|

SUNeVision(1686)

Analysis¡G

SUNeVision is benefiting from AI demand and data center expansion, with new client deployments across its portfolio of data centers. Notably, Phase 1 of MEGA IDC ¡X Hong Kong¡¦s hyperscale data center with the largest power capacity ¡X was successfully commissioned in 2024, and occupancy is expected to rise further by FY2026. Construction of Phase 2 has already begun and is slated for completion in 2026/2027, adding approximately 350,000 sq ft of floor area to continue meeting demand from hyperscale cloud customers. The Group¡¦s data center in Tsuen Wan has also seen new client deployments, while the Sha Tin facility is benefiting from power capacity upgrade projects that enable it to fulfil new customer requirements and increase overall capacity. In addition, clients at other data centers are accelerating their expansion plans. As a premium data center provider in the market, the Group has devoted substantial resources to ensuring all its facilities maintain rigorous physical and network security controls, with regular third-party professional audits and testing. Unlike many data centers that frequently change ownership, SUNeVision focuses on long-term development and continues to invest in facility optimisation to create value for customers.

Artificial intelligence is increasingly driving demand for inference and cloud services, a trend that now spans the Group¡¦s entire data center portfolio. In particular, inquiries from Chinese hyperscale clients about capacity expansion have risen sharply as they seek to integrate more AI inference services into their core offerings. This trend is already delivering direct benefits to the Group, with AI-related deployments growing at MEGA Gateway and MEGA-Two. Supported by MEGA-i¡¦s extensive fibre interconnect and subsea cable ecosystem, the Group¡¦s connectivity business remains robust. MEGA-i is Hong Kong¡¦s premier connectivity hub and ranks among the global top five.

Looking ahead, demand is expected to stay strong as more data traffic to and from mainland China routes through Hong Kong, reinforcing the city¡¦s position as Asia¡¦s leading connectivity hub. The Group will manage future capital expenditure flexibly and on a demand-driven basis. Currently, it has the ability to deliver capacity within four to six months of order confirmation ¡X a model that allows it to efficiently address frequent urgent client needs while optimizing capex through a just-in-time approach.The Group will continue to prioritize investment in high-quality projects that require advanced infrastructure and are expected to deliver above-market returns. Through disciplined capital allocation and a prudent balance sheet, it is well positioned to enhance returns and maintain strong financial health. As of 30 September 2025, the adjusted gearing ratio stood at a healthy 44% (or 31% excluding shareholder loans). Backed by strong support from parent company Sun Hung Kai Properties, the Group has ample liquidity and financial resources to capitalise on rising AI inference demand in Hong Kong.(I do not hold the stock)

Strategy¡G

Buy-in Price: $6.60, Target Price: $7.50, Cut Loss Price: $6.30

|

GIGADEVICE(603986)

Analysis¡G

The company is a leading domestic manufacturer of storage chip design, offering products such as NOR Flash (non-volatile memory) and DRAM (volatile memory). It is also actively developing and researching MCU (microcontroller) and related peripheral products. Its products are widely used in handheld mobile terminals like smartphones and tablets, consumer electronics, IoT devices, personal computers and peripherals, as well as automotive electronics and industrial control equipment. The company's core businesses include flash memory chip products, microcontroller products (MCU), sensor modules, and dynamic random-access memory (DRAM). The sensor business is operated through the acquisition of Shanghai Silil Microelectronics Technology Co., Ltd. in 2019. In the first three quarters of 2025, the company achieved operating revenue of 6.832 billion yuan, a yoy increase of 20.92%; net profit attributable to the parent company was 1.083 billion yuan, up 30.18% yoy. Benefiting from the rising storage price cycle, the Company's profitability significantly improved, with Q3 alone reporting net profit attributable to the parent company of 508 million yuan, up 61.13% yoy and 48.97% qoq. Gross margin reached 40.72%, an increase of 3.71 percentage points qoq. The Company announced its FY2025 positive alert: annual operating revenue of 9.203 billion yuan, up 25% yoy, and net profit attributable to the parent company of 1.61 billion yuan, up 46% yoy. Currently, AI continues to drive demand growth in sectors such as smartphones, PCs, and servers, positioning the company's products to benefit further.

Strategy¡G

Buy-in Price: $288.00, Target Price: $321.00, Cut Loss Price: $270.00

|

|

Yinlun (002126 CH) - leader in Automotive Thermal Management, continuously Expanding Growth Curve

Company profile:Yinlun Co., Ltd. originated from Tiantai Machinery Factory established in 1958. It was restructured into a privately held joint-stock company in 1999 and was listed on the main board of the Shenzhen Stock Exchange in 2007. The Company primarily produces heat exchangers and thermal management products for oil, water, gas, and refrigerant systems, as well as automotive air conditioning systems and related products for post-treatment exhaust systems.

The Company's business is mainly divided into four strategic lines. The first line focuses on thermal management for traditional vehicles and off-road machinery. The second line targets thermal management for new energy vehicles. The third line includes thermal management solutions for power stations, substations, energy storage systems, charging and battery swapping infrastructure, data centres, and low-altitude aircraft. The fourth line encompasses embodied intelligence modules including rotary joint modules, linear joint modules, dexterous hand modules, and thermal management modules.

After over 40 years of development, the Company has become a leading enterprise in China's automotive thermal management industry. In terms of industry position, the Company has maintained the number one domestic ranking in heat exchanger production and sales volume for 20 consecutive years. With more than 10 thousand employees globally, it has established production bases in 10 provinces and cities in China, as well as in seven countries including the United States, Mexico, and Sweden, thus possessing global supply capabilities. In H1 2025, the revenue contribution from the Company's overseas business reached 25.94%. Key clients include Mercedes-Benz, BYD, Cummins, Caterpillar, CATL, and Sungrow. Investment SummaryIndustry Analysis:

Thermal Management for New Energy Vehicles Rises in Volume and Value

In 2025, China's new energy vehicle sales reached 16,490 thousand units, up 28% yoy, with penetration exceeding 50%. The unit value of thermal management systems for new energy vehicles is 3 to 4 times that of traditional internal combustion vehicles (RMB5,850 to RMB6,050 for PTC systems (RMB, the same below), RMB9,550 to RMB9,950 for CO₂ heat pump systems), driving rapid expansion of the thermal management market. By 2025, the global thermal management market for new energy vehicles is projected to reach RMB226.5 billion, with a CAGR of 32.95% from 2022 to 2026; the China market is expected to reach RMB96.4 billion, with a CAGR of 20.33%. On the technology front, integrated thermal management systems (ITMS) are becoming mainstream, enhancing energy efficiency through integrated design of multi-way valves and heat exchangers. AI algorithms are dynamically optimising thermal strategies, and new materials such as phase-change materials and graphene thermal films are promoting lightweight design. The competitive landscape features "international Tier 1 takes the lead + domestic players break through". Leading domestic companies such as Yinlun Co., Ltd. have entered the global supply chain by leveraging advantages in specific products like oil coolers and water-cooled plates. In 2024, thermal management products for new energy vehicles accounted for 42% of the Company's revenue, with sales of 25,490 thousand units.

AI Computing Power Demand Drives Explosive Growth in Liquid Cooling of the Data Centre

The iteration of AI large models has led to increased power density in data centres. NVIDIA's next-generation Rubin GPU has a power consumption of 2,300W, making traditional air cooling insufficient. Liquid cooling has become a necessity due to its high efficiency (thousands of times greater than air cooling) and low PUE (maintainable below 1.15). In 2024, China's liquid-cooled server market reached USD2.37 billion, and is expected to exceed USD16.2 billion by 2029, with a CAGR of 46.8%. Global cloud vendors are significantly increasing capital expenditure; leading North American firms plan to invest USD500 billion over the next four years in building AI data centres. Meanwhile, China's "east data, west computing" policy is driving higher liquid cooling penetration. The industry chain features cross-sector competition. Automotive component companies like Yinlun Co., Ltd., leveraging accumulated thermal management expertise, have entered the upstream segment of liquid cooling. The Company's products cover CDUs, cold plates, and immersion cooling equipment. In H1 2025, the Company's digital energy business revenue reached RMB692 million, up 58.9% yoy. Company Analysis:Core Business Grows Steadily, and Capital Structure Remains Manageable During Expansion

In the first three quarters of 2025, the Company reported revenue of RMB11,057 million, up 20.12% yoy; net profit attributable to the parent company was RMB672 million, up 11.18% yoy. In Q3 2025 alone, the revenue was RMB3.89 billion, up 27.38% yoy, and net profit attributable to the parent company was RMB230 million, up 14.5% yoy.

The gross margin for the first three quarters was 19.30%, down 0.77 ppts yoy, mainly due to tariff pressures, OEM price reductions, and a one-off accounting standard adjustment. The period expense ratio showed some fluctuation: Driven by the accelerated globalisation strategy, expenses for developing overseas and emerging markets increased, leading to a 0.26 ppts yoy rise in the selling expense ratio to 1.61%. Administration and R&D expense ratios were 4.97% and 3.94%, down 0.39 and 0.77 ppts yoy, respectively, reflecting effective refined management and cost control. Benefiting from increased exchange gains due to exchange rate movements, the financial expense ratio fell significantly by 0.24 ppts to 0.25%.

By business segment, according to the Company's H1 2025 interim report, the revenue contributions from commercial vehicles and off-road/passenger vehicles and new energy/digital and energy thermal management businesses were 33.84%, 53.49%, and 9.65%, respectively. In terms of revenue growth, the first business line remained stable (+3.9%), the second showed rapid growth in the low-to-mid double digits (+20.5%), and the third sustained high growth in the mid-to-high double digits (+58.9%).

In terms of BS, the net cash flow from operating activities in the first three quarters of 2025 was a net inflow of RMB701 million, higher than net profit, but down 20.71% yoy, mainly due to increased pressure on receivables and bill collections. The Company is in a phase of high capital expenditure and expansion. As of the end of September 2025, total assets stood at RMB20,634 million, with a debt ratio of 62.5%, indicating a manageable capital structure.

Global Capacity Deployment Accelerates, and New Projects Continue to Advance

The Company continues to implement its "domestic + overseas" global strategy. The Southwest China intelligent manufacturing base in Sichuan (investment of RMB378 million) focuses on water-cooled plates and front-end modules, serving clients such as Chery. The Mexico base (investment of RMB269 million) targets the North American market, with a construction period from January 2026 to July 2027. In addition, the Company's overseas factories have begun to yield results. In H1 2025, the North American plant reported revenue of RMB790 million and net profit of RMB30 million; the European plant is expected to achieve full-year turnaround.

During 2024, the Company secured more than 300 new projects, which, once fully ramped up over their life cycles, are expected to contribute additional annual sales revenue of approximately RMB9,073 million. In H1 2025, more than 200 new projects were secured, expected to generate an additional RMB5,537 million in annual revenue once in full production.

The Third Line: Liquid Cooling of the Data Centre Enters Volume Expansion Phase, Strengthened by Technological Moat

The product portfolio of the Company's digital energy business covers CDUs, cold plates, and integrated immersion liquid cooling equipment, forming a layout of "systems + primary/secondary cooling sources + components". In November 2025, the Company plans to acquire a 55% stake in Syslab, enhancing capabilities in controllers and drivers, aiming to transform from "thermal management hardware" to "thermal management + intelligent control" integrated systems. This supports the modular CDU products for data centre liquid cooling. Overseas, the Company plans an additional investment of RMB269 million to build the Mexico base, serving North American commercial vehicle and data centre clients, with production expected in 2027.

The Fourth Line: Establishment of the ŕ+4+N" Framework for Humanoid Robots, Strategically Positioned in Embodied Intelligence

The Company has defined a framework of ŕ cognitive system + 4 major modules (thermal management, rotary joints, actuators, and dexterous hands) + N key components" and established a joint venture, Suzhou Yizhi Dexterous Drive Technology Co., Ltd., with its partners to focus on developing dexterous hands. In October 2025, the Company confirmed supply cooperation for certain product categories with key clients. Although the business is still in an early stage, the technological approach is highly synergistic with the Company's thermal management capabilities. If mass production occurs in 2026--2027, this business line could become a new source of valuation upside. Investment Thesis & ValuationYinlun is transitioning from a leader in automotive thermal management to a global core supplier for liquid cooling in digital energy. It is deeply integrated with top-tier clients, with new overseas bases about to begin production. Its dual positioning in technology and capacity captures the global AI computing thermal management opportunity, while its robot thermal management segment opens up a new growth curve.

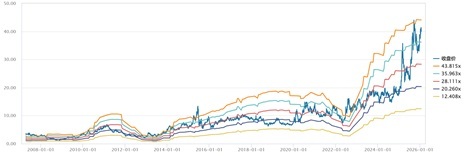

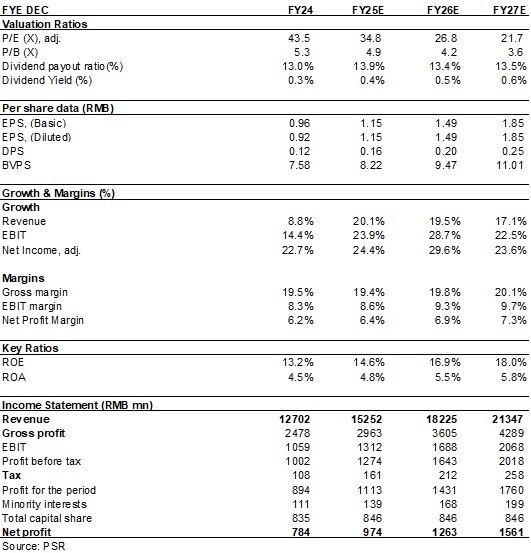

As analyzed above, we expected diluted EPS of the Company to RMB 1.15/1.49/1.85 of 2025/2026/2027. And we accordingly gave the target price to 46.3, respectively 31x P/E for 2026. "Accumulate" rating. (Closing price as at 23 January) Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research Financials

(Closing price as at 23 January)

Click here to download PDF version...

| Recommendation on 28-1-2026 | | Recommendation | Accumulate (Initiation) | | Price on Recommendation Date | $ 40.050 | | Suggested purchase price | N/A | | Target Price | $ 46.300 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|