|

KINGSOFT CLOUD(3896)

Analysis¡G

Kingsoft Cloud continues to execute its high-quality sustainable development strategy effectively. In the third quarter ended September 30, 2025, the company achieved accelerated revenue growth and improved profitability. Both adjusted operating profit and adjusted net profit turned positive for the first time on a quarterly basis. The integration of artificial intelligence and cloud services has brought significant market opportunities for the group.

In the third quarter of last year, the group¡¦s revenue growth accelerated year-over-year to 31.4%, reaching RMB 2.478 billion, and increased 5.5% quarter-over-quarter from RMB 2.349 billion in the second quarter of 2025. This was primarily driven by the continuous upgrades to AI infrastructure and products, leading to revenue growth from AI-related customers. Among them, public cloud services revenue surged 49.1% year-over-year to RMB 1.752 billion. During the period, AI business billings reached RMB 782 million, with a growth rate of approximately 120%. The strategic cooperation with the Xiaomi-Kingsoft ecosystem continued to strengthen, with revenue contribution from this ecosystem surging 83.8% to RMB 690 million (or approximately RMB 6.9 billion in some references, but aligned with official ~RMB 691 million). The group¡¦s adjusted gross profit was RMB 392 million, up 27.6% year-over-year and 12% quarter-over-quarter, mainly due to the expansion in revenue scale (particularly from intelligent computing cloud services). Adjusted EBITDA profit reached RMB 826 million, representing a 345.9% increase. The adjusted EBITDA margin was 33.4%, up 23.6 percentage points, primarily attributable to improvements in cost and expense control, as well as non-recurring other income realized in this quarter. The group achieved a turnaround in adjusted operating profit to a profit of RMB 15.4 million, compared to a loss of RMB 140 million in the same quarter last year and a loss of RMB 166 million in the previous quarter. Adjusted net profit achieved profitability for the first time, reaching RMB 28.7 million, versus an adjusted net loss of RMB 236 million in the same quarter last year.

Xiaomi is expected to invest approximately RMB 10 billion in the AI field in 2026. As the cloud service provider for the Xiaomi ecosystem, Kingsoft Cloud will be a major beneficiary. It is anticipated that Kingsoft Cloud will update its agreement with Xiaomi before mid-2026, raising the revenue cap for 2026-2027 by 10% to 15%, implying a compound annual growth rate (CAGR) of approximately 37% for revenue from Xiaomi between 2025 and 2028. The group has not only rapidly expanded intelligent computing cloud within public cloud but has also actively laid the strategic foundation for deep integration of AI with industries in enterprise cloud. The company is excited and optimistic about the rapid adoption of AI across ecosystems and diverse vertical sectors, which will bring substantial AI-driven growth opportunities.(I do not hold the above stock)

Strategy¡G

Buy-in Price: $7.70, Target Price: $8.40-9.00, Cut Loss Price: $7.25

|

STREAMAX TECH(002970)

Analysis¡G

The Company is a global leader in commercial vehicle video surveillance, covering all models of commercial vehicles and leading the global market share. The main products include commercial vehicle universal monitoring products, commercial vehicle comprehensive monitoring information systems, and fixed video monitoring products, providing intelligent networked industry solutions for commercial vehicles such as buses/taxis/two passengers and one danger/trucks/dump trucks. The Company continues to expand its overseas market share, and in recent years, its overseas business revenue has exceeded that of the domestic market. In the first half of 2025, overseas revenue accounted for 70% of the company's total, and the European safety management solution was launched. Progress in the European standard bus sector is rapid, with new regulations expected to drive revenue growth. Recently, the company officially initiated server power supply OEM operations, focusing on edge-side AI application models, and has introduced the SafeGPT driving safety cognition model, with further developments anticipated. Its FY2025 earnings positive alert indicates a projected increase in net profit attributable to the parent company by 27.6% to 37.9% yoy.

Strategy¡G

Buy-in Price: RMB78.60, Target Price: RMB90.20, Cut Loss Price: RMB72.20

|

|

Weichai (2338 HK) - From a cyclical heavy truck enterprise to a structurally growing energy platform

Company ProfileWeichai is one of the automobile and equipment manufacturing groups with the strongest comprehensive strength in China's heavy truck industry. Based on the powertrain system including engine, axle and gearbox, the Company extends upstream components and downstream heavy trucks, and takes the lead in forklifts and intelligent warehousing. After years of development, the Company has built a synergetic development pattern of four major industrial segments including powertrain (engine, transmission, axle/hydraulics), vehicle and machinery, intelligent logistics and other segments. Investment SummaryPerformance Review: Revenue Grows Steadily, Net Profit Continues to Improve

According to Weichai Power's FY2025 third-quarter report: In the first nine months of 2025, the company reported a revenue of RMB170.57 billion, representing a year-on-year (YoY) growth of 5.3%. Net profit attributable to the parent company amounted to RMB8.88 billion, marking a YoY increase of 5.7%. The net profit after excluding non-recurring items reached RMB7.97 billion, up 3.4% YoY, reflecting steady progress in overall performance.

Looking at the results by quarter, the revenues for the first three quarters were RMB57.46 billion, RMB55.69 billion, and RMB57.42 billion, showing YoY changes of +1.9%, -0.8%, and +16.1%, respectively. Net profit attributable to the parent company was RMB2.71 billion, RMB2.93 billion, and RMB3.23 billion, reflecting YoY changes of +4.3%, -11.2%, and +29.5%, respectively. The first two quarters saw more moderate growth in net profit, while the third quarter showed a sharp increase, mainly due to fluctuations in oil and gas price differentials and policy subsidies. The domestic natural gas heavy truck industry experienced a high in the early period of 2024 followed by a decline in the later period, while 2005 saw a weak first half and a rapid recovery in the second half, driving fluctuations in the company's natural gas engine sales. Additionally, in the first half of the year, Kion incurred a one-time expense related to its efficiency plan, resulting in a negative impact of RMB480 million. After adjusting for this, the net profit attributable to the parent company in the first half of the year increased by 3.8% YoY to RMB6.13 billion.

Profitability Remains Resilient

In terms of profitability, for the first three quarters, the company's gross margin and net profit margin attributable to the parent company were 21.9% and 5.2%, respectively, largely unchanged YoY (+0.04 ppts, +0.01 ppts). The sales expense ratio for the first three quarters was 5.82%, up by 0.18 ppts YoY, the administrative expense ratio was 5.4%, up by 0.74 ppts YoY, and the R&D expense ratio was 3.62%, down by 0.21 ppts YoY.

In detail, the gross margin for the first three quarters was 22.2%, 22.1%, and 21.4%, with YoY changes of +0.12 ppts, +0.74 ppts, and -0.74 ppts, respectively. The net profit margin attributable to the parent company was 4.72%, 5.27%, and 5.63%, with YoY changes of +0.11 ppts, -0.62 ppts, and +0.58 ppts, respectively. Profitability remains resilient, primarily due to the improved profitability of subsidiaries Shaanxi Heavy Duty Truck and Kion, as well as the fluctuation in provisions, supply chain optimization, and continuous cost reduction and efficiency improvements in various stages. Heavy Truck Industry Structural Reshuffle, Weichai remain Steady Product AdvantagesIn January 2025, the government introduced a subsidy policy to promote vehicle replacements, expanding the subsidy coverage to vehicles meeting the National IV emission standard and below. In March, the policy was further extended to natural gas heavy trucks, driving a gradual increase in demand for heavy trucks. The penetration rate of natural gas and new energy heavy trucks has rapidly increased under the dual influence of policy and technology. According to data from the China Association of Automobile Manufacturers (CAAM), the cumulative sales of heavy trucks in the Chinese market reached 1,145 thousand units in 2005, a YoY growth of 27%. Of this, 341 thousand units were exported, showing a YoY growth of 17.4%. The market now features a three-way division among diesel, natural gas, and new energy vehicles, with market shares of 46%, 25%, and 29%, respectively.

To align with industry trends, the company has developed multiple technological routes, including pure electric, fuel cell, and hybrid solutions. In the first three quarters, the company sold a total of 536 thousand engines, including 188 thousand heavy truck engines. By fuel type, the sales of diesel heavy truck engines were approximately 117 thousand units, while natural gas heavy truck engines accounted for around 71 thousand units. According to the First Commercial Vehicle Network, the company's new energy power system business achieved a revenue of RMB1.97 billion (RMB, the same below) in the first three quarters of 2005, marking an 84% YoY growth. Its subsidiary, Shaanxi Heavy Duty Truck, sold 109 thousand heavy trucks in the first three quarters, a YoY growth of 18%. Sales of new energy heavy trucks reached about 16 thousand units, a YoY growth of approximately 2.5 times, maintaining a leading position in the industry.

Looking ahead, the expected balanced supply-demand structure is likely to support natural gas prices at a stable and reasonable range, and the application of natural gas heavy trucks will become more widespread, with the penetration rate continuing to rise. With continued policy support, technological upgrades, and improvements in infrastructure, the market penetration of new energy heavy trucks is also expected to keep increasing. In the medium term, the positive effects of fiscal and monetary stimulus policies, along with the next phase of emission standard upgrades in the industry, will have a positive impact on heavy truck sales. Weichai leads the market share in heavy truck engines, particularly in the natural gas heavy truck engine market, with shares of 23% and 52%, respectively, and is expected to benefit first. Accelerated Computing Infrastructure Drives Growth in Large-Bore Engine and Fuel Cell (SOFC) BusinessesWith the rapid iteration of AI technology in recent years driving the acceleration of computing infrastructure, the power generation industry has experienced rapid growth. The demand for backup power engines has surged, and the company has deeply invested in multiple product forms, including diesel, natural gas, and solid oxide fuel cells (SOFC), to meet market needs. The company's large-bore engine (diesel) business has reached a certain scale and is entering a phase of rapid growth. In the first three quarters of 2005, sales exceeded 7,700 units, marking a YoY increase of over 30%. Among these, sales of products related to data centers surpassed 900 units, growing more than threefold YoY.

Regarding solid oxide fuel cells, in November, Weichai signed a manufacturing license agreement with its affiliate, Ceres, to establish production lines for batteries and stacks to be used in the stationary power generation market. Some key components will be supplied by Ceres, and the products will provide power for applications such as AI data centers, commercial buildings, and industrial parks. This means the company will have full control over the core technologies of batteries, stacks, systems, and power stations, and will be authorized to enter the global market for sales. Currently, the company has now a good order backlog in the SOFC field, with promising profit prospects.

We expect that with the rapid development of the global computing power market, the domestic supply chain will gradually mature and production capacity will steadily be released, leading to an accelerated expansion of the power generation equipment business order scale. The second growth curve is becoming increasingly clear. Investment ThesisAs the share of profits from AIDC power generation business is expected to exceed 30% by 2030, the company is being revalued from a cyclical heavy truck enterprise to a structurally growing energy platform, with broad long-term growth potential. Overall, the company's leading position remains solid, with a clear strategy framework of "power + hydraulics + new energy". The forward-looking new businesses are opening up growth potential, and the high dividend payout ratio is expected to be maintained.

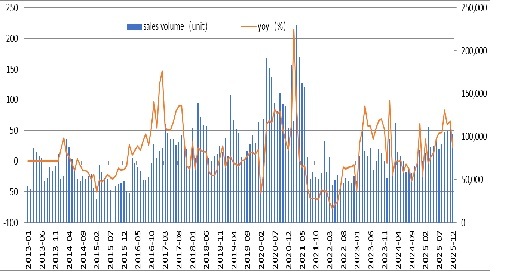

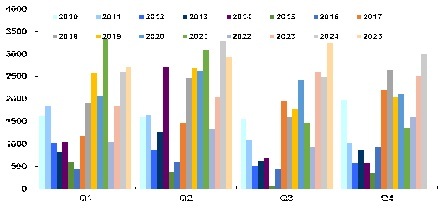

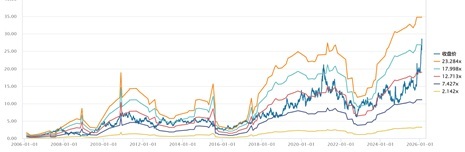

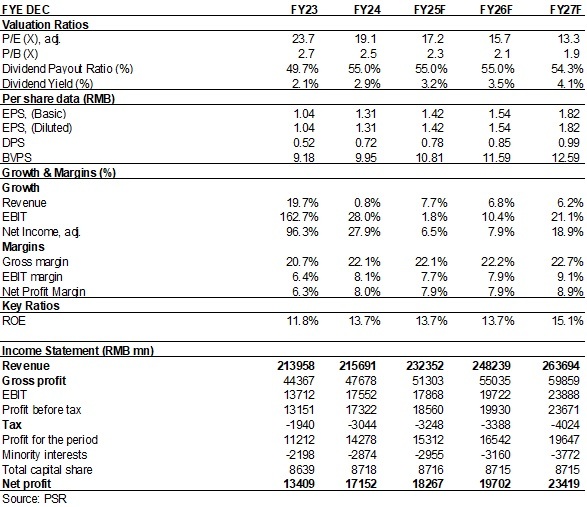

We forecast the EPS of the Company to be RMB 1.42/1.54/1.82 yuan in 2005/2006/2007. We will also revise target price to 34.6HKD (22/20/17x P/E and 2.9/2.6/2.4x P/B for 2005/2006/2007) and BUY rating. (Closing price as at 5 February) Domestic Heavy-duty truck monthly sales and growth

Source: Wind, Company, Phillip Securities Hong Kong Research Weichai Quarterly Net Profit

Source: Wind, Company, Phillip Securities Hong Kong Research Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research Financials

(Closing price as at 5 February)

Click here to download PDF version...

| Recommendation on 13-2-2026 | | Recommendation | BUY (Maintain) | | Price on Recommendation Date | $ 27.200 | | Suggested purchase price | N/A | | Target Price | $ 34.600 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|