Giordano(709) Analysis¡G Giordano¡¦s ¡§Digital-First¡¨ and ¡§Winning in Greater China¡¨ strategic initiatives continue to drive high-growth channel and market transformation. In Q3 2025, the Group recorded revenue of HK$894 million, down 1.4% year-on-year, but cumulative revenue for the first nine months still achieved 0.6% growth to HK$2.828 billion.Online revenue in Q3 surged 16.5% YoY to HK$134 million; cumulative online revenue for the first nine months reached HK$414 million, up 22.8% YoY. By region, despite unprecedented severe weather challenges in Greater China, the core business remained stable. Q3 revenue in Greater China was HK$407 million (flat YoY), while nine-month revenue rose 6.3% to HK$1.285 billion. The high-growth GCC (Gulf Cooperation Council) markets continued to shine, with Q3 revenue up 11.6% YoY to HK$164 million and nine-month revenue up 4.5% to HK$532 million.The Group actively optimized its product portfolio management, which led to a significant improvement in gross margin. As of 30 September 2025, inventory balance stood at HK$612 million (2024: HK$630 million), reflecting the Group¡¦s ongoing commitment to enhancing operational efficiency, aligning product supply with customer demand strategically, and maintaining strict procurement discipline and financial flexibility to capture emerging trends.Looking ahead, the Group will focus on pricing strategies across different channels to strike a balance between revenue growth and gross margin improvement, fully in line with its omni-channel strategy. By region, the Group is optimistic about the continued recovery and future growth prospects in Hong Kong and Macau. For its premium women¡¦s brand Giordano Ladies, the Group will further refine its positioning toward a more modern, relaxed, and business-casual ¡§Premium Elegance¡¨ style. The Korea Collection continues to deliver cross-market synergies, validating the feasibility of the ¡§One Giordano¡¨ cross-market collaboration strategy. The Group plans to introduce a wider variety of Korean series products into new markets. In Mainland China, the Group will fully restructure, reallocate resources, and revitalize operations to restore profitability. In the GCC markets, the Group will focus on product innovation and tailored marketing strategies that cater to the unique preferences of local consumers to further solidify its market position. Strategy¡G Giordano's ¡§Digital-First¡¨ and ¡§Winning in Greater China¡¨ strategic initiatives continue to drive high-growth channel and market transformation. In Q3 2025, the Group recorded revenue of HK$894 million, down 1.4% year-on-year, but cumulative revenue for the first nine months still achieved 0.6% growth to HK$2.828 billion.Online revenue in Q3 surged 16.5% YoY to HK$134 million; cumulative online revenue for the first nine months reached HK$414 million, up 22.8% YoY. By region, despite unprecedented severe weather challenges in Greater China, the core business remained stable. Q3 revenue in Greater China was HK$407 million (flat YoY), while nine-month revenue rose 6.3% to HK$1.285 billion. The high-growth GCC (Gulf Cooperation Council) markets continued to shine, with Q3 revenue up 11.6% YoY to HK$164 million and nine-month revenue up 4.5% to HK$532 million.The Group actively optimized its product portfolio management, which led to a significant improvement in gross margin. As of 30 September 2025, inventory balance stood at HK$612 million (2024: HK$630 million), reflecting the Group¡¦s ongoing commitment to enhancing operational efficiency, aligning product supply with customer demand strategically, and maintaining strict procurement discipline and financial flexibility to capture emerging trends.Looking ahead, the Group will focus on pricing strategies across different channels to strike a balance between revenue growth and gross margin improvement, fully in line with its omni-channel strategy. By region, the Group is optimistic about the continued recovery and future growth prospects in Hong Kong and Macau. For its premium women¡¦s brand Giordano Ladies, the Group will further refine its positioning toward a more modern, relaxed, and business-casual ¡§Premium Elegance¡¨ style. The Korea Collection continues to deliver cross-market synergies, validating the feasibility of the ¡§One Giordano¡¨ cross-market collaboration strategy. The Group plans to introduce a wider variety of Korean series products into new markets. In Mainland China, the Group will fully restructure, reallocate resources, and revitalize operations to restore profitability. In the GCC markets, the Group will focus on product innovation and tailored marketing strategies that cater to the unique preferences of local consumers to further solidify its market position. (I do not personally hold the above stock.)

Kuaishou(1024) Analysis¡G In the third quarter of 2025, Kuaishou's e-commerce business GMV increased by 15.2% year-over-year to RMB 385 billion. The live streaming business revenue rose by 2.5% from RMB 9.3 billion in the same period of 2024 to RMB 9.6 billion in the third quarter of 2025. During the third quarter of 2025, the average daily active users of the Kuaishou App exceeded 416 million, setting a new historical record.In the same quarter, Kuaishou launched Dynamic Canvas, upgraded its first-and-last-frame feature, and introduced a digital human solution. At the end of September 2025, Kuaishou released the Keling AI 2.5 Turbo model. The new model achieved significant improvements across multiple dimensions, including text response, dynamic effects, style consistency, and aesthetic quality. Just ten days after its release, the Keling AI 2.5 Turbo model simultaneously topped the global rankings for both text-to-video and image-to-video models on the renowned AI evaluation platform Artificial Analysis. While maintaining industry-leading content generation capabilities, the new model also reduced video generation inference costs through continuous engineering innovations, lowering the cost per video generated for creators by nearly 30.0%. This further enhanced the comprehensive cost-performance advantage of Keling AI. Strategy¡G Buy price: $64.95,Target price: $71.30,Stop-loss price: $58.80

Vertiv (VRT) designs, manufactures and services critical digital infrastructure for data centers (80% of net sales in 2024), communication networks (10%), and commercial and industrials (10%). Key products include critical infrastructure & solutions (AC & DC power management, integrated modular solutions, thermal management), integrated rack solutions (racks, rack power and power distribution, rack power distribution etc.), and management systems for monitoring and controlling digital infrastructure, integral to the technologies in services such as e-commerce, online banking, file sharing, video on-demand, energy storage, wireless communications, IoT and online gaming. The most prominent brands include Vertiv, Liebert, NetSure, Geist, Energy Labs, ERS, Albér, and Avocent. The company operates across three reportable segments: the Americas (56% of net sales in 2024); Asia Pacific (22%); and Europe, Middle East, & Africa (22%).

Industry overview

VRT is operating in the data center infrastructure industry, a core sector supporting global digital transformation, primarily providing hardware facilities and technical services required for data storage, computation, and transmission in fields like the internet, cloud computing, and AI. The industry primarily generates revenue through the sale of key data center equipment, including power systems (e.g., 800VDC platform), cooling equipment (e.g., liquid cooling CDU units), server racks, and IT infrastructure. Taking VRT as an example, its 3Q25 revenue reached $2,676mn (82.8% of product sales), driven mainly by explosive demand from AI data centers for liquid cooling solutions and high-efficiency power products. VRT's role as the exclusive liquid cooling supplier in the NVIDIA-led COOLERCHIPS program further validates the profit potential of high value-added products.Capital expenditure by hyperscale operators and data centers grew by 55% in 2024 and is expected to increase by a further 56% in 2025. However, Vertiv's organic sales grew by only 18% in 2024, with projected growth of 26-28% in 2025. This indicates that the company is struggling to fully meet the surging market demand due to factors such as supply chain constraints and the typical positioning of cooling solutions later in the procurement cycle. As the backlog of unfilled orders continues to rise and stable capital expenditure supports the growth trajectory, the company's order volume continues to increase. Given that organic order volume is a core revenue driver, we forecast net sales growth of 27%/25% in 2025/2026 under the baseline scenario.According to Dell'Oro Group data, the liquid cooling market size is expected to approach $2 billion by 2027, with a compound annual growth rate of 60% during the period 2020-2027. The upgrade in cooling technology requires driving product structure optimization, allowing Vertiv to strengthen its pricing power and improve gross margins. However, the full manifestation of this effect depends on the pace of technological evolution, so its impact is relatively limited in the 2026 forecast. The breakthrough in microfluidics technology announced by Microsoft in September, which embeds liquid cooling directly inside chips, makes precise control of liquid flow paths within racks crucial. Amid the growing trend of hyperscale operators emphasizing independent intellectual property development, the company, with its unique positioning, can seize such high-value innovation opportunities and continue to serve as a core partner for the development, supply, and deployment of large-scale solutions.

Company valuation

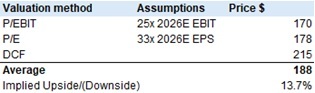

Data centers are placing higher demands on cooling solutions to support continuously increasing rack power densities. Current data centers commonly support rack power exceeding 20kW, but the market is moving towards levels above 50kW. The thermal density characteristics of new-generation CPUs and GPUs significantly exceed those of previous generations, while server manufacturers are packing more processing units into individual racks to meet the surging demands of high-performance computing and AI applications.Although the growth in order volume has been accompanied by a narrowing incremental profit margin, reflecting a weakening pricing power since the second quarter of 2024, signs of easing pressure have emerged. In the third quarter of 2025, the Americas region contributed 40% of the incremental operating profit margin, marking a strong reversal from the declining trend in incremental margins in the first half of the year. This was primarily due to the fading impact of raw material costs and tariffs. Management expects to largely offset the tariff impacts by the end of the first quarter of 2026. Accordingly, we set the incremental operating profit margin for the baseline 2025/2026 scenario at 23%/24%.Key assumptions in the DCF analysis:1. WACC: The capital structure consists of 67.6% debt and 32.4% equity, with a debt cost of 1.2%, an effective tax rate of 35.2%, and an equity cost of 27.2%.2. The discount period is from the fourth quarter of 2025 to the fourth quarter of 2026, calculated on a quarterly basis.3. The perpetual growth rate is 4.0%, based on the US GDP growth rate, converted to a quarterly growth rate of 1.0%.Considering the limitations of the DCF model, we employed three valuation methods, comparing this result with EV/EBIT and P/E valuations, and ultimately derived a target price of $188, initiating with an "Accumulate" rating.