|

INGDAN(400)

Analysis¡G

INGDAN is primarily engaged in the sale of integrated circuits and other electronic components. Leveraging its deep insight into upstream chip characteristics and downstream industry needs, the group has developed mature application solutions covering cutting-edge fields such as robotics, autonomous driving, and the low-altitude economy. These solutions effectively help customers lower technical barriers and accelerate product innovation. In terms of business model, the group has built a unique closed-loop ecosystem, driving a strategic upgrade from simple ¡§chip trading¡¨ to ¡§chip trading¡¨ to ¡§technology integration.¡¨ It provides customers with efficient supply-chain services, in-depth technical solutions, and customized products. Through innovative practices, the group has achieved a value leap from ¡§chip selection¡¨ to ¡§chip application,¡¨ delivering ¡§ready-to-use¡¨ core technology modules that significantly shorten customers¡¦ R&D cycles, allowing them to focus on differentiated innovation in their own applications and gain first-mover advantage in the market.

As a core supplier, the group is dedicated to connecting upstream AI chip technology with downstream innovation demand, focusing on two key areas: AI infrastructure and edge AI & devices. It offers AI chip application solutions, chip licensing and distribution, and self-developed AI products. Benefiting from massive demand for AI computing power, for the third quarter ended 30 September 2025, the group recorded revenue of approximately RMB 3.332 billion, up 22.1% year-on-year, and operating profit of RMB 127.9 million, up 34.7%. For the first nine months of 2025, revenue reached RMB 10.008 billion, a 42% increase year-on-year, with operating profit of RMB 303 million, up 24.8%.

The group recently received confirmation from the Hong Kong Stock Exchange for the proposed spin-off and separate A-share listing of its subsidiary, Comtech. As a core supplier in the AI computing-power supply chain, Comtech is deeply involved in the construction of global computing networks, serving data centers, AI servers, AI switches, optical modules, and a wide range of AI applications. It maintains close partnerships with leading global chip manufacturers and distributes products from more than 80 core chip companies, including international giants such as Nvidia, AMD-Xilinx, Intel, as well as many prominent domestic Chinese chip designers. Its main product lines cover GPUs, CPUs, FPGAs, ASICs, memory chips, software, and full-series related products. The proposed spin-off will better reflect the intrinsic value of Comtech, enhance operational and financial transparency, and allow it to directly and independently access equity and debt capital markets in mainland China while improving its ability to obtain bank financing. Meanwhile, the parent group will be able to fully concentrate on developing its AIoT business and deploying capital without needing to consider Comtech¡¦s funding requirements. (I personally hold no position in the stock.)

Strategy¡G

Buy-in Price: $2.95, Target Price: $3.15-3.30, Cut Loss Price: $2.80

|

CSPC PHARMA(1093)

Analysis¡G

In the first three quarters of 2025, CSPC 's revenue decreased by 12.3% year-on-year to 19.89 billion yuan, while net profit attributable to shareholders declined by 7.1% to 3.51 billion yuan. Notably, third-quarter revenue grew by 3.4% year-on-year to 6.62 billion yuan, and net profit attributable to shareholders surged by 27.2% to 964 million yuan. The rebound in Q3 2025 revenue was driven by two key factors: 1) the narrowing decline in authorized income after excluding it from the finished drug business, with the impact of the Duomisuo centralized procurement gradually dissipating; 2) the recognition of prepayments (approximately 465 million yuan in total) for collaborations with AstraZeneca's AI platform and certain Lp(a) small-molecule BD projects. CSPC 's core pipeline, including SYS6010 (EGFR ADC), KN026 (HER2 bispecific antibody), and idaglutide £\ (GLP-1 weight-loss drug), has all entered key registration phases. Among these, the GLP-1 product is expected to receive approval by the end of 2025 or in 2026, positioning CSPC to capture a billion-yuan weight-loss market. With multiple innovative drugs nearing commercialization, CSPC boasts robust long-term growth momentum.

Strategy¡G

Buy-in Price: $7.86, Target Price: $9.19, Cut Loss Price: $7.10

|

|

Daimay (603730 CH) - Expanding Roof Business to Open More Growth Potential

Investment SummaryFY2025 Q3 Remain Stable

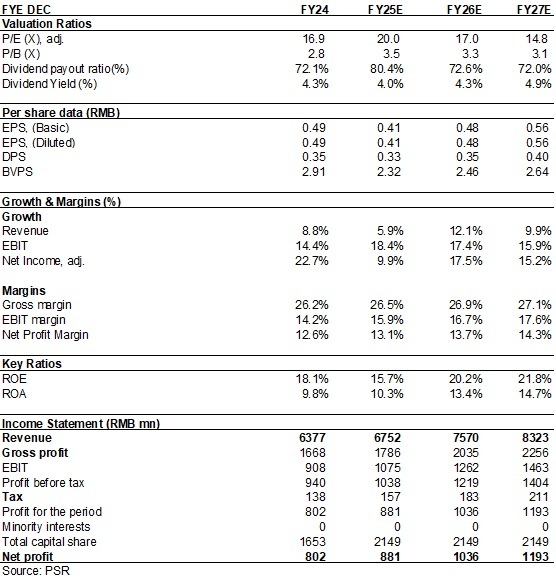

The Company released its Q3 2025 report: In the first three quarters of 2025, the company achieved revenue/net profit/net profit excluding non-recurring items of RMB 4.794 billion/RMB 445 million/RMB 600 million, representing yoy growth of -0.19%/-28.62%/-3.09%, with a gross margin of 28.04%, a yoy decrease of -0.22 percentage points. In Q3 2025 alone, the Company achieved revenue/net profit/net profit excluding non-recurring items of RMB 1.62 billion/RMB 203 million/RMB 198 million, which represents yoy increases of +6.65%/+0.24%/+0.75%.

Fire Impact in the First Half Gradually Eliminated

Despite a challenging overseas market in Q3, the performance of Daimay remain stable: From the demand of major auto markets in Q3 2025: North American vehicle sales were 5.104 million units, down slightly by 2.16% qoq; European passenger car registrations were 3.1136 million units, down by 9.33% qoq. However, the company's Q3 revenue/net profit excluding non-recurring items showed qoq increases of +2.38%/+0.83%, reflecting its stable operations. Additionally, a fire in the second quarter at the Company's Mexican plant led to non-operating expenses of USD 33.751 million, equivalent to RMB 242 million. These damaged assets are all covered under insurance claims. Daimay has submitted a claim letter to AXA Insurance and expects the final insurance compensation to cover the actual losses.

Expanding Roof Business to Open More Growth Potential

In 2023, Daimay issued convertible bonds to expand the production of roof and roof assembly products. The project has secured customer appointments, including 300,000 sets of automotive roof system integration products and 600,000 sets of automotive roof products at the Mexican Daimei facility, and 700,000 sets of automotive roof products at the Zhoushan Yindai facility. The company's main products, such as sun visors, headrests, and central roof controllers, have an equivalent per vehicle value of RMB 588. The roof products and roof integration system products from the convertible bond project have a per vehicle value of RMB 700 and RMB 4,000, respectively. This value increase will open up growth potential for Daimay's future performance. According to the prospectus of the convertible bonds, it is estimated that once the project reaches full capacity, Daimay's revenue will increase by RMB 844 million in the first year, accounting for 16.4% of Daimay's 2022 revenue, and by RMB 2.11 billion in the third year. On the net profit side, after the project reaches full capacity, net profit will increase by RMB 111 million in the first year, and RMB 289 million in the third year. Currently, the company's "Annual Production of 700,000 Roof Products" project has been completed, while the "Mexican Automotive Interior Parts Industrial Base Construction Project" is expected to be delayed from January 2025 to December 2026. Upon completion, it is expected to add 300,000 sets of automotive roof system integration products and 600,000 sets of automotive roof products annually. The capacity expansion will provide assurance for securing new orders from North American customers in the future. Company profileDaimay was established in 2001 and is a well-known manufacturer in the global automotive interior parts sector. Its main products include automotive interior components for roof systems and seat systems, such as sun visors, headrests, roof linings, central roof controllers, armrests, and other automotive interior products. Among these, the Company's core product, the automotive sun visor, ranks first globally in its segment, with a market share exceeding 40% in 2022. In 2024,Daimay reported a revenue of RMB 6.377 billion, a yoy increase of +8.8%, with 85.35% of the revenue coming from overseas markets. The net profit was RMB 802 million, a yoy increase of +22.66%. Investment Thesis & ValuationThe Company's business in the automotive sector remains stable, and the projects funded by the convertible bonds are about to contribute to revenues, providing momentum for performance growth. We are optimistic about the Company's development prospects.

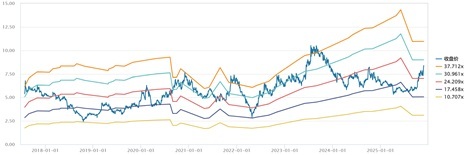

As analyzed above, we expected diluted EPS of the Company to RMB 0.41/0.48/0.56 of 2025/2026/2027. And we accordingly gave the target price to 9.17, respectively 19x P/E for 2026. "Accumulate" rating. (Closing price as at 25 November) Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research Financials

(Closing price as at 25 November 2025) Click here to download PDF version...

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|