|

KB LAMINATES(1888)

Analysis¡G

Kingboard Laminates possesses a complete vertically integrated supply chain and a vast customer network, benefiting from the sustained growth in demand for electronic products and the rapid development of high-end fields such as AI. The demand for emerging electronic products centered around AI concepts is strong, leading to an upward trend in the prosperity of the upstream and downstream businesses in the copper clad laminate industry chain. The Group¡¦s sales proportion of high-end, high-value-added products continues to increase to adapt to market demand changes, with improved capacity utilization and stacked product price adjustments, driving growth in revenue and profit for the copper clad laminate division. For the first half year ended June 30, 2025, the Group¡¦s revenue increased by 11% year-on-year to HK$9.588 billion, and net profit attributable to shareholders rose 28% to HK$933 million.

Given the trend toward small-batch, diversified development in the copper clad laminate market, the Group is actively researching and developing new products to meet diverse customer needs in terms of performance and price, while continuously exploring new market segments, achieving ideal progress in optimizing its product portfolio. Data centers and cloud computing have driven a significant increase in the use of thick copper foil. The latest phase of copper foil capacity in Lianzhou, at 1,500 tons per month, was fully operational in the first half of 2025, greatly enhancing the Group¡¦s cost efficiency. Additionally, thanks to an experienced management team that continuously improves production technology to boost efficiency and reduce energy consumption, while enhancing production equipment automation to cut personnel expenses, profit before interest, taxes, depreciation, and amortization rose 3% to HK$1.607 billion.Looking ahead, the rise of AI technology is driving the vigorous development of multiple industry chains, including cloud data centers, robotics, autonomous driving, and smart wearable devices, as well as the continuous upgrade of high-speed networks, all of which will stimulate demand for electronic products and become a growth driver for copper clad laminate demand. High-performance, high-reliability, and high-stability premium copper clad laminates will become the mainstream demand in the future electronics market. The Group will actively promote market share for mid-to-high-end products such as high-frequency high-speed, medium-high heat resistance, halogen-free, and prepreg materials. The Group¡¦s heavily invested copper clad laminate R&D center has successfully developed various high-frequency high-speed products applicable to GPU motherboards in AI servers, and through vertical industry chain synergies, has successfully developed HVLP3 copper foil for AI servers and ultra-thin VLP copper foil for IC packaging substrates.

In high-end communication fields, especially in 5G, 6G communications, and AI servers, low-dielectric glass fiber yarn is currently in short supply. The Group¡¦s first kiln for producing low-dielectric glass fiber yarn, located in Qingyuan City, Guangdong Province, commenced production in the first half of this year. In the second half, three additional kilns will be added to produce low-dielectric glass fiber yarn, including higher-value-added second-generation low-dielectric glass fiber yarn, to meet the requirements for high computing power driven by 5G, 6G communications, and AI development. At the same time, in 2026, another specialty glass fiber yarn factory will be built in the park, with six kilns put into production for low-dielectric, low-expansion, and quartz glass fiber yarn to expand the Group¡¦s market share in high-end products. Additionally, the project in Shaoguan City, Guangdong Province, with an annual output of 70,000 tons of electronic-grade glass fiber yarn and 96 million meters of electronic-grade glass fiber cloth, will commence production in the second half of 2026, alleviating capacity bottlenecks for downstream products upon completion. Overseas, the Group expanded copper clad laminate capacity in Thailand by 400,000 sheets per month in 2024, reaching 1 million sheets per month by the end of 2024. Subsequently, it will continue to add two phases of 400,000 sheets each in Thailand, reaching a total capacity of 1.8 million sheets, making the Group the largest copper clad laminate producer in Southeast Asia. This capacity expansion can support the growing demand from overseas clients, including the overseas operations of Kingboard Holdings (148)¡¦s printed circuit board companies.(I do not hold the aforementioned stock)

Strategy¡G

Buy-in Price: $12.60, Target Price: $14.00, Cut Loss Price: $11.90

|

XINTE ENERGY(1799)

Analysis¡G

Xinteenergy is a leading high-quality polycrystalline silicon manufacturer, with its core business encompassing the production and sales of polycrystalline silicon, as well as the EPC and operation of photovoltaic/wind power stations. It is a subsidiary spun off from TBEA's new energy sector for separate listing on the Hong Kong stock exchange, with TBEA holding a 66.5% stake in the company. In H1 2025, the revenue structure showed that the polycrystalline silicon business accounted for 50%, while the construction and operation of photovoltaic/wind power stations contributed 27% and 11% respectively, with electrical equipment and other segments making up 12%. Affected by the cyclical downturn in the photovoltaic industry, the company incurred a significant loss of 3.9 billion yuan (RMB, same below) in 2024. In H1 2025, due to reduced impairment and increased investment income, the company reported a loss of 260 million yuan, narrowing by 71% yoy. Notably, the company achieved a profit of 70 million yuan in Q2 2025, marking a turnaround from the previous quarter. Under industry policies aimed at curbing internal competition and enforcing minimum cost sales, industry output has declined for the first time in 12 years. The tax-inclusive price of polycrystalline silicon dense material surged from a July low of 35,000 yuan per ton to approximately 60,000 yuan this week. The PV industry is expected to recover in 2026, with leading companies likely to see a significant rebound in performance.

Strategy¡G

Buy-in Price: $7.51, Target Price: $8.73, Cut Loss Price: $6.80

|

|

CATL (3750 HK) - Multi-Product Momentum Drives Continued Performance Improvement

Company ProfileContemporary Amperex Technology Co., Limited ("CATL") is a global leader in the supply of power battery systems, focusing on the research and development, production, and sales of power battery systems and energy storage systems for new energy vehicles. Its main businesses include power battery systems, energy storage systems, and lithium battery material systems (mainly ternary precursors). Specifically, the power battery system comprises cells, modules, and battery packs, which are used in electric passenger vehicles, commercial vehicles, and other applications. In addition, CATL has entered the field of battery recycling through the acquisition of Brunp Recycling and invested in and held stakes in overseas lithium mines to secure ties with raw material suppliers, thereby achieving a closed-loop layout of the upstream and downstream industry chain. In 2024, the company ranked first in global power battery installations for the eighth consecutive year with a market share of 37.9%, and also ranked first for the fourth consecutive year in energy storage batteries with a market share of 36.5%. Investment SummaryStrong Growth Maintained in Q3 Results, Further Net Profit Margin Expansion, and Stable Per Unit Profitability

In the first three quarters of 2025, the Company reported revenue of RMB283.072 billion (RMB, the same below), up 9.28% yoy; net profit attributable to the parent company was RMB49.034 billion, up 36.20% yoy; net profit attributable to the parent company excluding non-recurring items was RMB43.619 billion, up 35.56% yoy. The strong performance was mainly driven by robust demand in the power battery and energy storage battery sectors, as well as expansion in overseas markets.

Operating cash flow amounted to RMB80.66 billion, up 19.6% yoy. The Company maintained abundant cash reserves, with cash and trading financial assets exceeding RMB360 billion at the end of the period.

In Q3 2025, the Company reported revenue of RMB104.186 billion, up 12.90% yoy and 10.62% quarter-on-quarter; net profit attributable to the parent company was RMB18.549 billion, up 41.21% yoy and 12.26% quarter-on-quarter; net profit attributable to the parent company excluding non-recurring items was RMB16.422 billion, up 35.47% yoy and 6.85% quarter-on-quarter.

The Q3 gross margin was 25.8%, largely flat quarter-on-quarter; net profit margin was 19.1%, up 4.1 ppts yoy. The rise in lithium carbonate market prices led to a yoy decrease in impairment losses, significantly boosting performance. Per unit gross profit and net profit for batteries remained relatively stable quarter-on-quarter. In addition, revenue from technology licensing continued to increase, reflecting recognition of the Company's technologies and patents.

Rapid Growth in Production and Sales Volume, Stable Market Position, and Accelerated Global Capacity Deployment

In the third quarter, the Company's total shipment volume of power and energy storage batteries approached 180GWh, representing a yoy increase of nearly 40% and a quarter-on-quarter increase of nearly 20%. Energy storage accounted for approximately 20% of total shipments, while overseas exports also accounted for about 20%. Inventory at the end of Q3 increased by RMB8 billion quarter-on-quarter to exceed RMB80 billion, primarily due to products in transit resulting from business expansion and preparation for future deliveries. Inventory turnover days remained stable.

The Company's market position remains solid. According to data from SNEResearch, the Company accounted for 36.8% of global power battery installation volume from January to August 2025, maintaining its position as the global leader. According to data published by the China Automotive Power Battery Industry Innovation Alliance, the Company's domestic market share of power battery installation volume was 42.75% from January to September 2025, continuing to lead the industry.

Q3 capital expenditure reached RMB9.875 billion, remaining at a high level. Full-year CAPEX is expected to increase compared to last year. With strong market demand, the Company's overall capacity utilisation remained high, and it plans to continue investing in R&D for new products and technologies as well as new equipment.

During this period of strong capital expenditure, the Company's global capacity deployment has accelerated. Its German plant commenced operations last year; construction of the Hungarian plant is progressing as planned, with Phase I exceeding 30GWh and expected to be completed, installed, and commissioned by the end of 2025, while Phase II is also advancing steadily. The Spanish plant has completed preliminary approvals, and the Indonesian plant is scheduled to commence operations in the first half of 2026. Multi-Product Momentum Drives Continued Performance ImprovementBenefiting from the growing economic viability of commercial vehicle electrification and the improvement of infrastructure, the domestic new energy commercial vehicle sector is experiencing rapid growth, with an electrification rate reaching 23%. The Company's shipments of commercial power batteries have grown rapidly, with their share gradually increasing to approximately 20% of total shipments. The Company is actively building a battery-swapping ecosystem for heavy trucks to accelerate their electrification.

In the passenger vehicle segment, the Company has launched the second-generation Shenxing ultra-fast charging battery, the Xiaoyao dual-core battery, and the new sodium-ion power battery for passenger cars. The future product mix is expected to further improve.

In the energy storage sector, the rapid expansion of global AI data centres has driven significant power demand, resulting in surging energy storage needs. The Company's current energy storage capacity is fully utilised, and capacity expansion is being accelerated, especially the mass production of the 587Ah energy storage product to meet market demand. The Company's 587Ah dedicated energy storage cell has achieved an optimal balance among three key elements---energy density, safety margin, and long lifespan---marking a milestone. Shipments of the 587Ah product are expected to gradually increase.

In the solid-state battery sector, small-scale production of all-solid-state batteries is expected to be realised in 2027. These breakthroughs in new technologies and the mass production of new products will help the Company adapt to future market changes and further strengthen its competitive advantage and industry-leading position.

On 17 December, CATL's world-first PACK production line for new energy power batteries featuring large-scale deployment of humanoid embodied intelligent robots officially commenced operation. The humanoid robot "Xiao Mo" is now capable of accurately completing complex tasks such as battery plug insertion, marking a breakthrough in the application of embodied intelligence in smart manufacturing. Future production lines will become increasingly intelligent, with continuously improving efficiency. Investment ThesisAccording to EVtank, global lithium battery shipments are projected to reach approximately 1899GWh in 2025, representing a yoy growth of about 23%, and are expected to exceed 5000GWh by 2030, with a compound growth rate of around 22%. As an industry leader, the Company is well positioned to fully benefit from the rapid growth in downstream demand. Its long-term investments in ecosystem innovation businesses offer substantial growth potential, and its first-mover advantage is expected to remain significant.

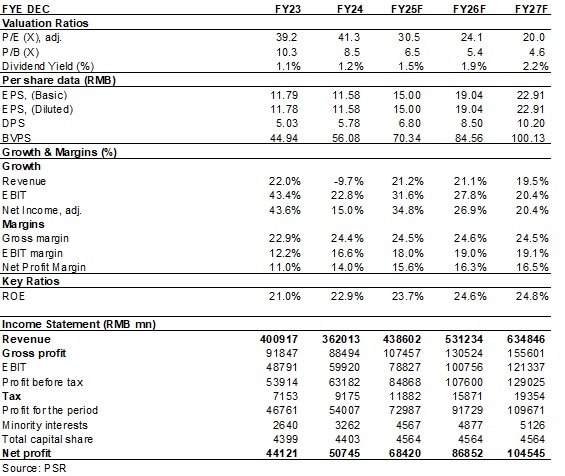

As for valuation, we expected diluted EPS of the Company to RMB 15.0/19.0/22.9 for 2025/2026/2027. And we accordingly gave the target price to HKD 635, respectively 38/30/25x P/E for 2025/2026/2027. "BUY" rating. (Closing price as at 29 December) RiskTechnical Iteration Risks

Raw material price fluctuation risk

The downturn in macroeconomics affects demand for end-use products

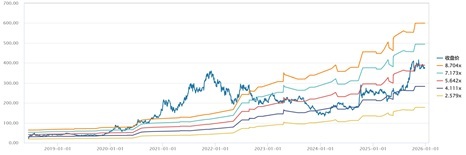

Geopolitics and Trade Policy Risks P/E Band trend for its A share

Source: Wind, Company, Phillip Securities Hong Kong Research Financials

(Closing price as at 29 December)

Click here to download PDF version...

| Recommendation on 30-12-2025 | | Recommendation | BUY (Upgrade) | | Price on Recommendation Date | $ 497.800 | | Suggested purchase price | N/A | | Target Price | $ 635.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|