|

JD HEALTH(6618)

Analysis¡G

JD Health delivered another quarter of strong growth in Q3 2025, with both revenue and profit significantly beating market expectations. The robust performance was primarily driven by strong sales of pharmaceuticals and nutraceuticals, deeper strategic partnerships, and the continued expansion of AI-powered healthcare applications.

For the period, JD Health recorded revenue of RMB 17.12 billion, up 28.7% year-on-year. Operating profit surged 125.3% to RMB 1.243 billion, while non-IFRS net profit rose 42.4% to RMB 1.902 billion. The group further strengthened synergies across its self-operated business, online marketplace, and instant retail channels, continuously expanding product supply, enhancing service experience, and maintaining price competitiveness.

JD Health continued to deepen cooperation with leading pharmaceutical companies and health product suppliers, winning greater user trust while creating new growth opportunities for its partners. In Q3 2025, the company signed strategic cooperation agreements with leading pharmaceutical companies including Eli Lilly, Innovent Biologics, Eisai China, and Bayer China. It also debuted a range of innovative drugs online, such as Eisai¡¦s originator drug DAYVIGO (Lemborexant Tablets), Hengrui Pharma¡¦s dry eye treatment Heng Qin (Perfluorohexyloctane Eye Drops), and Bayer¡¦s Talcid Lactulose, further solidifying JD Health¡¦s position as ¡§the Leading Online Marketplace for New and Specialty Medicine Launches.¡¨ Beyond pharmaceuticals, JD Health also hosted the initial launch for various nutrition and health supplement products, including Haleon¡¦s next-generation Centrum Silver vitamins and Sainte¡¦s Teai Benjia, China¡¦s first special medical purpose formula for phenylketonuria.

In September 2025, JD Health partnered with leading medical device brands such as Yuwell, Sinocare, and MicroTech to establish the intelligent interconnected ecosystem alliance. Leveraging JD Health¡¦s AI-powered system, the alliance is building an intelligent blood glucose management ecosystem that integrates monitoring, analysis, intervention, and follow-up care. The initiative will expand into blood pressure, ECG, respiratory oxygen therapy, and other areas in the future, aiming to create a full-lifecycle service ecosystem from disease prevention to chronic disease management, fully addressing users¡¦ long-term health needs. On the healthcare services front, the group will continue to expand its supply of high-quality professional resources¡Xincluding doctors, pharmacists, and nurses¡Xaccelerate the integration of online and offline health services, and deepen the application of artificial intelligence across multiple medical scenarios. (I do not personally hold the above stock)

Strategy¡G

Buy-in Price: $65.00, Target Price: $69.50-$75.00, Cut Loss Price: $61.50

|

SHANGHAI FUDAN(1385)

Analysis¡G

In the first three quarters of 2025, the company¡¦s operating revenue reached RMB 3.024 billion, a year-on-year increase of 12.7%. The revenue breakdown by product line is as follows: safety and identification chips approximately RMB 631 million, non-volatile memory approximately RMB 783 million, smart meter chips approximately RMB 386 million, FPGA and other products approximately RMB 1.116 billion, and testing service revenue (after consolidation adjustment) approximately RMB 108 million. Although revenue increased across all product lines, net profit attributable to shareholders declined by 25.63% to RMB 330 million. This was mainly due to increased inventory write-downs as demand for some products fell short of expectations and inventory aging lengthened. Additionally, changes in the supply chain and customer demand led to the write-off or impairment of some capitalized R&D projects, as they were no longer expected to deliver anticipated economic benefits. Furthermore, other earnings decreased due to a reduction in the value-added tax additional deduction for integrated circuit design enterprises and lower government subsidy approvals. On a positive note, net cash flow from operating activities surged by 263.30% year-on-year to RMB 419 million. Basic earnings per share were RMB 0.4, down 23.08% year-on-year. As a leading domestic FPGA and high-reliability chip company, Shanghai Fudan (1385.HK) is benefiting from recovering demand in the memory and high-reliability sectors, breakthroughs in automotive-grade products, and technological upgrades. Its performance in 5 shows signs of recovery, with clear long-term growth potential.

Strategy¡G

Buy-in Price: $40.70, Target Price: $46.28, Cut Loss Price: $39.10

|

|

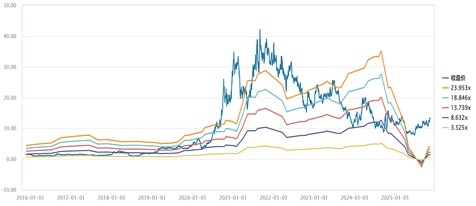

FLAT GLASS (6865 HK) - FY25Q3 Saw Significant Improve, as the Anti-Excessive Competition Measures Strengthened

Investment SummarySignificant Performance Improvement in Q3 2025

According to the Company's announcement, in the first three quarters of 2025, Flat Glass Group Co., Ltd. recorded revenue of RMB12.464 billion (RMB, the same below), down 14.7% yoy, and net profit attributable to the parent company of RMB638 million, down 50.8% yoy. Specifically, the Company recorded revenue of RMB4.079/3.658/4.727 billion in Q1/Q2/Q3, down 28.8%/26.4%/up 21.0% yoy and flat/-10.3%/up 29.2% qoq; net profit attributable to the parent company amounted to RMB106/155/376 million, down 86.0%/79.0%/up 285.5% yoy and up 136.7%/46.0%/142.9% qoq, respectively. The results showed a trend of improvement quarter by quarter, with particularly notable growth in Q3.

Anti-Excessive Competition Measures Strengthened, Driving Recovery in Profitability

The performance improvement was mainly driven by the accelerated inventory de-stocking that led to a recovery in industry prosperity, easing of cost pressures, and the support from overseas business (accounting for approximately 30%).

In 2025, the photovoltaic (PV) industry intensified its efforts to curb excessive competition. As of July 2025, the cold-repair capacity in the PV glass industry reached 7,750 tonnes/day, reducing the domestic operating capacity to 89 thousand tonnes/day---a decline of approximately 22.4% from the peak of 114.7 thousand tonnes/day in November 2024. This accelerated capacity reduction strengthened supply-side constraints, which supported PV glass price stabilisation. In July, prices bottomed out, followed by a rebound in August. In September, the price of 2.0mm PV glass rose 18% month-on-month to RMB13--13.5/sq.m, recovering approximately 25% from July's RMB10.5/sq.m.

The Company's gross margin for the first three quarters was 15.1%, down 3.9 ppts yoy. In Q3, gross margin reached 16.8%, up 10.8 ppts yoy and 0.1 ppt qoq, benefiting from increased shipments driven by price recovery, a decline in soda ash costs, and support from high-margin overseas business. The Q3 period expense ratio stood at 6.9%, down 3.7 ppts yoy and 0.6 ppt qoq, mainly attributable to scale effects. Additionally, a reversal of asset impairment losses of RMB80 million in Q3 further boosted profit. As a result, the Q3 net profit margin attributable to the parent company rose to 7.96%, up 13.2 ppts yoy and 3.7 ppts qoq.

Industry Expected to Maintain Weak Balance in Q4

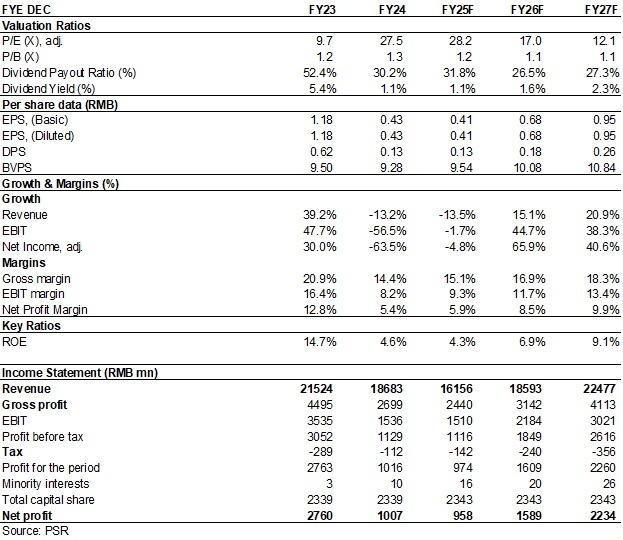

As of early November 2025, PV glass prices declined slightly due to weakening demand support, and industry inventories showed an increasing trend. The mainstream transaction price for 2.0mm PV glass was around RMB12.5--13/sq.m. However, considering the onset of the heating season and the resulting increase in natural gas prices, cost support is expected to limit the extent of price fluctuations. Benefiting from its advantages in technology, scale, capital, and clientele, the Company's cost advantages will become more prominent as market prices decline, potentially leading to an expansion in market share. The Company showed a clear downward trend in inventory in Q3. As of the end of Q3 2025, the Company's inventory balance stood at approximately RMB1.207 billion, down RMB751 million qoq, with a possible slight rebound in Q4. As of the end of September 2025, the Company's cumulative operating capacity totalled 16,400 tonnes/day, down 15% from the beginning of the year. The Company's two lines in Anhui (2,400 tonnes/day) and four lines in Nantong (4,800 tonnes/day) will commence operation based on market conditions. The two new production lines in Indonesia (3,200 tonnes/day) are expected to have a long construction period and will not commence production for at least two years. Investment ThesisDespite short-term pressure on industry prices, as a leading PV glass manufacturer, Flat Glass remains an industry leader in both scale and profitability. With continuous expansion of its overseas capacity, its profitability is expected to reach new heights. We expected the company's EPS for 2025/2026/2027 to be 0.41/0.68/0.95 yuan, respectively, and adjust the target price to HK$14.4, corresponding to a valuation ratios of 32.3/19.5/13.8x P/E and 1.4/1.3/1.2x P/B for the respective years, with an downgrade rating to "Accumulate." (Closing price as at 13 November 2025) P/E Band

Source: Wind, Phillip Securities Hong Kong Research Financials

(Closing price as at 13 November 2025) Click here to download PDF version...

| Recommendation on 19-11-2025 | | Recommendation | Accumulate (Downgrade) | | Price on Recommendation Date | $ 12.600 | | Suggested purchase price | N/A | | Target Price | $ 14.400 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|