|

AIA(1299)

Analysis¡G

AIA delivered an outstanding performance in the third quarter of 2025, with new business value reaching a record high of US$1.476 billion. On a constant exchange rate basis, this represented a 25% year-on-year increase, while on an actual exchange rate basis the growth was 27%, comfortably exceeding market expectations of US$1.405 billion. Double-digit growth was achieved in 11 of the Group¡¦s 18 markets, underlining AIA¡¦s continued strong expansion across Asia and the powerful momentum in its agency channel.During the quarter, the new business value margin rose to 58.2% on an actual exchange rate basis, an improvement of 6 percentage points compared with the same period last year, while annualised new premiums grew 15% to US$2.55 billion. For the first nine months of 2025, cumulative new business value reached US$4.314 billion, reflecting 18% growth on a constant exchange rate basis and 19% on an actual exchange rate basis. Over the same period, the new business value margin climbed 4.6 percentage points to 57.9%, and annualised new premiums rose 11% to US$7.492 billion.

The agency distribution channel remained the cornerstone of the Group¡¦s success, delivering 19% growth and contributing more than 70% of total new business value. Recruitment momentum stayed robust, with the number of new agents joining rising 18%, which in turn supported further expansion of the active agent force. The partnership distribution channels, comprising Hong Kong¡¦s independent financial adviser and broker networks together with the overall bancassurance business, recorded an impressive 46% increase in new business value.

By market, AIA Hong Kong posted 40% new business value growth, driven by strong demand from both local customers and Mainland Chinese visitors. AIA China achieved 27% growth, helping lift the nine-month figure for the Group by 5% year-on-year. Across the ASEAN region, new business value rose 15%, supported by double-digit advances in both agency and partnership channels. Thailand stood out with 20% growth, Singapore delivered strong gains powered by agency and partnership performance alike (with new agent recruitment up 9%), and Malaysia returned to overall growth in the third quarter thanks to improved agency productivity and continued double-digit contribution from partnership channels. Double-digit new business value increases were also recorded in South Korea, Vietnam, and India.

Demand for the Group¡¦s traditional protection and unit-linked products remained very healthy in local markets, enabling new business value margins to stay in line with the level reported for the first half of the year. AIA¡¦s continued emphasis on high-quality recruitment drove increases in both new agents and agency leaders.

From a technical perspective, AIA¡¦s share price has pulled back into its previous HK$70¡V77 consolidation zone and is now approaching the midpoint of that range near HK$73.5, which also coincides closely with the 100-day moving average. This level is regarded as an attractive entry point, with a price target of HK$80 and a stop-loss set at HK$70.(I do not hold the above stock.)

Strategy¡G

Buy-in price: HK$73.5,price target: HK$80, stop-loss price: HK$70

|

Jingfang Pharmaceutical(2595)

Analysis¡G

On November 11, the Drug Clinical Trial Registration and Information Publicity Platform showed that Jingfang Pharmaceutical has initiated a multicenter, open-label, randomized controlled Phase III clinical study to compare the efficacy, safety, and tolerability of GFH375 monotherapy versus investigator-choice chemotherapy in patients with KRAS G12D mutant metastatic pancreatic cancer who have undergone prior treatment. According to the company's prospectus, GFH375 is positioned as a frontrunner in the development of oral G12D inhibitors. The monotherapy of this product was approved in June 2024 to enter Phase I/II trials. GFH375/VS-7375 has already received FDA Fast Track designation this year for the first-line and later-line treatment of locally advanced, metastatic KRAS G12D mutant pancreatic ductal adenocarcinoma (PDAC). Earlier preclinical data of GFH375 monotherapy for solid tumors were disclosed at prestigious international academic conferences such as the ASCO and WCLC this year, in the form of Late-Breaking Abstracts (LBA) and oral presentations.

Strategy¡G

Buy price: HK$28,Target price: HK$30 ,Stop-loss price: HK$26.5

|

|

Vertiv (VRT.US) - Liquid Cooling Technology Presents New Growth Opportunities

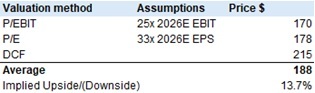

Company backgroundVertiv (VRT) designs, manufactures and services critical digital infrastructure for data centers (80% of net sales in 2024), communication networks (10%), and commercial and industrials (10%). Key products include critical infrastructure & solutions (AC & DC power management, integrated modular solutions, thermal management), integrated rack solutions (racks, rack power and power distribution, rack power distribution etc.), and management systems for monitoring and controlling digital infrastructure, integral to the technologies in services such as e-commerce, online banking, file sharing, video on-demand, energy storage, wireless communications, IoT and online gaming. The most prominent brands include Vertiv, Liebert, NetSure, Geist, Energy Labs, ERS, Albér, and Avocent. The company operates across three reportable segments: the Americas (56% of net sales in 2024); Asia Pacific (22%); and Europe, Middle East, & Africa (22%). Industry overviewVRT is operating in the data center infrastructure industry, a core sector supporting global digital transformation, primarily providing hardware facilities and technical services required for data storage, computation, and transmission in fields like the internet, cloud computing, and AI. The industry primarily generates revenue through the sale of key data center equipment, including power systems (e.g., 800VDC platform), cooling equipment (e.g., liquid cooling CDU units), server racks, and IT infrastructure. Taking VRT as an example, its 3Q25 revenue reached $2,676mn (82.8% of product sales), driven mainly by explosive demand from AI data centers for liquid cooling solutions and high-efficiency power products. VRT's role as the exclusive liquid cooling supplier in the NVIDIA-led COOLERCHIPS program further validates the profit potential of high value-added products.Capital expenditure by hyperscale operators and data centers grew by 55% in 2024 and is expected to increase by a further 56% in 2025. However, Vertiv's organic sales grew by only 18% in 2024, with projected growth of 26-28% in 2025. This indicates that the company is struggling to fully meet the surging market demand due to factors such as supply chain constraints and the typical positioning of cooling solutions later in the procurement cycle. As the backlog of unfilled orders continues to rise and stable capital expenditure supports the growth trajectory, the company's order volume continues to increase. Given that organic order volume is a core revenue driver, we forecast net sales growth of 27%/25% in 2025/2026 under the baseline scenario.According to Dell'Oro Group data, the liquid cooling market size is expected to approach $2 billion by 2027, with a compound annual growth rate of 60% during the period 2020-2027. The upgrade in cooling technology requires driving product structure optimization, allowing Vertiv to strengthen its pricing power and improve gross margins. However, the full manifestation of this effect depends on the pace of technological evolution, so its impact is relatively limited in the 2026 forecast. The breakthrough in microfluidics technology announced by Microsoft in September, which embeds liquid cooling directly inside chips, makes precise control of liquid flow paths within racks crucial. Amid the growing trend of hyperscale operators emphasizing independent intellectual property development, the company, with its unique positioning, can seize such high-value innovation opportunities and continue to serve as a core partner for the development, supply, and deployment of large-scale solutions. Company valuationData centers are placing higher demands on cooling solutions to support continuously increasing rack power densities. Current data centers commonly support rack power exceeding 20kW, but the market is moving towards levels above 50kW. The thermal density characteristics of new-generation CPUs and GPUs significantly exceed those of previous generations, while server manufacturers are packing more processing units into individual racks to meet the surging demands of high-performance computing and AI applications.Although the growth in order volume has been accompanied by a narrowing incremental profit margin, reflecting a weakening pricing power since the second quarter of 2024, signs of easing pressure have emerged. In the third quarter of 2025, the Americas region contributed 40% of the incremental operating profit margin, marking a strong reversal from the declining trend in incremental margins in the first half of the year. This was primarily due to the fading impact of raw material costs and tariffs. Management expects to largely offset the tariff impacts by the end of the first quarter of 2026. Accordingly, we set the incremental operating profit margin for the baseline 2025/2026 scenario at 23%/24%.Key assumptions in the DCF analysis:1. WACC: The capital structure consists of 67.6% debt and 32.4% equity, with a debt cost of 1.2%, an effective tax rate of 35.2%, and an equity cost of 27.2%.2. The discount period is from the fourth quarter of 2025 to the fourth quarter of 2026, calculated on a quarterly basis.3. The perpetual growth rate is 4.0%, based on the US GDP growth rate, converted to a quarterly growth rate of 1.0%.Considering the limitations of the DCF model, we employed three valuation methods, comparing this result with EV/EBIT and P/E valuations, and ultimately derived a target price of $188, initiating with an "Accumulate" rating.

Risk factors1) Intensifying competition;

2) Intensified trade friction;

3) Deteriorated market demand. Financials

Current Price as of: Nov 19

Source¡G PSHK Est. Download PDF version...

| Recommendation on 24-11-2025 | | Recommendation | Accumulate | | Suggested purchase price | $ 165 | | Target Price | $ 188.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|