|

Lopal Tech(2465)

Analysis¡G

As one of the world¡¦s leading suppliers of lithium iron phosphate (LFP) cathode materials, Lopal Tech has been aggressively expanding in the new-energy battery sector in recent years, signing multiple major long-term sales contracts focused on securing stable, long-term supply of LFP cathode materials. These contracts have not only solidified the company¡¦s position in the power battery and energy storage markets, but also driven significant breakthroughs in overseas markets. Building on the 260,000-tonne long-term supply agreement previously signed with LG Energy Solution, Lopal further entered into additional long-term supply agreements in January and June 2025 with Blue Oval Battery Park in Michigan (Ford¡VSK On JV) and Eve Energy Malaysia, respectively. These agreements further lock in overseas LFP cathode material sales volume from 2026 to 2030.

In China, in May 2025, Lopal¡¦s controlling subsidiaries Changzhou Liyuan and Nanjing Liyuan signed an LFP cathode material sales contract with subsidiaries of Cornex New Energy. Under the agreement, the sellers will supply a total of 150,000 tonnes of LFP cathode material to the buyer from 2025 to 2030, with monthly pricing to be determined according to the contract terms. Based on current estimated volumes and market prices, the total contract value is expected to exceed RMB 5 billion (final amount subject to actual orders and settlement). In November 2025, both parties signed ¡§Supplementary Agreement II¡¨, increasing the total committed volume to 1.3 million tonnes of LFP cathode material from 2025 to 2030. Based on estimated volumes and current market prices, the combined value of the original contract and Supplementary Agreement II is expected to exceed RMB 45 billion. This provides strong positive support for the Group¡¦s future performance and is expected to help the company turn from loss to profit.

The accelerated construction and progressive ramp-up of multiple production bases have formed a diversified and resilient supply system, enabling stable product delivery to customers, advancing the Group¡¦s vertical integration strategy, and further enhancing large-scale production capacity.

Notably, the Phase I 30,000 t/a LFP cathode material project in Indonesia has begun mass production in 2025, with product quality recognized by customers and stable supply to target markets already achieved. Construction of Phase II (90,000 t/a) in Indonesia is actively underway, marking a further significant expansion of the Group's overseas LFP cathode production capacity. (I do not hold any position in the above stock)

Strategy¡G

Buy-in price: HK$14.8 Target price :HK$16.5 Stop-loss price: HK$14

|

Willfar(3393)

Analysis¡G

The Company mainly engages in the business of intelligent measurement solutions, including electric intelligent measurement, communication and fluid (communication terminals and water, gas and heat) intelligent measurement, as well as the manufacturing and sales of intelligent distribution equipment. The Company has long been at the forefront of product procurement shares related to State Grid and Southern Power Grid. For the non-grid market, the company focuses primarily on the data center industry. Driven by the global explosion of generative AI, accelerated cloud computing penetration, and the implementation of digitalization strategies, this sector is poised to become a major engine for driving the company's performance growth. In the first half of 2025, the company achieved revenue of approximately RMB 4.39 billion, a yoy increase of 17%, with net profit attributable to the parent company surging by 33% yoy to RMB 440 million. The company's competitiveness in overseas markets continues to strengthen, with rapid growth in overseas revenue, increasing by 19.2% yoy to RMB 1.24 billion in the first half of the year, accounting for 30.8% of total revenue.

Strategy¡G

Buy-in price: HK$13.15 Target price : HK$15.7 Stop-loss price: HK$11.7

|

|

Company ProfileShanghai Baolong Automotive Corporation(Baolong or the "Company") started with tire valves. Later, following the automobile development trend, the Company continuously expanded the product line, and successively engaged in wheel weights, exhaust pipes, lightweight structural parts, TPMS (tire pressure monitoring system), as well as the intelligent automotive field of sensors, ADAS (that is, advanced driver assistance systems, mainly based on vision products and millimeter-wave radars), and air suspension. After more than 20 years of development, the Company is at the forefront of the segment in terms of the market share of its traditional business, namely, tire valves, wheel weights, exhaust pipes, and TPMS, which is currently the main source of revenue and profit. The Company's emerging business covers intelligent drive solutions-related parts and hydraulic lightweight structural parts, such as sensors, air suspension, and ADAS. The emerging business is currently the core direction of the Company's vigorous development, and will be an important growth point for future revenue and profit. Investment Summary

Revenue Maintains Rapid Growth, but Profitability is Weighed DownIn the first three quarters of 2025, Baolong achieved total revenue of RMB6.048 billion (RMB, the same below), representing a year-on-year increase of 20.32%. In terms of individual quarters, Q1/Q2/Q3 generated revenue of RMB1.905 billion, RMB2.045 billion, and RMB2.098 billion, respectively, reflecting year-on-year growth of 28.46%, 20.23%, and 13.85%.The company continues to experience rapid revenue growth, driven by steady year-on-year growth across most of its business segments. Notably, emerging businesses such as intelligent suspension systems and sensors are rapidly ramping up, while traditional businesses such as TPMS also recorded strong performance, demonstrating strong market expansion capabilities, especially in the areas of automotive intelligence and lightweighting.However, the company¡¦s net profit attributable to the parent in the first three quarters of the year was RMB198 million, a year-on-year decrease of 20.35%. The net profit after excluding non-recurring gains and losses stood at RMB132 million, a decline of 36.95%, indicating a clear squeeze on profitability. Specifically, the net profit attributable to the parent in Q1/Q2/Q3 was RMB95 million, RMB40 million, and RMB63 million, respectively, with year-on-year changes of +39.99%, -50.76%, and -36.92%.

The pressure on net profit is primarily due to the impact of price wars in the automotive market, which have affected upstream parts suppliers, as well as the negative effects of tariffs imposed by the United States.. Gross Margin Under Pressure in Q3, but Slight QoQ Improvement, which Expected Going ForwardDue to the factors mentioned earlier, coupled with the rapid growth of products with lower gross margins, such as air suspension systems and ADAS, which led to an increase in their proportion, the company¡¦s gross margin for the first three quarters of 2025 was 21.65%, a year-on-year decrease of 4.6 percentage points. However, the company has intensified cost control efforts, and the expanding revenue scale has led to economies of scale, with the period expense ratio decreasing by 3.3 percentage points year-on-year, reaching 16.33%.

In the third quarter of 2025, the company¡¦s gross margin was 21.34%, a year-on-year decrease of 3.26 percentage points, but a quarter-on-quarter increase of 0.86 percentage points. This indicates that cost pressures are easing at the margin, primarily due to the recovery in the proportion of high-margin products, the reduced impact of price cuts and rebates by automakers, and the decline in shipping costs from the previous peak caused by ¡§export rush¡¨ activities. The period expense ratio for the third quarter was 16.57%, a year-on-year decrease of 1.2 percentage points. With the upcoming agreements on tariff-sharing with customers, some tariff expenses may be backdated to revenue. Additionally, rebates for popular models are expected to be collected in due course, which is expected to drive further performance improvement in the coming quarters.Net cash outflow from investment activities reached RMB1.633 billion, with RMB649 million used for the purchase and construction of fixed assets and RMB983 million invested externally, indicating that the company is accelerating its capacity expansion and strategic positioning.

Air Suspension Business Has Abundant Orders, Emerging Business Expansion AcceleratesIn the first three quarters, according to business segment classification, the company¡¦s revenues from its major divisions¡XTPMS, automotive metal fittings, valve cores, air suspension, and sensors¡Xreached RMB1.822 billion, RMB1.121 billion, RMB618 million, RMB953 million, and RMB557 million, respectively, reflecting year-on-year growth of 13.1%, 0.35%, 5.1%, 51.7%, and 18.2%. The company has become one of the global leading suppliers in specialized fields such as valve cores, balance blocks, exhaust pipes, and TPMS.According to the company¡¦s official WeChat account, orders for its intelligent suspension business have exceeded expectations. As of the end of Q3, the cumulative orders for the intelligent suspension business surpassed RMB24.070 billion. With the strong sales of models such as the NIO ES8, ONVO L90, Li Auto i8, and BYD DENZA, the visibility for rapid growth in air suspension sales remains high.Additionally, the expansion of the sensor business and emerging businesses such as ADAS is also accelerating: COB-packaged cameras have passed the AEC-Q certification, and wheel speed sensors and height sensors have been selected by several leading domestic joint venture and independent brands as well as overseas brands, with mass production expected to start between Q4 2025 and 2027. As of the end of Q3, the cumulative orders for the ADAS business exceeded RMB6.870 billion.

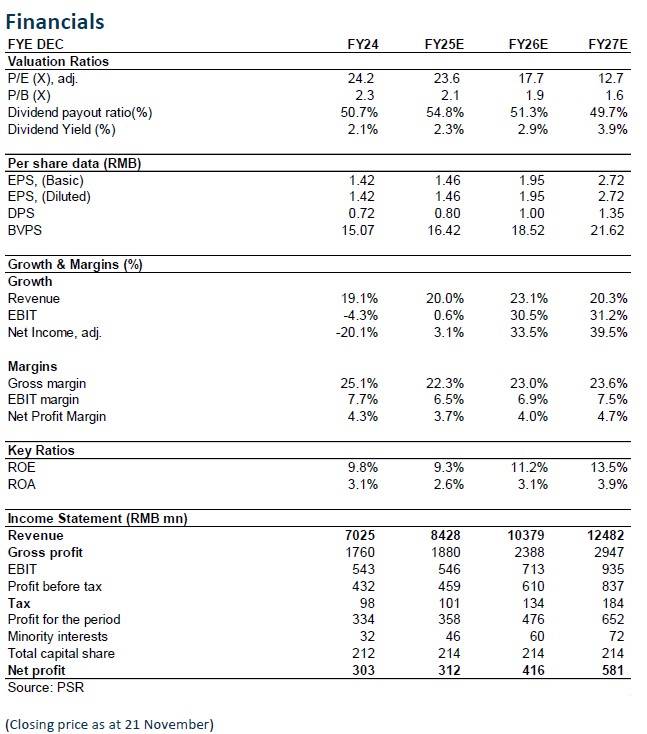

The company¡¦s overseas expansion is progressing steadily: the Thai factory is expected to begin mass production in Q1 next year; the second phase of the Hungarian production line is scheduled for equipment installation and commissioning by mid-next year, with mass production starting in Q1 2027; new projects in the U.S. and Mexico are also being actively pursued. The establishment of a global production capacity supply chain provides strong support for the company¡¦s future development.Investment Thesis & ValuationOverall, the company has strong growth momentum, but short-term profitability is impacted by disturbances from automotive price wars. In the medium to long term, benefiting from its forward-looking strategy and accumulated competitive advantages in emerging businesses, the company is expected to usher in a new growth cycle.As analyzed above, we expected diluted EPS of the Company to RMB 1.46/1.95/2.72 of 2025/2026/2027. And we accordingly gave the target price to 39, respectively 26.7/20/14.4x P/E for2025/2026/2027. "Accumulate" rating. (Closing price as at 21 November)

Financials

Current Price as of: Nov 21

Source¡G PSHK Est.

Download PDF version...

| Recommendation on 27-11-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 34.400 | | Suggested purchase price | N/A | | Target Price | $ 39.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|