of heavy trucks

Overseas market risk, adverse exchange direction risk

Risk of significant increase in raw materials Financials

(Closing price as at 23 February)

Source: PSR Download PDF version...

| Recommendation on 27-2-2026 | | Recommendation | Accumulate (Downgrade) | | Price on Recommendation Date | $ 42.960 | | Suggested purchase price | N/A | | Target Price | $ 49.300 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|