|

SANHUA(2050)

Analysis¡G

Sanhua Intelligent Controls recently issued a positive profit alert, expecting net profit attributable to shareholders for the year ended December 31, 2025 to range between RMB 3.873 billion and RMB 4.648 billion, representing a 25% to 50% increase compared with 2024. This is mainly because the group has continued to consolidate its industry-leading position in refrigeration and air-conditioning appliance components, fully capitalizing on opportunities from growing market demand while leveraging the technological accumulation and large-scale production advantages of its core products to drive sustained expansion in this segment. At the same time, relying on its leading global market layout in new energy vehicle thermal management, the group has continued to secure high-quality orders through the demonstration effect of benchmark clients, further strengthening the performance growth momentum of its automotive components business. The two major business segments are working in synergy, providing solid support for the group¡¦s full-year results growth.

With rising energy costs, consumers are increasingly inclined to purchase energy-efficient and low-carbon appliances, which has propelled the development of the refrigeration and air-conditioning appliance components industry. In addition, the rapid growth of the cold-chain logistics and data-center sectors has brought broad development opportunities to emerging markets. In the new energy vehicle sector, advances in high-voltage fast charging and battery technologies have increased the need for rapid heat dissipation, driving demand for efficient vehicle thermal management systems and thereby stimulating growth in demand for related components. At the same time, progress in automotive thermal management technology is pushing components toward integrated and modular designs. Higher computing-power requirements for automotive chips also call for intelligent thermal management systems to optimize heat dissipation, resulting in continuously rising demand for high-efficiency thermal management components. Furthermore, advancements in battery cooling and heating technologies, the development of heat pump systems, and the adoption of low-global-warming-potential refrigerant alternatives are all helping to optimize vehicle energy consumption, placing even higher performance demands on thermal management system components.

As one of the pioneering companies leading the development of thermal management technology, the group has successfully entered the field of bionic robot electromechanical actuators by leveraging its expertise in motor manufacturing, together with its advantages in scale and cost control. With continuous technological progress, the downstream applications of bionic robots have expanded from the industrial sector to multiple industries including medical services and logistics services. The wide range of application scenarios has stimulated growing demand for bionic robot electromechanical actuators.(I do not hold the above stock).

Strategy¡G

Buy-in Price: $36.80, Target Price: $40.00, Cut Loss Price: $35.00

|

UBTECH ROBOTICS(9880)

Analysis¡G

In the first half of 2025, the company's operating revenue was 621 million RMB, a year-on-year increase of 27.5%. Within this, revenue from educational intelligent robots and intelligent robotic solutions was 240 million RMB, accounting for 38.6% of the total; revenue from logistics intelligent robots and intelligent robotic solutions was 56 million RMB, representing 9%; revenue from customized intelligent robots and intelligent robotic solutions for other industries was 64 million RMB, accounting for 10.3%; revenue from consumer-grade robots and other hardware devices was 260 million RMB, representing 41.8%; and other income was 1.627 million RMB, accounting for 0.3%. The gross margin was 35%. The company has not yet turned a profit, with a loss of 440 million RMB for the period, narrowing by 22.7% year-on-year. This year's Spring Festival Gala featured robots from multiple companies taking the stage, attracting widespread market attention and providing strong short-term catalysts for the robotics industry. Since February, nearly 3 billion RMB has been deployed early into robotics ETFs. Many fund companies predict that from 2026 onwards, the humanoid robot sector will undergo a quantitative shift from tens of thousands to hundreds of thousands of units. The robotics industry is accelerating from a sci-fi concept into the fast lane of industrialization at an unprecedented pace. As a leading enterprise in China's humanoid robot sector, UBTECH ROBOTICS has built core barriers with its full-stack self-developed technology, accelerated commercialization, secured over 1.4 billion RMB in orders on hand, and achieved an annual production capacity of thousands of units in 2025, positioning it to benefit from the rapid growth of the humanoid robot industry. Despite short-term challenges such as sustained losses, cost control pressures, and intensified industry competition, the company's technological leadership, multi-scenario layout, and clear path to cost reduction through scaling offer long-term first-mover advantages in the trillion-yuan embodied intelligence channel.

Strategy¡G

Buy-in Price: $144.50, Target Price: $161.00, Cut Loss Price: $137.00

|

|

Weichai (2338 HK) - From a cyclical heavy truck enterprise to a structurally growing energy platform

Company ProfileWeichai is one of the automobile and equipment manufacturing groups with the strongest comprehensive strength in China's heavy truck industry. Based on the powertrain system including engine, axle and gearbox, the Company extends upstream components and downstream heavy trucks, and takes the lead in forklifts and intelligent warehousing. After years of development, the Company has built a synergetic development pattern of four major industrial segments including powertrain (engine, transmission, axle/hydraulics), vehicle and machinery, intelligent logistics and other segments. Investment SummaryPerformance Review: Revenue Grows Steadily, Net Profit Continues to Improve

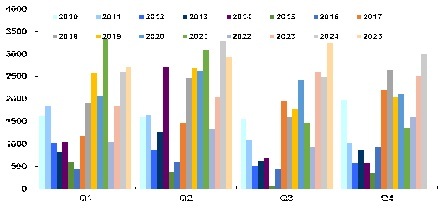

According to Weichai Power's FY2025 third-quarter report: In the first nine months of 2025, the company reported a revenue of RMB170.57 billion, representing a year-on-year (YoY) growth of 5.3%. Net profit attributable to the parent company amounted to RMB8.88 billion, marking a YoY increase of 5.7%. The net profit after excluding non-recurring items reached RMB7.97 billion, up 3.4% YoY, reflecting steady progress in overall performance.

Looking at the results by quarter, the revenues for the first three quarters were RMB57.46 billion, RMB55.69 billion, and RMB57.42 billion, showing YoY changes of +1.9%, -0.8%, and +16.1%, respectively. Net profit attributable to the parent company was RMB2.71 billion, RMB2.93 billion, and RMB3.23 billion, reflecting YoY changes of +4.3%, -11.2%, and +29.5%, respectively. The first two quarters saw more moderate growth in net profit, while the third quarter showed a sharp increase, mainly due to fluctuations in oil and gas price differentials and policy subsidies. The domestic natural gas heavy truck industry experienced a high in the early period of 2024 followed by a decline in the later period, while 2005 saw a weak first half and a rapid recovery in the second half, driving fluctuations in the company's natural gas engine sales. Additionally, in the first half of the year, Kion incurred a one-time expense related to its efficiency plan, resulting in a negative impact of RMB480 million. After adjusting for this, the net profit attributable to the parent company in the first half of the year increased by 3.8% YoY to RMB6.13 billion.

Profitability Remains Resilient

In terms of profitability, for the first three quarters, the company's gross margin and net profit margin attributable to the parent company were 21.9% and 5.2%, respectively, largely unchanged YoY (+0.04 ppts, +0.01 ppts). The sales expense ratio for the first three quarters was 5.82%, up by 0.18 ppts YoY, the administrative expense ratio was 5.4%, up by 0.74 ppts YoY, and the R&D expense ratio was 3.62%, down by 0.21 ppts YoY.

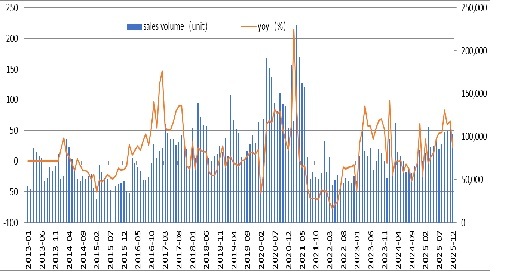

In detail, the gross margin for the first three quarters was 22.2%, 22.1%, and 21.4%, with YoY changes of +0.12 ppts, +0.74 ppts, and -0.74 ppts, respectively. The net profit margin attributable to the parent company was 4.72%, 5.27%, and 5.63%, with YoY changes of +0.11 ppts, -0.62 ppts, and +0.58 ppts, respectively. Profitability remains resilient, primarily due to the improved profitability of subsidiaries Shaanxi Heavy Duty Truck and Kion, as well as the fluctuation in provisions, supply chain optimization, and continuous cost reduction and efficiency improvements in various stages. Heavy Truck Industry Structural Reshuffle, Weichai remain Steady Product AdvantagesIn January 2025, the government introduced a subsidy policy to promote vehicle replacements, expanding the subsidy coverage to vehicles meeting the National IV emission standard and below. In March, the policy was further extended to natural gas heavy trucks, driving a gradual increase in demand for heavy trucks. The penetration rate of natural gas and new energy heavy trucks has rapidly increased under the dual influence of policy and technology. According to data from the China Association of Automobile Manufacturers (CAAM), the cumulative sales of heavy trucks in the Chinese market reached 1,145 thousand units in 2005, a YoY growth of 27%. Of this, 341 thousand units were exported, showing a YoY growth of 17.4%. The market now features a three-way division among diesel, natural gas, and new energy vehicles, with market shares of 46%, 25%, and 29%, respectively.

To align with industry trends, the company has developed multiple technological routes, including pure electric, fuel cell, and hybrid solutions. In the first three quarters, the company sold a total of 536 thousand engines, including 188 thousand heavy truck engines. By fuel type, the sales of diesel heavy truck engines were approximately 117 thousand units, while natural gas heavy truck engines accounted for around 71 thousand units. According to the First Commercial Vehicle Network, the company's new energy power system business achieved a revenue of RMB1.97 billion (RMB, the same below) in the first three quarters of 2005, marking an 84% YoY growth. Its subsidiary, Shaanxi Heavy Duty Truck, sold 109 thousand heavy trucks in the first three quarters, a YoY growth of 18%. Sales of new energy heavy trucks reached about 16 thousand units, a YoY growth of approximately 2.5 times, maintaining a leading position in the industry.

Looking ahead, the expected balanced supply-demand structure is likely to support natural gas prices at a stable and reasonable range, and the application of natural gas heavy trucks will become more widespread, with the penetration rate continuing to rise. With continued policy support, technological upgrades, and improvements in infrastructure, the market penetration of new energy heavy trucks is also expected to keep increasing. In the medium term, the positive effects of fiscal and monetary stimulus policies, along with the next phase of emission standard upgrades in the industry, will have a positive impact on heavy truck sales. Weichai leads the market share in heavy truck engines, particularly in the natural gas heavy truck engine market, with shares of 23% and 52%, respectively, and is expected to benefit first. Accelerated Computing Infrastructure Drives Growth in Large-Bore Engine and Fuel Cell (SOFC) BusinessesWith the rapid iteration of AI technology in recent years driving the acceleration of computing infrastructure, the power generation industry has experienced rapid growth. The demand for backup power engines has surged, and the company has deeply invested in multiple product forms, including diesel, natural gas, and solid oxide fuel cells (SOFC), to meet market needs. The company's large-bore engine (diesel) business has reached a certain scale and is entering a phase of rapid growth. In the first three quarters of 2005, sales exceeded 7,700 units, marking a YoY increase of over 30%. Among these, sales of products related to data centers surpassed 900 units, growing more than threefold YoY.

Regarding solid oxide fuel cells, in November, Weichai signed a manufacturing license agreement with its affiliate, Ceres, to establish production lines for batteries and stacks to be used in the stationary power generation market. Some key components will be supplied by Ceres, and the products will provide power for applications such as AI data centers, commercial buildings, and industrial parks. This means the company will have full control over the core technologies of batteries, stacks, systems, and power stations, and will be authorized to enter the global market for sales. Currently, the company has now a good order backlog in the SOFC field, with promising profit prospects.

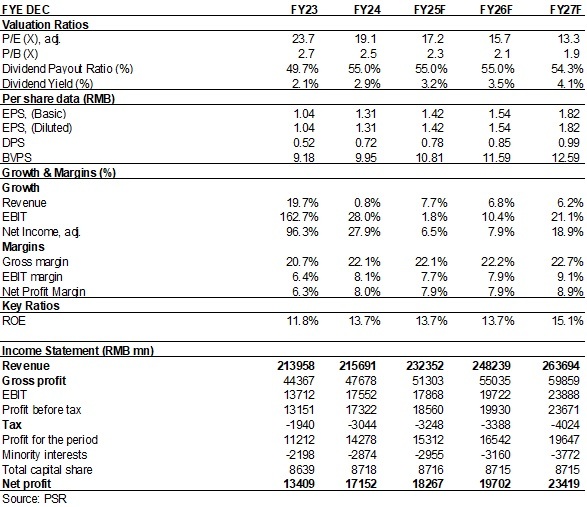

We expect that with the rapid development of the global computing power market, the domestic supply chain will gradually mature and production capacity will steadily be released, leading to an accelerated expansion of the power generation equipment business order scale. The second growth curve is becoming increasingly clear. Investment ThesisAs the share of profits from AIDC power generation business is expected to exceed 30% by 2030, the company is being revalued from a cyclical heavy truck enterprise to a structurally growing energy platform, with broad long-term growth potential. Overall, the company's leading position remains solid, with a clear strategy framework of "power + hydraulics + new energy". The forward-looking new businesses are opening up growth potential, and the high dividend payout ratio is expected to be maintained.

We forecast the EPS of the Company to be RMB 1.42/1.54/1.82 yuan in 2005/2006/2007. We will also revise target price to 34.6HKD (22/20/17x P/E and 2.9/2.6/2.4x P/B for 2005/2006/2007) and BUY rating. (Closing price as at 5 February) Domestic Heavy-duty truck monthly sales and growth

Source: Wind, Company, Phillip Securities Hong Kong Research Weichai Quarterly Net Profit

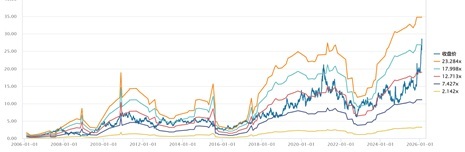

Source: Wind, Company, Phillip Securities Hong Kong Research Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research Financials

(Closing price as at 5 February)

Click here to download PDF version...

| Recommendation on 23-2-2026 | | Recommendation | BUY (Maintain) | | Price on Recommendation Date | $ 27.200 | | Suggested purchase price | N/A | | Target Price | $ 34.600 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|