|

SKB BIO-B(6990)

Analysis¡G

Kelun-Biotech is primarily engaged in the biopharmaceutical business, focusing on oncology, autoimmune diseases, and metabolic diseases. It currently has over 10 ADC and novel conjugate drug assets in clinical or higher stages, including sac-TMT (Jia Tai Lai), which has obtained marketing approval for two indications, and trastuzumab botidotin (Shu Tai Lai) for HER2+ BC, which has reached the NDA stage. In November 2024, sac-TMT was approved by the National Medical Products Administration (NMPA) for listing in China, for the treatment of adult patients with unresectable locally advanced or metastatic TNBC who have previously received at least two systemic therapies (with at least one targeted at the advanced or metastatic stage). Sac-TMT is the first domestically produced ADC with global intellectual property rights to receive full approval for marketing, and the group has begun its commercialization.

In March 2025, the group obtained NMPA approval for sac-TMT for the treatment of adult patients with EGFR mutation-positive locally advanced or metastatic non-squamous NSCLC who have progressed after EGFR-TKI treatment and platinum-containing chemotherapy. Compared to docetaxel, sac-TMT monotherapy shows statistically significant and clinically meaningful improvements in ORR, PFS, and OS. This is the world¡¦s first TROP2 ADC drug approved for marketing in the LC field. In May 2025, the NDA for sac-TMT for the treatment of adult patients with unresectable locally advanced or metastatic HR+/HER2- BC who have previously received endocrine therapy and other systemic treatments in the advanced or metastatic stage was accepted by the NMPA and included in the priority review and approval process.

In December 2025, the group announced a strategic partnership with Crescent Biopharma to jointly develop and commercialize oncology treatments. Under the terms of the collaboration, the group grants Crescent exclusive rights to research, develop, manufacture, and commercialize the group¡¦s antibody-drug conjugate SKB105 in the United States, Europe, and all markets outside Greater China. The group will receive an upfront payment of $80 million from Crescent and is eligible for milestone payments of up to $1.25 billion, as well as tiered royalties in the mid-single to low-double digit percentages based on net sales of SKB105. This collaboration complements and strengthens the group¡¦s differentiated oncology R&D pipeline by introducing Crescent¡¦s tetravalent bispecific antibody, while also accelerating the global development process of SKB105, enhancing its potential commercial value, and expanding the group¡¦s global partnership network. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $475.00, Target Price: $520.00, Cut Loss Price: $450.00

|

JUNEYAO AIRLINE(603885.CH)

Analysis¡G

he company is a full-service airline with Shanghai as its primary hub and Nanjing and Chengdu as secondary hubs, ranking among the leading private airlines. It wholly owns a low-cost carrier, 9 Air, based in Guangzhou, achieving comprehensive coverage of the high, medium, and low-end passenger markets. The company has implemented a development strategy featuring dual brands and dual hub operations. From Q1 to Q3 2025, the company's revenue reached 17.48 billion yuan, remaining roughly flat yoy, while net profit attributable to the parent company stood at 1.09 billion yuan, down 14% yoy, primarily due to the impact of Pratt & Whitney engine maintenance delays on aircraft utilization. Looking ahead, 9 Air plans to introduce 5-6 aircraft annually from 2027 to 2028, with effective capacity expected to grow significantly over the next three years. As aircraft utilization gradually improves, performance is anticipated to exceed expectations and recover.

Strategy¡G

Buy-in Price: $14.95, Target Price: $16.75, Cut Loss Price: $14.00

|

|

Desay SV (002920 CH) - Continuous Updates of Intelligent Products

Investment SummaryCompany profile

Desay SV, established in 1986, is a leading company in the automotive electronics field, with its main products including intelligent cockpits, intelligent driving, and connected services. As the cornerstone of the company's revenue, the intelligent cockpit generated a revenue of RMB18.23 billion in 2024, (RMB, the same below), accounting for 66.01% of total revenue. The intelligent driving business also saw growth, with 2024 revenue reaching RMB7.314 billion, a yoy increase of 63.06%, accounting for 26.5%. The company's total revenue in 2024 amounted to 27.618 billion yuan, up 26.06% yoy, with a net profit of 2.005 billion, up 29.62% yoy.

Strong Performance in the First Three Quarters

In the first three quarters of 2025, the Company achieved revenues/net profits/net profits excluding non-recurring items of RMB22.337 billion/RMB1.788 billion/RMB1.724 billion, marking yoy increases of 17.72%/27.08%/19.02%, respectively. The gross margin was 19.70%, down 0.5 percentage points yoy. In the third quarter of 2025 alone, the company achieved revenues/net profits/net profits excluding non-recurring items of RMB7.692 billion/RMB0.565 billion/RMB0.571 billion, marking yoy increases of 5.63%, but a decline of 0.57% and 13.25%, respectively. Compared to the previous quarter, revenues/net profits/net profits excluding non-recurring items decreased by 2.04%, 11.74%, and 12.86%, respectively. The third-quarter performance declined quarter-on-quarter, mainly due to the decrease in sales from the core customer Li Auto and industry-wide price reduction pressures. However, with the upcoming launch and delivery of new models such as the Li Auto i6 and Xpeng X9 in the fourth quarter, it is expected that the increase in sales driven by the launch of multiple new models will improve performance in the fourth quarter.The quarter-on-quarter decline in performance was mainly influenced by lower sales of core customer Li Auto's vehicles and price reduction pressures in the industry. However, with the upcoming launch and delivery of new models such as the Li Auto i6 and XPeng X9 in the fourth quarter, it is expected that the increase in sales from these new models will improve fourth-quarter performance.

Ongoing Investment in R&D, Continuous Updates of Intelligent Products, Leading the Industry

In 2024, the company's R&D expenses were RMB2.256 billion, accounting for 8.17% of revenue. In the first three quarters of 2025, R&D expenses amounted to RMB2.003 billion, accounting for 8.97% of revenue. The continued increase in R&D investment has provided strong support for new technologies and products. 1) Intelligent Cockpit: The company's fourth-generation intelligent cockpit has been scaled up for mass production in collaboration with Li Auto, Xiaomi Auto, and Geely Auto, and has continued to receive new project orders from GAC Passenger Cars, Geely Auto, and GAC Aion. The fourth-generation flagship intelligent cockpit domain controller is now in mass production for Chery Auto. The fifth-generation intelligent cockpit platform has secured new project orders from Li Auto and attracted attention from several top global OEMs. The company's HUD (Head-Up Display) first mass production project has been launched, marking a significant breakthrough in the intelligent driving visual field. New project orders have been received from Shanghai GM, GAC Passenger Cars, and Dongfeng Nissan. 2) Intelligent Driving: In the field of advanced driver-assistance systems (ADAS), the company continues to maintain the highest market share in China and continuously optimizes and upgrades its products to meet the needs of different vehicle levels. Several flagship ADAS domain controllers have been mass-produced and successfully delivered to prominent clients such as Xiaomi Auto, Li Auto, Great Wall Motors, XPeng Motors, GAC Toyota, Geely Auto, and GAC Aion. New project orders have been received from Great Wall Motors, Geely Auto, Chery Auto, GAC Aion, and Dongfeng Passenger Vehicles. The company also offers several lightweight ADAS solutions for mid- to low-priced vehicles, the largest segment of the market, and has secured new project points from major clients such as GAC Toyota, Chery Auto, and Toyota. These solutions will be promoted to more customers. 3) Connected Services: The company has successfully achieved mass production of UWB (Ultra-Wideband) and BLE (Bluetooth Low Energy) solutions, becoming the first supplier in China to implement UWB solutions. This first-mover advantage has helped the company win key client collaborations with Li Auto and Chery Auto. Successful Fundraising, Capacity ExpansionIn October, the company completed a private placement of A-shares, raising a net amount of RMB4.393 billion. The funds are intended for investment in projects such as the Desay SV automotive electronics base in Central and Western China (Phase I) (RMB1.699 billion), intelligent automotive electronic system-level component production (RMB1.974 billion), and the intelligent computing centre and cockpit integration platform R&D (RMB0.72 billion). The company expects the first two projects, once completed, will add annual revenues of RMB8.276 billion and RMB14.773 billion, respectively, and net profits of RMB0.59 billion and RMB1.187 billion, significantly boosting the company's long-term growth potential and reinforcing its leadership position in the automotive electronics sector. Deepening International Strategy, Building Ecosystem CollaborationThe company has strengthened its strategic partnerships with global core chip manufacturers and OEMs, successfully securing new project orders from clients such as VW and Toyota, and making breakthroughs with white-spot clients such as Renault and Honda. The company has also established overseas branches in major countries and regions such as Germany, France, Spain, Japan, and Singapore. Regarding overseas production capacity, in May 2025, the company began contributing production capacity in Indonesia, strengthening the supply chain resilience and delivery capabilities in Southeast Asia. In June 2025, the Monterrey plant in Mexico launched its first mass production project, offering more efficient localized service guarantees for the Americas market. The smart factory in Spain is expected to begin mass production in 2026, providing cutting-edge intelligent products for the intelligent cockpit and ADAS fields in Europe. In the first half of 2025, the gross margin of overseas operations reached 28.93%, up 8.22 percentage points yoy, exceeding the domestic gross margin by 9.26 percentage points. The expansion of overseas production capacity will provide strong support for profit growth. Unmanned Vehicle Launch, Expanding into New BusinessesOn September 2, the company launched the "Chuanxing Zhiyuan" vehicle-grade unmanned vehicle brand in Shanghai. Entering the unmanned vehicle field is an extension of the company's core capabilities. The first product, the S6, features a vehicle-grade fully-controlled chassis and modular upper structure. Based on the S6 platform, the vehicle is capable of serving various scenarios such as industrial parks, logistics parks, agricultural trade distribution, express delivery, supermarket distribution, store restocking, fresh food distribution, and pharmaceutical delivery. The S6 series of low-speed unmanned vehicle products has already received multiple customer orders. Investment ThesisThe Company is a leader in automotive electronics, benefiting from continuous investment in R&D to maintain its technological leadership, while also actively exploring new businesses. We remain highly optimistic about the company's growth prospects.

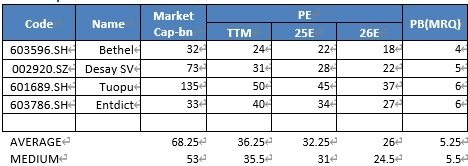

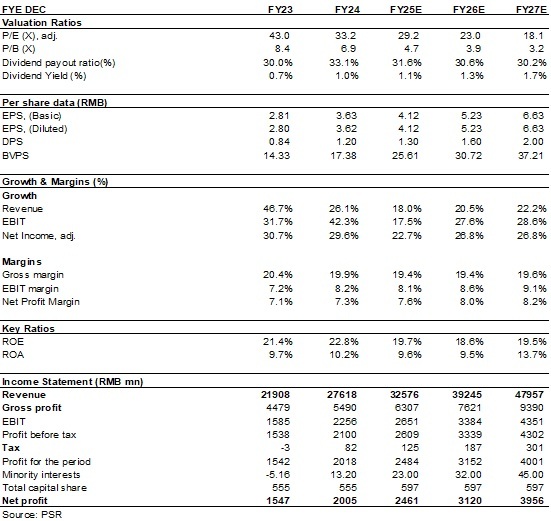

As for valuation, we expected diluted EPS of the Company to RMB 4.12/5.23/6.63 of 2025/2026/2027. And we accordingly gave the target price to RMB147, respectively 35.7/28.1/22.2x P/E for 2025/2026/2027. "Buy" rating. (Closing price as at 31 December 2025) Peer Comparison

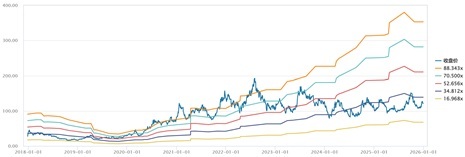

Source: Wind, Phillip Securities Hong Kong Research PE BAND

Source: Wind, Phillip Securities Hong Kong Research RiskProgress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices Financials

(Closing price as at 31 December 2025)

Click here to download PDF version...

| Recommendation on 13-1-2026 | | Recommendation | Buy (Initiation) | | Price on Recommendation Date | $ 120.300 | | Suggested purchase price | N/A | | Target Price | $ 147.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|